Key Points :

- A potential compromise has emerged after two months of negotiations between crypto and banking stakeholders

- The central issue is whether stablecoins can offer yield—and how that affects traditional bank deposits

- Major players like Coinbase signal progress, indicating a possible breakthrough

- Political timing (2026 midterm elections) may determine whether the bill succeeds or fails

- Stablecoins are becoming a critical battleground for financial dominance between crypto platforms and banks

Introduction: A Defining Moment for Crypto Regulation

The United States is approaching a pivotal moment in shaping the regulatory future of digital assets. The proposed “Clarity Act,” a comprehensive market structure bill for cryptocurrencies, has long been stalled due to deep divisions between the crypto industry and the traditional banking sector. However, recent developments suggest that a viable compromise may finally be within reach.

After nearly two months of negotiations, stakeholders from both industries have reportedly converged on a revised proposal. While details remain undisclosed, insiders from both sides have expressed cautious optimism, calling the latest draft a “workable solution.”

This progress is particularly significant given the prior deadlock. Earlier drafts introduced by lawmakers—including figures like Thom Tillis and Angela Alsobrooks—failed to gain industry support, causing legislative momentum to stall. Now, with renewed alignment, the Clarity Act may be back on track.

The Core Conflict: Stablecoin Yield vs. Bank Deposits

At the heart of the dispute lies a deceptively simple question:

Should stablecoin providers be allowed to offer yield to users?

Stablecoins—such as USD Coin and Tether—are designed to maintain a stable value, typically pegged to the U.S. dollar. Unlike volatile cryptocurrencies like Bitcoin or Ethereum, stablecoins are increasingly used as digital cash equivalents in blockchain ecosystems.

However, the controversy arises when these stablecoins begin offering interest or yield to holders.

Why Banks Are Concerned

Traditional banks rely heavily on customer deposits as a source of capital for lending and investment. If stablecoin issuers offer higher yields than banks, users may shift their funds away from bank accounts into crypto platforms.

This could lead to:

- Reduced deposit bases for banks

- Higher funding costs

- Potential instability in traditional financial systems

From the banking perspective, stablecoin yields represent not just competition—but systemic risk.

Why Crypto Supports Yield

For the crypto industry, yield-bearing stablecoins are essential for:

- Attracting liquidity

- Enabling decentralized finance (DeFi) ecosystems

- Competing with traditional financial products

Platforms like Coinbase have argued that prohibiting yield would stifle innovation and unfairly advantage legacy financial institutions.

Signs of Progress: A “Workable Compromise”

Recent reports indicate that a compromise has been reached—at least in principle. While specifics are still confidential, the tone from both sides has shifted noticeably.

Notably, Coinbase’s Chief Legal Officer, Paul Grewal, stated that an agreement on the stablecoin yield issue could be achieved within 48 hours, expressing strong confidence in forward movement.

This is particularly meaningful because Coinbase had previously opposed the bill. Its change in tone suggests that the revised proposal addresses key industry concerns.

The White House Factor: A Hidden Report

An important yet unresolved element in this debate is a report from the White House’s Council of Economic Advisers (CEA).

The report examines the impact of stablecoin yields on:

- Bank deposits

- Lending capacity

- Financial stability

Interestingly, early indications suggest that the report is favorable to the crypto industry. According to insiders, it challenges the assumption that stablecoin yields significantly harm banks.

CEA Acting Chair Pierre Yared has publicly stated that:

- The impact on banks is likely small

- The potential for stablecoin adoption is significant

Despite this, the report has not yet been released—raising questions about political timing and strategic considerations.

Political Pressure: The Race Against Time

Even if a compromise is finalized, the legislative journey is far from over.

The Clarity Act must still:

- Pass Senate committee markup

- Secure approval in the full Senate

- Be reconciled with House versions

- Survive political negotiations across parties

The timeline is tight.

With the 2026 midterm elections approaching, lawmakers face increasing pressure. If the bill is not passed before August 2026, it risks being delayed indefinitely due to campaign season dynamics.

Treasury Secretary Scott Bessent has acknowledged that political control of Congress could determine the bill’s fate. A shift in power—particularly if Democrats gain control of the House—could complicate or even halt progress.

Broader Implications: A Battle for Financial Infrastructure

This debate is not just about regulation—it is about the future structure of finance.

Stablecoins are rapidly evolving into:

- Payment rails

- Settlement layers

- Liquidity hubs for global finance

If yield-bearing stablecoins are permitted, they could:

- Compete directly with bank savings accounts

- Enable borderless financial services

- Accelerate adoption of decentralized finance

Conversely, strict limitations could:

- Reinforce traditional banking dominance

- Slow crypto innovation

- Push activity offshore to more favorable jurisdictions

Market Trends: Why This Matters Now

Beyond legislation, broader market trends are reinforcing the importance of this debate:

1. Institutional Entry

Major financial institutions are increasingly exploring stablecoins for payments and settlement.

2. DeFi Expansion

Yield generation is a core component of DeFi protocols, making regulatory clarity critical.

3. Global Competition

Jurisdictions like the EU (with MiCA regulations) and parts of Asia are advancing crypto frameworks faster than the U.S.

4. Dollar Dominance

Stablecoins pegged to the U.S. dollar may reinforce global dollar dominance—an argument often used in favor of supportive regulation.

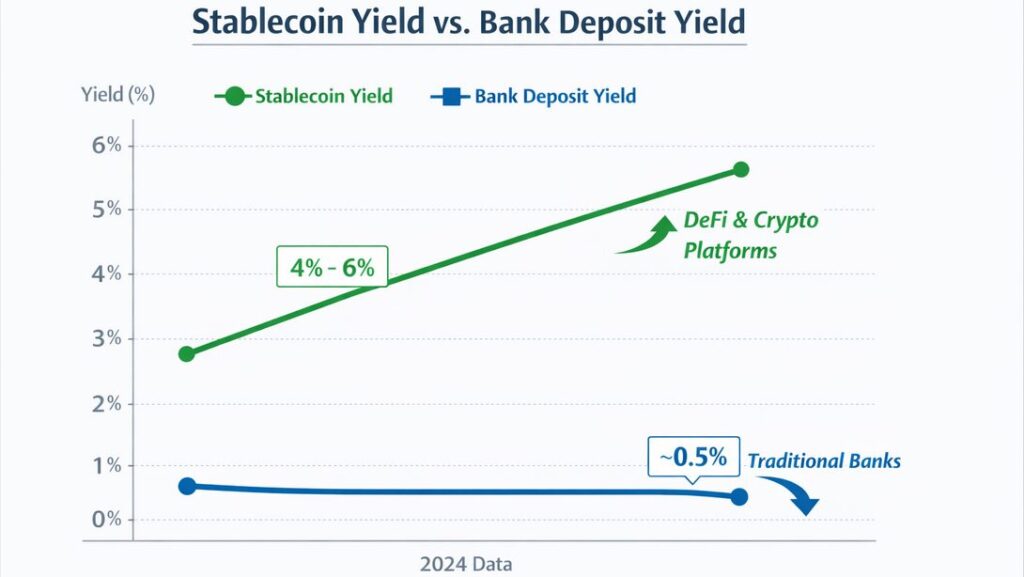

(Stablecoin vs Bank Deposit Yield Comparison Chart)

Conclusion: A Turning Point for Crypto and Banking

The Clarity Act represents one of the most consequential regulatory efforts in the history of digital assets.

The emerging compromise on stablecoin yield could redefine:

- How money is stored

- How financial institutions compete

- How innovation is regulated

While significant hurdles remain, the current momentum suggests that a breakthrough is possible.

For investors, builders, and institutions alike, the outcome of this legislation will shape not just the U.S. crypto market—but the global financial system.