Main Points :

- The U.S. Department of Defense has initiated a plan to stockpile roughly $1 billion in critical minerals (rare earths and other strategic metals) to reduce dependence on China, reflecting a shift in national security strategy.

- This effort is part of a broader global pivot toward securing supply chains for technologies like EVs, semiconductors, and advanced electronics.

- China, in response to global pressure, clarified that its export controls on rare earths are legal and that compliant applications will still be approved, relieving worst-case fears.

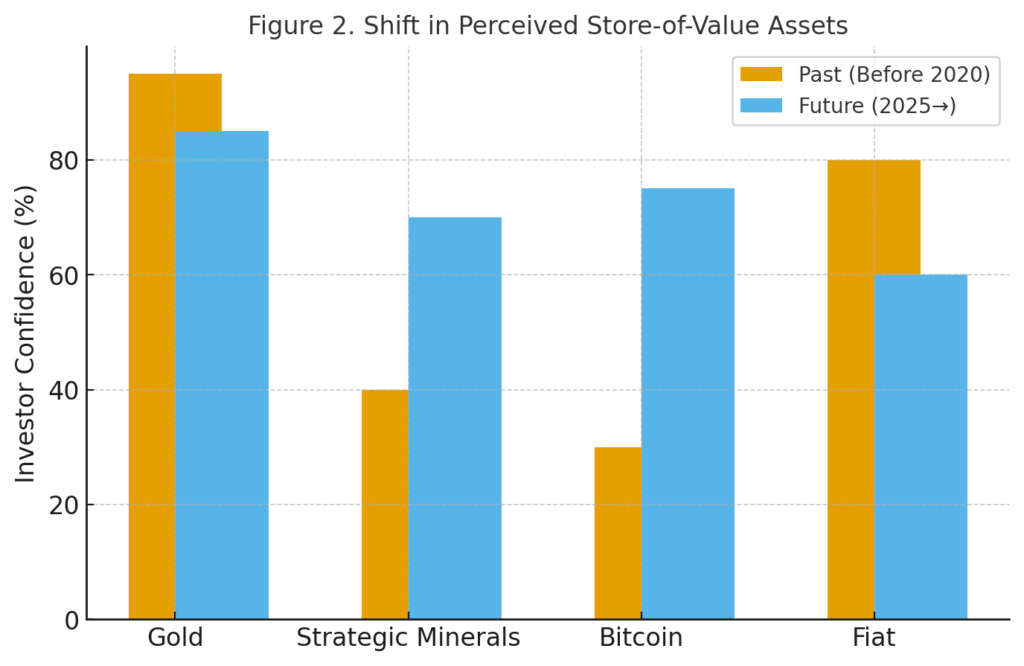

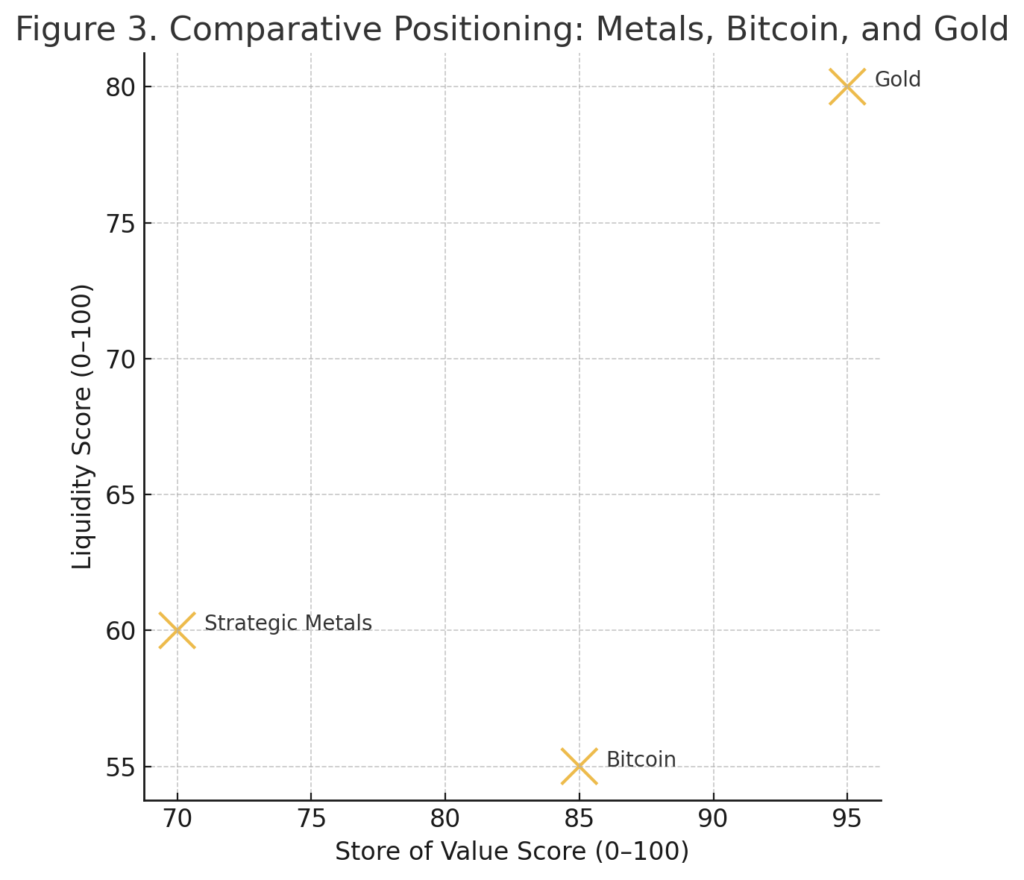

- In this context, gold has traditionally been viewed as a “safe haven,” but strategic minerals are gaining a new role in value storage given their critical industrial importance.

- Bitcoin (BTC) is being reconsidered by some as a form of “digital gold,” especially in scenarios of geopolitical or trade disruption, but it faces challenges in volatility, mining costs, and its sensitivity to broader risk sentiment.

- The U.S. move signals a broader redefinition of “store of value”: not only precious metals but also strategic materials and digital assets are now in the conversation.

- For crypto investors, this evolving backdrop suggests that BTC (and potentially other non-fiat digital assets) may see renewed interest, especially from those seeking assets unlinked from physical supply chains.

Below is an English-written, more expansive version, followed by a corresponding full Japanese translation.

1. U.S. Strategic Minerals Stockpile Initiative

The U.S. Department of Defense (Pentagon) has launched a plan to amass up to $1 billion worth of critical minerals, including rare earth elements, in order to shore up the nation’s supply chain resilience. This is part of a strategic pivot away from reliance on Chinese supplies for resources vital to electric vehicles, advanced electronics, semiconductors, aerospace, and defense systems.

This initiative reflects growing unease globally over supply chain fragility, especially after China tightened controls on rare earth exports—a move that raised fears of potential embargoes.

The stockpiling plan is intended as both a buffer against future supply shocks and as leverage in geopolitical competition over key technologies.

2. China’s “Softening” Stance and Market Reaction

In recent days, China responded to concerns by clarifying that its export restrictions are not blanket bans but regulatory controls in line with international law. Applications meeting the requisite criteria will still be approved.

This clarification helped calm markets that had begun to price in extreme worst-case scenarios. The possibility of an outright embargo had pushed speculative premiums in resource markets and triggered risk-off flows in equities.

By signaling that the controls are manageable, China has allowed markets to reframe the situation as more of a geopolitical negotiation than a sudden supply cutoff.

3. Commodities, Mineral Scarcity, and the Redefinition of “Safe Assets”

Traditionally, geopolitical stress has pushed capital into gold and other precious metals, which are seen as stores of value in turbulent times. But now, strategic minerals such as lithium, cobalt, neodymium, and others are being recast as containing embedded security value, because they are essential to modern infrastructure and defense systems.

This means that demand for such metals may increasingly be driven not only by industrial use but by strategic stockpiling. In effect, they become dual-purpose: input commodities and quasi “reserve assets.”

Assets whose scarcity and importance are tied to next-generation technology (AI, EVs, 5G, defense systems) may thus rise in relevance as value stores in their own right.

4. Bitcoin as “Digital Gold”: Promise and Pitfalls

Given its independence from physical supply chains, Bitcoin has sometimes been framed as a “digital gold” or an alternative store of value disconnected from geopolitics and trade restrictions. In a scenario where physical supply chains are disrupted, Bitcoin’s intangible nature could be advantageous.

However, Bitcoin is not immune to broader market sentiment and risk appetite. In a sharp sell-off, BTC can suffer steep losses alongside equities or other risk assets.

Mining economics also depend on inputs like semiconductors, energy, and hardware—all of which could be influenced by the same supply chain pressures the U.S. is attempting to avoid. If chip shortages or energy constraints arise, mining margins may crumble.

Moreover, Bitcoin lacks the industrial utility that gives strategic minerals their real-world backbone; its value is purely based on demand, network effect, and perceived scarcity.

5. Implications for Crypto Investors and Blockchain Practitioners

For those seeking new crypto assets or yield opportunities, the current environment suggests several angles to watch:

- BTC as geopolitical hedge: Some capital may rotate into Bitcoin if confidence weakens in traditional markets or if supply chains face disruption.

- Layer-1 / infrastructure plays: Projects that facilitate decentralized finance, cross-chain messaging, or alternative consensus mechanisms (e.g., Proof of Useful Work) may gain more attention, especially as investors seek assets with intrinsic utility.

- Tokenized minerals or commodity wrappers: Blockchain protocols that tokenize rare earth or strategic metal exposure might gain traction, merging the worlds of resource scarcity and on-chain liquidity.

- Energy and mining innovations: Crypto projects innovating in low-energy consensus (e.g. Proof of Stake, Proof of Space, or hybrid models) may become more attractive in an era where energy supply and semiconductors become more contested.

- Treasury strategies for institutions: We may see more funds adopting hybrid treasury models—allocating among gold, strategic metals, and crypto holdings, hedging across domains.

6. Recent Trends and Data (2025 Context)

- Reporting suggests the Pentagon is actively seeking to acquire $1 billion in critical minerals to counter China’s dominance.

- Analysts note that while U.S. investment in rare earth supply chains lags, China’s dominance remains strong.

- In crypto markets, Bitcoin recently rebounded from a volatility spike triggered by escalated U.S. tariffs on Chinese goods.

- Institutional interest in crypto remains robust, with recent ETF inflows signaling that institutional capital is still actively seeking exposure to Bitcoin and Ethereum.

- Commodities markets are also seeing renewed attention; for example, silver has surged, partly driven by its dual role as industrial input and speculative value store.

Summary & Outlook

The U.S. decision to allocate $1 billion toward strategic mineral stockpiling marks a notable shift in how value and security are being conceived at the intersection of geopolitics, technology, and capital markets. In this evolving landscape, assets beyond traditional safe havens—especially those tied to critical technologies and supply chains—are being reframed as contenders for “store of value” status.

For crypto investors, Bitcoin’s independence from physical constraints offers a compelling narrative, especially under heightened geopolitical tension. Yet Bitcoin’s vulnerabilities—volatility, ASIC/mining dependency, and sensitivity to risk sentiment—should not be ignored. The future may not be about a single “digital gold,” but rather a diversified portfolio of real and digital assets: strategic minerals, tokenized exposures, energy-efficient blockchains, and crypto infrastructure protocols.

As we proceed through 2025 and beyond, watch for capital flows among these classes and the emergence of new tokenized commodities or blockchain infrastructure that explicitly tie to tangible strategic resources. That may herald the next frontier where crypto and real-world scarcity converge.