Main Points:

- Executive order to allow alternative assets—including cryptocurrencies—in 401(k) plans

- GENIUS Act establishes stablecoin regulatory framework, signaling broader crypto acceptance

- FHFA directive to count unconverted crypto holdings in mortgage underwriting

- Advantages: portfolio diversification, inflation hedge, increased mainstream adoption

- Risks: volatility, liquidity issues, systemic stability concerns, fiduciary responsibilities

- Implications for Japanese investors: global market shifts, strategic portfolio adjustments

- FAQs addressing timing, asset choice, and cross-border applicability

1. 401(k) Crypto Inclusion: A New Asset Class for Retirement Plans

On July 10, 2025, President Trump announced an executive order directing the Department of Labor and SEC to issue guidance opening defined contribution retirement plans—including 401(k) accounts—to alternative investments such as private equity, hedge funds, and cryptocurrencies. This directive reverses a cautious stance from the Biden administration and aims to diversify retirement portfolios beyond traditional equity and bond funds.

1.1 Background: The US 401(k) Landscape

The 401(k) system underpins retirement savings for over half of the U.S. workforce, with approximately $9 trillion in total assets under management and a participation rate nearing 50 %. Historically, plan offerings have included mutual funds, ETFs, and select alternative funds, but direct crypto exposure was rare and typically limited to self-directed brokerage windows.

1.2 Executive Order Details

- Issuing Bodies: Department of Labor & SEC

- Authorized Assets: Private equity, REITs, venture capital, and cryptocurrencies (e.g., BTC, ETH, major altcoins)

- Access Mechanism: Structured products and managed accounts, rather than direct token holdings.

Employers may begin incorporating these options through third-party plan providers, who will be obligated to uphold fiduciary standards and enhance participant education.

1.3 Implementation Timeline

- July 10, 2025: Executive order signed

- Q3 2025: Regulatory guidance issued

- Q4 2025: Pilot programs launch with select plan providers

- 2026: Full rollout across qualified plans

[Insert Figure 1: Timeline of Crypto Reform Implementation Here]

2. Mortgage Lending Meets Cryptocurrency

Shortly after the 401(k) announcement, the Federal Housing Finance Agency (FHFA) instructed Fannie Mae and Freddie Mac to recognize unconverted cryptocurrency holdings—rather than cashing out—as valid assets in mortgage underwriting. This policy could expand homebuying opportunities for crypto holders by factoring in on‑chain assets directly.

2.1 Traditional Mortgage Underwriting

Traditionally, borrowers have been required to liquidate crypto into USD prior to loan closing, ensuring transparency and regulatory compliance. Crypto was viewed as a speculative holding, unsuitable for collateral valuation.

2.2 FHFA’s New Directive

- Eligible Assets: Bitcoin (BTC), Ethereum (ETH), and approved stablecoins valued at face value

- Valuation Method: Mark‑to‑market for volatile assets, face‑value for stablecoins

- Risk Adjustments: Haircuts applied based on asset volatility ratings.

2.3 Political Pushback

Democratic lawmakers—including Senators Elizabeth Warren, Jeff Merkley, and Bernie Sanders—are probing the FHFA’s move, citing concerns over heightened systemic risk and the potential for crypto market downturns to trigger mortgage defaults.

3. Benefits and Risks: A Balanced View

3.1 Benefits

- Portfolio Diversification: Crypto allocations may enhance risk–return profiles, especially with mature tokens like BTC and ETH.

- Inflation Hedge: Bitcoin’s capped supply and stablecoins’ peg to USD provide distinct inflation‑combat strategies.

- Mainstream Adoption: Integration into 401(k)s and mortgages legitimizes crypto as a financial asset class, driving institutional involvement.

3.2 Risks and Challenges

- High Volatility: Price swings can erode retirement balances and destabilize mortgage portfolios.

- Liquidity Constraints: Converting large orders may impact market prices, especially for less liquid tokens.

- Regulatory Uncertainty: Future rule changes could redefine eligible assets and reporting requirements.

- Fiduciary Duty and Education: Plan sponsors must ensure participants understand risks, avoiding misallocation.

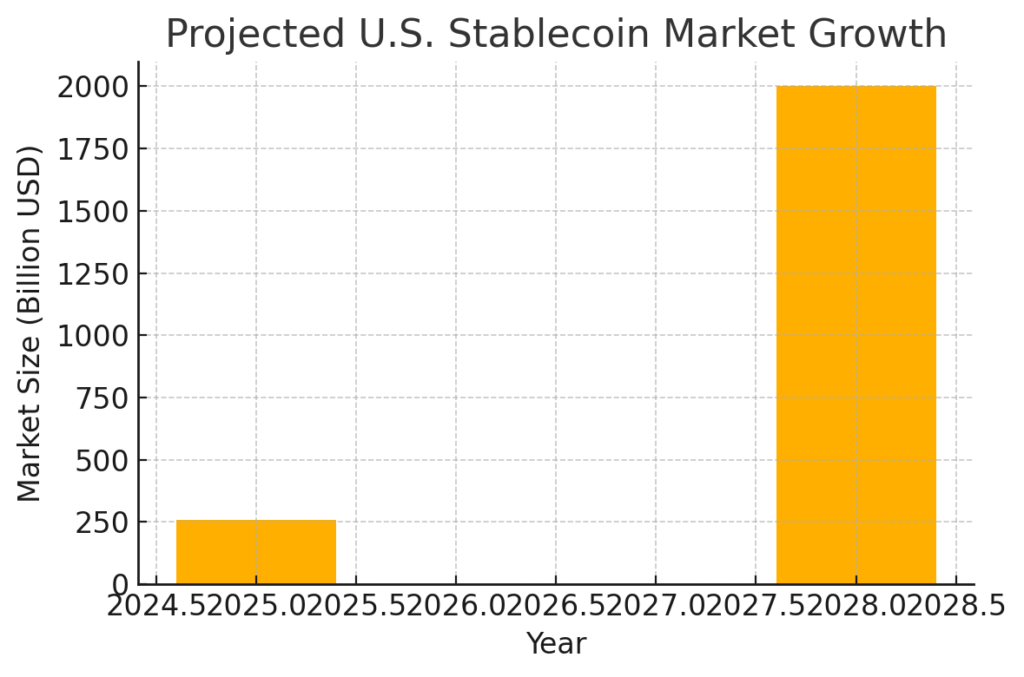

[Insert Figure 2: Projected U.S. Stablecoin Market Growth Here]

4. Implications for Japanese Investors

4.1 Global Market Shifts

The U.S. moves reflect a broader trend of regulatory clarity, which may influence Japanese policy discussions around integrating crypto into pension schemes like iDeCo and qualified pension funds.

4.2 Strategic Portfolio Adjustments

- Diversify Globally: Consider adding U.S.-listed crypto funds or ETFs to capture growth while hedging currency risk in JPY.

- Stablecoin Yield Farming: Evaluate regulated stablecoin products for yield generation, mindful of counterparty risk.

- Regulatory Watch: Monitor Japan’s Financial Services Agency (FSA) for potential revisions to crypto asset definitions and custody rules.

5. Frequently Asked Questions (FAQ)

Q1: When will these policies take effect?

401(k) crypto integration begins in late 2025, with full availability in 2026. Mortgage recognition is effective immediately upon FHFA guidance release in July 2025.

Q2: Can retirement assets lose value due to crypto volatility?

Yes, significant price swings can reduce portfolio value. Hence, risk‑management tools like automatic rebalancing and volatility buffers are recommended.

Q3: Which cryptocurrencies should beginners consider?

Large‑cap tokens (BTC, ETH) and regulated stablecoins (USDC, USDT) offer a balance between growth potential and stability.

Q4: Will Japan implement similar measures?

While iDeCo currently excludes crypto, growing international precedents may prompt the FSA to explore pilot programs.

Q5: How do taxes apply to crypto in 401(k)s and mortgages?

Crypto held within a qualified plan defers capital gains taxes until withdrawal. Mortgage-related crypto valuations could trigger tax events upon sale or liquidation.

6. Conclusion

The Trump administration’s dual approach—liberalizing 401(k) investments and modernizing mortgage underwriting—marks a watershed moment for mainstream crypto adoption. By embedding digital assets into foundational financial products, the U.S. is poised to accelerate institutional and retail participation. However, safeguarding against volatility, ensuring liquidity, and upholding fiduciary standards remain paramount. Japanese investors should closely monitor regulatory developments, diversify thoughtfully, and leverage emerging products to harness this evolving landscape.