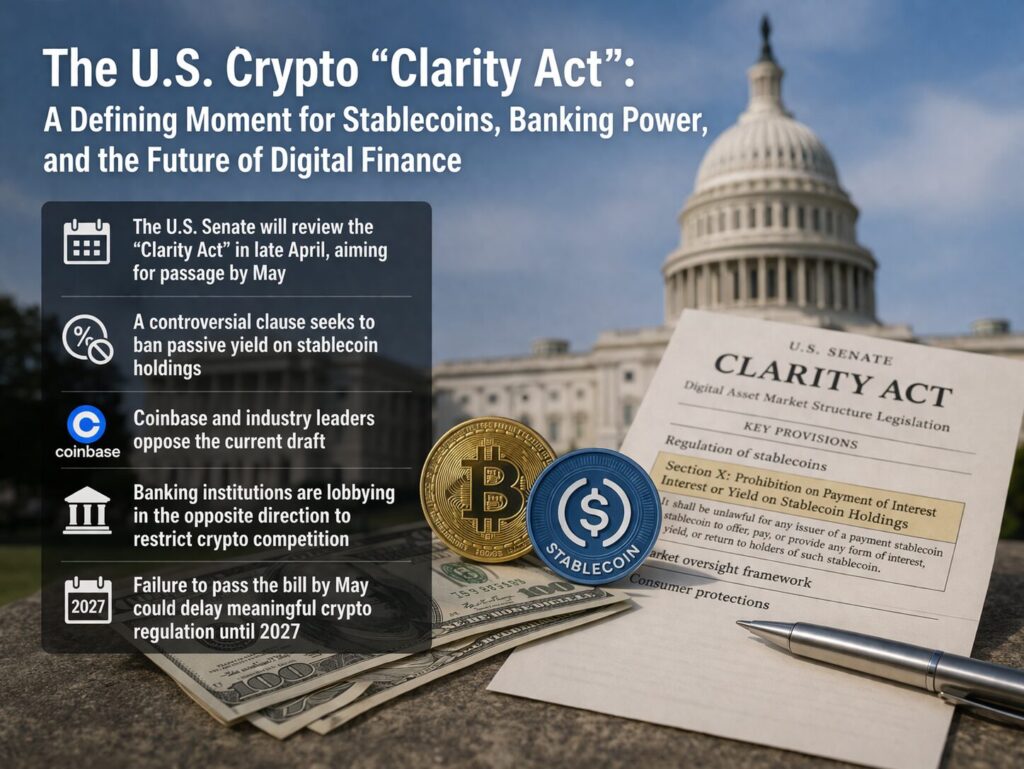

Key Points :

- The U.S. Senate will review the “Clarity Act” in late April, aiming for passage by May

- A controversial clause seeks to ban passive yield on stablecoin holdings

- Coinbase and industry leaders oppose the current draft

- Banking institutions are lobbying in the opposite direction to restrict crypto competition

- Failure to pass the bill by May could delay meaningful crypto regulation until 2027

1. A Regulatory Crossroads: Why the Clarity Act Matters Now

The United States stands at a critical inflection point in the evolution of digital asset regulation. The proposed “Clarity Act,” a sweeping market structure bill aimed at defining the legal and operational boundaries of cryptocurrencies, is scheduled for Senate committee markup in late April 2026.

While legislative efforts around crypto have been ongoing for years, this moment carries unusual urgency. According to policymakers, failure to pass the bill by May could effectively stall comprehensive crypto legislation until 2027—due to election cycles and shifting political priorities.

This timeline transforms the Clarity Act from just another regulatory proposal into a make-or-break event for the entire U.S. crypto ecosystem.

At stake is not merely compliance clarity, but the structural foundation of how digital assets—particularly stablecoins—interact with the broader financial system.

2. The Core Conflict: Stablecoin Yield and Financial Power

At the center of the controversy lies a deceptively simple issue:

Should stablecoins be allowed to generate passive yield for holders?

The current draft of the Clarity Act proposes:

- A ban on passive interest (yield) on stablecoin balances

- Allowance for activity-based rewards (e.g., payments, transactions)

This distinction has triggered intense backlash from the crypto industry.

For companies like Coinbase, stablecoin-related revenue represents a significant business line—reportedly around $1.35 billion annually, or roughly 20% of total revenue.

Eliminating passive yield would fundamentally reshape their economic model.

Why This Matters Practically

Stablecoins such as USDC are not just speculative tools—they are increasingly used for:

- Cross-border payments

- Treasury management

- On-chain settlement systems

- DeFi yield strategies

By restricting yield, the legislation would effectively remove one of the primary incentives for holding stablecoins, pushing users back toward traditional banking systems.

3. Industry vs Banking: A Structural Power Struggle

The debate around the Clarity Act is not merely regulatory—it is systemic and competitive.

On one side:

- Crypto companies argue that yield restrictions suppress innovation

- They highlight that banks earn roughly ~4% on reserves held at the Federal Reserve

- Meanwhile, depositors often receive near-zero interest

On the other side:

- Traditional banking leaders, including figures like Jamie Dimon, are reportedly pushing for stricter controls

- Their concern: stablecoins could drain deposits from commercial banks

This creates a fundamental tension:

| System | Yield Flow | Control |

|---|---|---|

| Traditional Banking | Centralized, opaque | Banks retain spread |

| Stablecoin Economy | Transparent, programmable | Users capture yield |

The Clarity Act effectively determines which model dominates the next decade of finance.

Stablecoin vs Traditional Banking Yield Flow (Conceptual)

4. Coinbase’s Counterproposal and Industry Coordination

Facing significant financial impact, Coinbase has taken an aggressive stance.

This is already the second time the company has withdrawn support for the bill.

More importantly, Coinbase is now:

- Coordinating with major crypto firms

- Developing a formal counterproposal

- Attempting to revise the language before April markup

Their primary argument is that the current compromise text—introduced by bipartisan lawmakers—would:

- Not only ban passive yield

- But effectively block activity-based rewards as well

If true, this would eliminate nearly all economic incentives tied to stablecoins.

5. Political Dynamics: Bipartisan Fragility

Despite strong industry resistance, lawmakers are attempting to maintain bipartisan momentum.

Cynthia Lummis emphasized that:

- The goal is to protect stablecoin innovation

- While also preventing deposit outflows from community banks

This balancing act reflects a deeper political reality:

- Republicans tend to favor innovation and market competition

- Democrats often prioritize financial stability and consumer protection

The Clarity Act sits precisely at the intersection of these philosophies.

6. What Happens If the Bill Fails?

According to Senator Moreno, failure to pass the bill by May could push meaningful crypto legislation to 2027 or beyond.

Implications of Delay

If that happens, several consequences are likely:

- Continued regulatory fragmentation

- Increased offshore migration of crypto businesses

- Slower institutional adoption in the U.S.

- Competitive advantage shifting to jurisdictions like:

- Singapore

- UAE

- Hong Kong

For investors and builders, this creates a paradox:

- Short-term uncertainty

- Long-term opportunity

Periods of regulatory ambiguity often coincide with early-stage innovation cycles.

Global Crypto Regulatory Competition Map

7. Strategic Implications for Investors and Builders

For readers seeking new assets, revenue streams, and real-world blockchain applications, the Clarity Act offers several actionable insights:

1. Stablecoin Yield May Become a Premium Feature

If restricted in the U.S.:

- Yield-bearing stablecoins may migrate offshore

- New structures (e.g., tokenized money market funds) could emerge

2. Infrastructure Plays Will Outperform

Rather than betting on tokens alone:

- Payment rails

- On/off ramps

- Compliance tooling

These areas are likely to see institutional capital inflows

3. Regulatory Arbitrage Will Expand

Developers and companies will increasingly:

- Structure entities across multiple jurisdictions

- Optimize for regulatory efficiency

This trend is already visible in global crypto hubs.

8. The Bigger Picture: Finance Is Being Rewritten

At its core, the Clarity Act is not just about crypto.

It represents a deeper question:

Who controls money in a digital world?

- Banks?

- Governments?

- Protocols?

- Users themselves?

Stablecoins are the first large-scale test of this question.

And yield—often dismissed as a technical detail—is actually the mechanism of power distribution.

Conclusion

The upcoming Senate review of the Clarity Act marks one of the most consequential moments in modern financial history.

Whether the bill passes, fails, or is significantly amended, the outcome will shape:

- The future of stablecoins

- The competitive balance between banks and crypto

- The global positioning of the United States in digital finance

For investors, builders, and institutions, the message is clear:

Regulation is no longer a background factor—it is the primary driver of opportunity.