Main Points:

- Tokenized securities remain subject to U.S. securities laws, regardless of on-chain novelty.

- Blockchain can facilitate capital formation and faster settlement but cannot alter an asset’s fundamental character.

- Market participants face distinct risks, especially with third-party token issuances (e.g., counterparty risk).

- Equity and ETF tokenization is gaining traction (e.g., Robinhood’s EU launch).

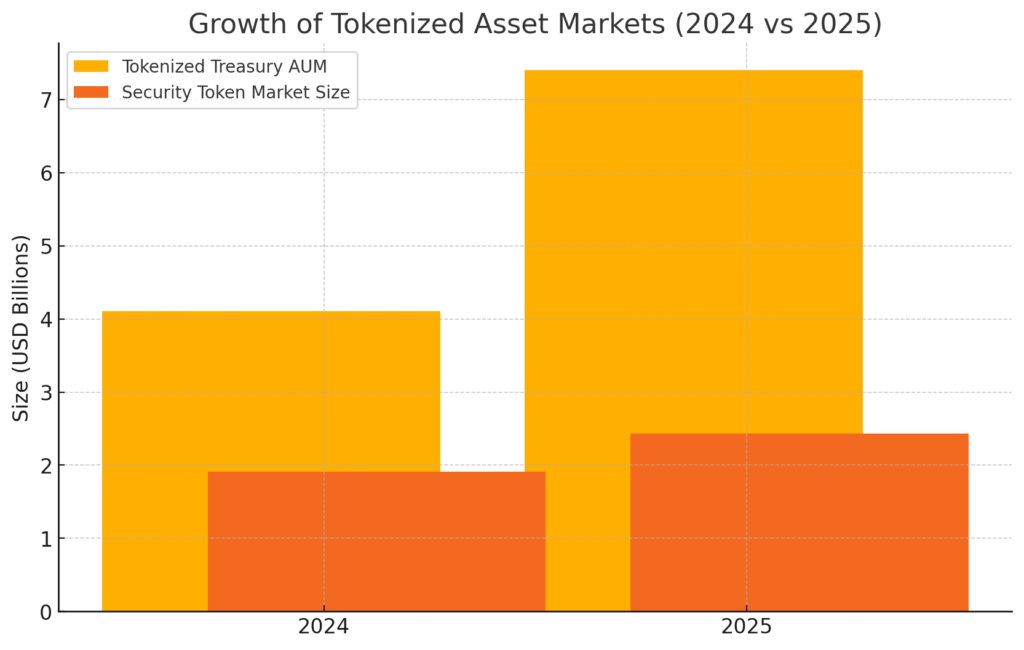

- Tokenized Treasury funds AUM jumped by 80% in H1 2025 to $7.4 billion; the broader security token market is projected at $2.43 billion in 2025.

- The SEC encourages early dialogue and stands ready to update rules where blockchain-specific exemptions are warranted.

1. Embracing Blockchain: Opportunities and Limitations

Blockchain technology has unlocked novel models for distributing and trading financial instruments in tokenized form. As SEC Commissioner Hester Peirce observed on July 9, 2025, “As powerful as blockchain technology is, it does not have magical abilities to transform the nature of the underlying asset.” Peirce recognizes blockchain’s potential to streamline processes—such as capital formation, fractional ownership, and collateral management—but stresses that these on-chain innovations cannot override established legal definitions.

Traditional securities—stocks, bonds, ETFs—when issued or traded as digital tokens, remain bound by the same substantive requirements that govern their off-chain counterparts. Faster settlement cycles, reduced counterparty layers, and programmable compliance present clear efficiency gains. Yet, these benefits do not obviate the necessity of registration, disclosure, and ongoing reporting as mandated by U.S. federal securities laws.

2. Tokenization Trends in Equity and ETFs

Tokenization of equities and ETFs has accelerated. In early July 2025, Robinhood announced the launch of tokenized shares—including private and pre-IPO equity—exclusively for EU users, marking one of the industry’s most prominent forays into on-chain stock trading. Other market participants, including Coinbase, have petitioned the SEC for approval to list tokenized securities on blockchain-based trading venues. While these developments signal growing institutional interest, they also underscore the SEC’s insistence that tokens representing ownership stakes adhere to existing registration protocols.

Many traditional fund managers are exploring tokenized versions of established products. For example, tokenized Treasury and money-market funds saw assets under management (AUM) surge 80% in the first half of 2025 to $7.4 billion, up from approximately $4.1 billion in 2024, driven by demand for higher yields and faster settlement in crypto collateral markets.

3. Regulatory Imperatives: Compliance with Securities Laws

In her statement, Peirce urged market participants to “consider—and adhere to—the federal securities laws when transacting in these instruments.” Whether tokenizing shares directly or through third-party custodians, issuers and intermediaries must fulfill registration requirements, provide prospectuses, and ensure adequate disclosures. Call for exemptions or rule updates must proceed through formal SEC channels, with Peirce indicating the Commission’s willingness to work with stakeholders on blockchain-specific carve-outs where justified.

Furthermore, SEC Chair Paul Atkins has signaled plans to propose targeted rules for distributions of crypto tokens deemed to be securities. In May 2025, Atkins highlighted the need for “clear rules of the road for the issuance, custody and trading of crypto assets” and suggested potential exemptions for registered broker-dealers operating alternative trading systems.

4. Risks in Third-Party Token Issuance

Peirce’s statement distinguishes between issuer-backed tokens and those minted by third parties. While an operating company might tokenize its own equity, an unaffiliated custodian could also create tokens representing entitlements to underlying securities. Purchasers of such third-party tokens face unique counterparty risks: if the custodian fails to honor its obligations, token holders may suffer losses despite holding a digital claim. Likewise, legal ambiguities around property rights and enforcement mechanisms on-chain heighten complexity for investors and compliance teams.

5. Market Growth Projections for Tokenized Assets

The tokenized asset space is rapidly expanding:

- Tokenized Treasury and Money-Market Funds: AUM rose from ~$4.11 billion in 2024 to $7.4 billion in H1 2025 (80% growth).

- Global Security Token Market: Projected to increase from $1.91 billion in 2024 to $2.43 billion in 2025 (CAGR ~27.3% through 2033).

The accompanying chart illustrates these growth trajectories, highlighting blockchain’s rising adoption across institutional finance.

6. Path Forward: Dialogue and Regulatory Evolution

While Peirce asserts that tokenized securities must comply with existing laws, she also emphasizes the SEC’s openness to revisiting outdated or redundant requirements. Market participants contemplating tokenization are encouraged to engage early with SEC commissioners and staff, ensuring that any proposed carve-outs or exemptions align with investor protection goals. Such collaboration could lead to streamlined processes—like automated compliance via smart contracts—without sacrificing transparency or accountability.

The SEC’s Crypto Assets and Cyber Unit and the broader regulatory framework continue to evolve. Future rulemaking may clarify custody obligations for digital assets, delineate responsibilities for smart contract failures, and establish guardrails for decentralized issuance models. Stakeholders should monitor SEC rulemaking dockets and participate in open comment periods to shape a balanced regulatory regime.

Conclusion

Tokenization stands at the intersection of traditional finance and blockchain innovation, offering efficiency gains, new market structures, and enhanced capital-formation tools. Yet, as Hester Peirce cautions, on-chain formats do not magically alter an asset’s legal identity: tokenized securities remain securities, subject to the same federal laws that govern their off-chain equivalents. Market participants must navigate disclosure, registration, and counterparty risks thoughtfully, leveraging early dialogue with regulators to refine rules for the digital age. With robust compliance and collaborative rule updates, tokenization can fulfill its promise as a transformative force in global finance—bridging the gap between legacy markets and the programmable future.