Key Takeaways :

- Stanley Druckenmiller predicts stablecoins could underpin global payments within 10–15 years

- Stablecoin market cap has grown to over $315 billion, with transaction volumes exceeding $33–35 trillion annually

- Real-world payments using stablecoins reached approximately $390 billion per year, doubling since 2024

- Traditional payment rails (e.g., Visa and Mastercard) are now actively integrating stablecoins

- Transaction costs can drop from $30 → less than $0.01, with near-instant settlement

- Regulatory clarity (e.g., the GENIUS Act) is accelerating institutional adoption

Introduction: A Rare Bullish Signal from a Skeptic

For decades, Stanley Druckenmiller has been known as one of the most disciplined macro investors in global finance. Unlike many crypto enthusiasts, he has historically expressed skepticism toward most cryptocurrencies, often describing them as “solutions in search of problems.”

Yet in a recent interview with Morgan Stanley, his tone shifted—decisively.

While maintaining doubts about speculative digital assets, Druckenmiller drew a sharp distinction: stablecoins are different. In his view, they represent a genuinely useful financial innovation with the potential to reshape the global payments infrastructure within the next decade.

This is not a casual endorsement. It is a signal that even the most conservative capital allocators are beginning to recognize a structural shift in how money moves.

Stablecoins vs. Traditional Crypto: A Functional Divide

Stablecoins are fundamentally different from volatile cryptocurrencies like Bitcoin or Ethereum.

Rather than fluctuating wildly in price, stablecoins are typically pegged to fiat currencies such as the U.S. dollar. Examples include:

- Tether

- USD Coin

These digital assets function as programmable money, enabling fast, low-cost transfers across blockchain networks.

Druckenmiller’s key insight lies here:

Stablecoins are not speculative instruments—they are financial infrastructure.

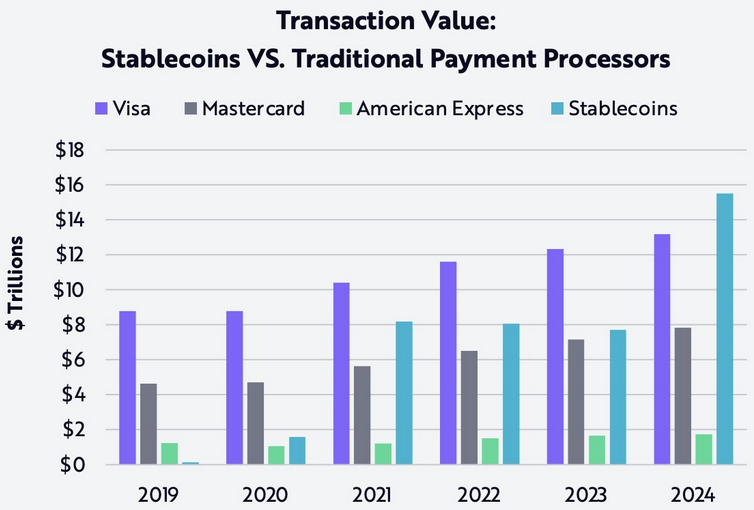

Market Growth: From Niche Tool to Global Liquidity Layer

The growth of stablecoins over the past five years has been extraordinary.

- Market capitalization: ~$55 billion → ~$315 billion

- Annual on-chain transaction volume: $33–35 trillion

This means stablecoins are now processing more value than traditional payment networks like Visa.

(Graph: Growth of Stablecoin Market Cap and Transaction Volume Over Time)

However, a critical nuance must be understood:

Most of this volume is still crypto-native activity—trading, liquidity provisioning, and DeFi operations.

Real-world usage, while growing, remains a fraction of total volume.

Real-World Payments: The $390 Billion Inflection Point

Despite the dominance of trading activity, stablecoins are rapidly gaining traction in real-world applications.

- Annual real-world payments: ~$390 billion

- Growth: More than 2× since 2024

This includes:

- Cross-border remittances

- Payroll distribution for global teams

- Supplier payments

- Treasury management

For companies operating across jurisdictions, stablecoins eliminate delays, reduce costs, and simplify reconciliation.

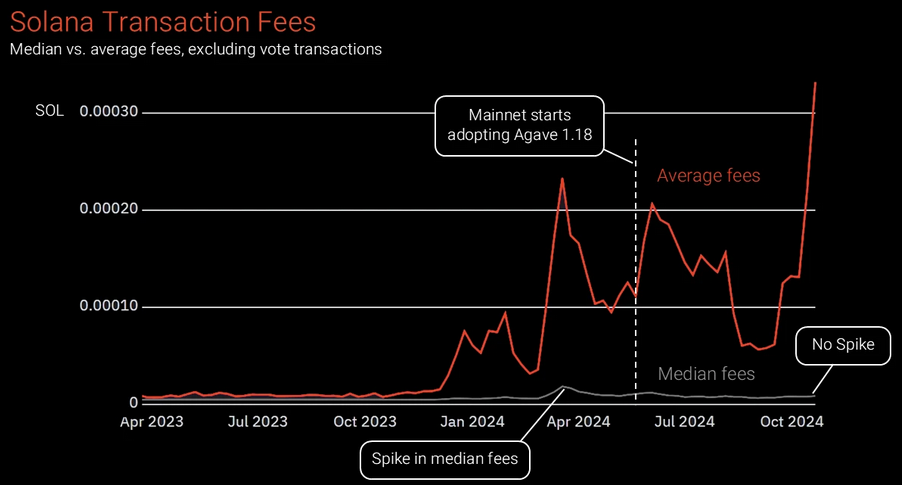

Why Stablecoins Are Disruptive: Speed, Cost, and Availability

Traditional financial rails suffer from structural inefficiencies:

- Settlement time: 1–5 days

- Fees:

- Card networks: 2–3%

- Cross-border transfers: ~6.5%

Stablecoins offer a radically different model:

- Settlement: seconds to minutes

- Availability: 24/7/365

- Cost: often <$0.01 per transaction

On networks like Solana, transaction fees can be as low as $0.00025.

(Chart: Cost Comparison — Traditional Payments vs Stablecoins)

This cost compression is not incremental—it is orders of magnitude.

Institutional Adoption: From Experimentation to Integration

Major financial players are no longer observing from the sidelines.

- Visa is piloting USDC settlement

- Mastercard is integrating stablecoin payment rails

- Fintech firms are embedding stablecoins into payment APIs

The shift is subtle but profound:

Stablecoins are evolving from assets into infrastructure layers.

Regulation: The Catalyst for Institutional Confidence

One of the biggest barriers to adoption has been regulatory uncertainty.

That is now changing.

In the United States, the GENIUS Act established:

- 1:1 backing requirements (cash or short-term U.S. Treasuries)

- Mandatory disclosures

- Federal oversight

Other regions—EU, Singapore, Hong Kong, UAE—are implementing similar frameworks.

This regulatory clarity is unlocking:

- Bank participation

- Institutional liquidity

- Enterprise integration

The Dollar Effect: Stablecoins as Digital Dollar Expansion

Most stablecoins are denominated in U.S. dollars.

If adoption continues, this implies a powerful macro consequence:

Stablecoins may extend the global dominance of the U.S. dollar into the digital era.

Even as concerns grow about long-term dollar hegemony, stablecoins could paradoxically reinforce it.

Druckenmiller himself hinted at this tension—acknowledging both the risks to the dollar and its potential digital resurgence.

Challenges: Why the Transition Is Not Yet Complete

Despite rapid growth, several barriers remain:

1. Merchant Adoption

Retail acceptance is still limited compared to traditional payment methods.

2. User Experience

Wallet management, private keys, and blockchain interactions remain complex for average users.

3. Regulatory Fragmentation

Global standards are still evolving, especially around custody and compliance.

4. Security Concerns

Risks include:

- Smart contract vulnerabilities

- Custodial failures

- Compliance breaches

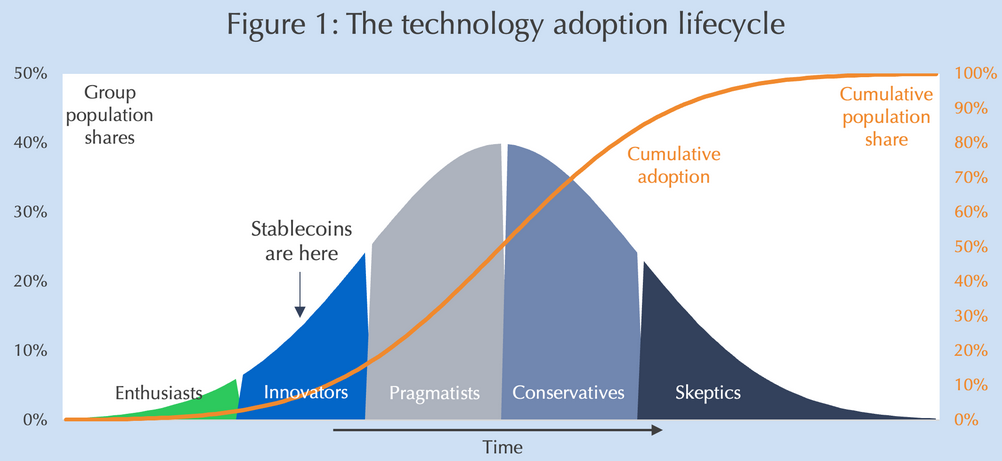

Future Outlook: A 10–15 Year Transformation

Druckenmiller’s timeline—10 to 15 years—is ambitious but plausible.

The trajectory suggests three phases:

- Current Phase (Infrastructure Build-Out)

Stablecoins dominate crypto-native activity - Expansion Phase (Enterprise Integration)

Businesses adopt stablecoins for treasury and payments - Maturity Phase (Consumer Adoption)

Stablecoins become invisible backend infrastructure

(Diagram: Evolution of Stablecoin Adoption Phases)

Conclusion: From Speculation to Infrastructure

Stablecoins are no longer a niche component of the crypto ecosystem.

They are emerging as a core layer of global financial infrastructure.

What makes this shift particularly significant is not just the technology—but who is recognizing it.

When a veteran macro investor like Stanley Druckenmiller signals that stablecoins could reshape global payments, it reflects a broader institutional awakening.

The key takeaway is clear:

The future of crypto may not be about volatility—it may be about efficiency.

And in that future, stablecoins are positioned not as speculative bets, but as the rails upon which the next generation of finance will run.