Key Takeaways :

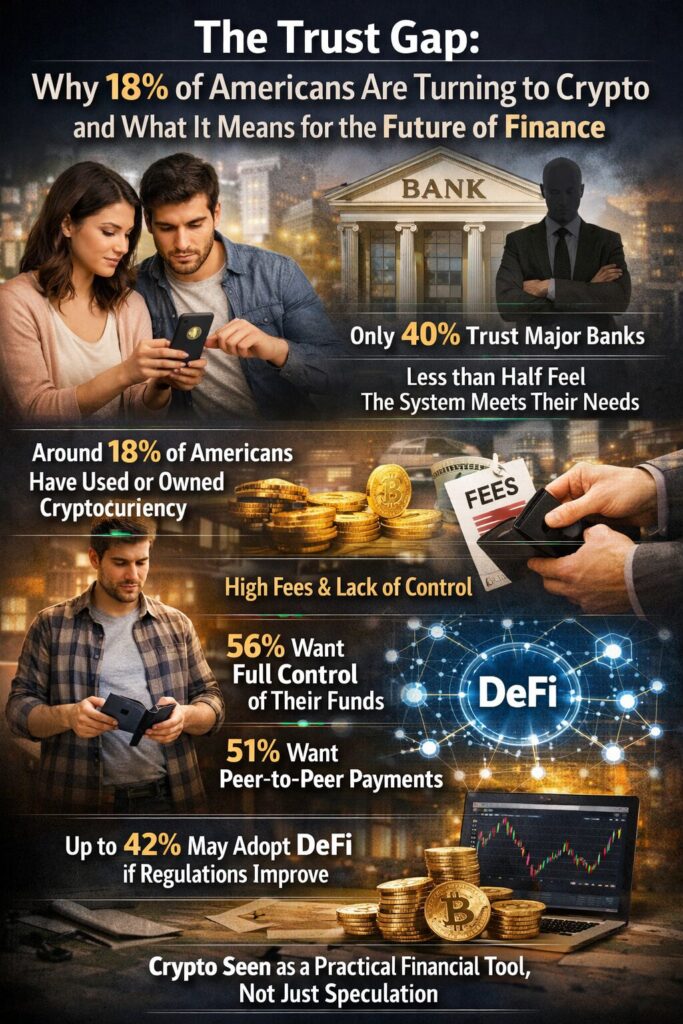

- Around 18% of Americans have used or owned cryptocurrency

- Only 40% trust major banks, and less than half feel the system meets their needs

- High fees and lack of control are primary drivers of dissatisfaction

- 56% want full control of their funds, and 51% want peer-to-peer payments without intermediaries

- Up to 42% may adopt DeFi if regulatory clarity improves

- Crypto is increasingly seen as a practical financial tool, not just speculation

Adoption vs Trust Gap

Introduction: A Structural Shift in Financial Trust

A recent nationwide survey conducted by the DeFi Education Fund (DEF) and Ipsos has revealed a fundamental shift in how Americans perceive financial systems. While traditional banking institutions have long been the backbone of economic activity, their dominance is increasingly being questioned.

Only 49% of respondents believe the current financial system meets their needs, and trust in major banks stands at a strikingly low 40%. At the same time, 18% of Americans—nearly one in five—have already engaged with cryptocurrency.

This is not merely a trend. It represents a structural transformation in financial behavior, driven by dissatisfaction, technological awareness, and a growing demand for autonomy.

1. Who Is Using Crypto? A Demographic Breakdown

Millennials Lead the Charge

Among all age groups, millennials (ages 30–44) show the highest adoption rate, with 22% actively using cryptocurrency in the past 12 months. This group sits at the intersection of digital literacy and financial responsibility, making them natural adopters of emerging financial technologies.

Diverse and Expanding User Base

Crypto adoption is no longer limited to niche tech communities. The survey highlights:

- 20% of Black (non-Hispanic) Americans have used crypto

- 20% of men report usage

- 16% of individuals with a bachelor’s degree or higher are involved

This diversification suggests that crypto is transitioning from a speculative asset class into a mainstream financial tool.

2. The Crisis of Confidence in Traditional Banking

The Fee Problem

One of the most striking findings is the widespread dissatisfaction with banking fees. Only 23% of respondents believe bank fees are fair.

For many users, the cost of:

- International remittances

- Currency conversion

- Account maintenance

creates friction that directly impacts financial accessibility.

Trust Deficit

Trust is the foundation of financial systems. Yet, only 40% of Americans trust major banks. This trust gap is not just emotional—it has economic consequences.

When users begin to question the fairness and transparency of financial institutions, they naturally explore alternatives.

3. The Rise of Financial Self-Sovereignty

Control Over Funds

A significant 56% of respondents want full control over their money at all times. This aligns closely with one of crypto’s core value propositions: self-custody.

Unlike traditional banking, where assets are intermediated, blockchain-based systems allow users to:

- Hold private keys

- Execute transactions directly

- Avoid third-party dependency

Demand for Peer-to-Peer Payments

Additionally, 51% of Americans want the ability to send digital payments without intermediaries. This demand directly supports the growth of:

- Stablecoins

- Layer-1 blockchain networks

- Payment-focused protocols

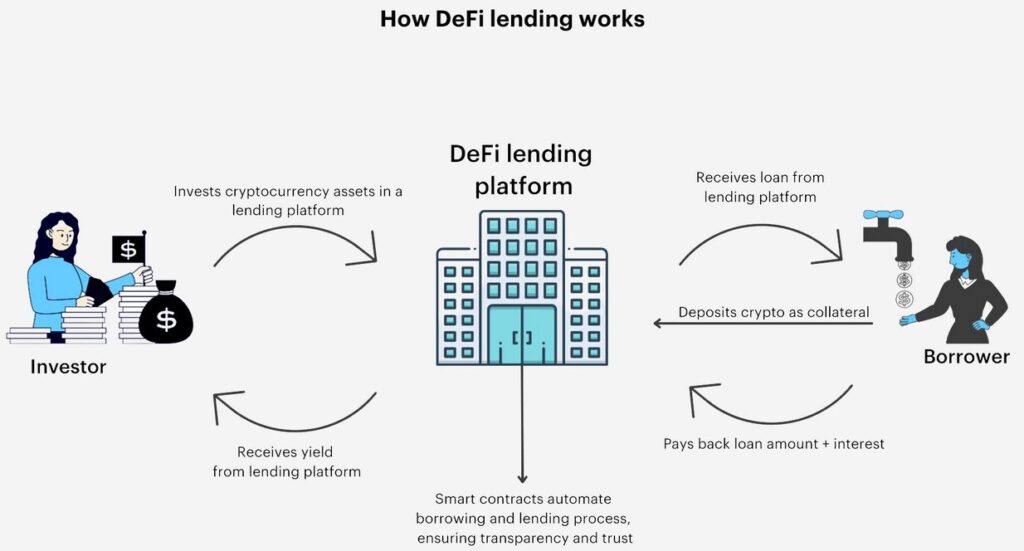

DeFi Use Cases

4. DeFi as the Next Financial Layer

Potential Adoption Surge

The survey indicates that 42% of Americans would consider using DeFi if regulations were clearer. This highlights a critical bottleneck: regulatory uncertainty.

As governments define frameworks for:

- Digital asset custody

- AML/KYC compliance

- Consumer protection

DeFi adoption could accelerate rapidly.

Primary Use Cases

Respondents identified practical use cases for DeFi:

- Online purchases (84%)

- Payments (78%)

- Savings (77%)

These are not speculative behaviors—they are core financial activities.

5. Broader Industry Trends (2025–2026)

Institutional Convergence

Major financial institutions are increasingly integrating blockchain technology. From tokenized assets to stablecoin settlements, traditional finance is adapting rather than resisting.

Stablecoin Expansion

Stablecoins are becoming a critical bridge between fiat and crypto economies. Their use in remittances and payments directly addresses the inefficiencies highlighted in the survey.

Regulatory Momentum

Countries are moving toward clearer frameworks:

- The U.S. is advancing discussions around crypto legislation

- The EU’s MiCA framework is setting global standards

- Asian markets are rapidly adopting digital asset regulations

6. Implications for Builders and Investors

Opportunities for New Revenue Streams

For entrepreneurs and developers, the data points to clear opportunities:

- Low-fee payment systems

- User-controlled wallets (non-custodial)

- DeFi savings and yield products

- Cross-border settlement infrastructure

UX as a Competitive Advantage

Despite growing interest, onboarding remains a challenge. Simplifying:

- Wallet creation

- Key management

- Compliance processes

will be critical to mass adoption.

Bridging Two Financial Worlds

The future likely lies in hybrid models—systems that combine:

- The usability of centralized platforms

- The transparency and control of decentralized networks

Conclusion: From Distrust to Decentralization

The findings from the DEF and Ipsos survey reveal more than dissatisfaction—they highlight a turning point.

As trust in traditional banking declines and demand for financial autonomy rises, cryptocurrency and DeFi are emerging as viable alternatives. What began as an experimental technology is now evolving into a foundational layer of modern finance.

For investors, builders, and institutions alike, the message is clear:

The shift toward decentralized, user-controlled finance is not coming—it is already underway.