Main Points:

- Legal Finality: Appeals Withdrawn, 2023 Ruling Stands — The SEC and Ripple have mutually dismissed their appeals in the Second Circuit, effectively ending the five-year battle and leaving Judge Analisa Torres’s 2023 split decision in place.

- XRP’s Status for Retail — Programmatic (exchange) sales of XRP are not investment contracts under Howey; sales to institutions without proper disclosures were illegal securities sales.

- Remedies That Remain — A permanent injunction on certain institutional sales and a $125 million civil penalty remain after a judge rejected a joint bid to soften them in June 2025.

- Macro Tailwinds: Stablecoin Law in the U.S. — The new federal stablecoin law (the “GENIUS Act”) sets reserve and disclosure rules and signals mainstream adoption—relevant to Ripple’s RLUSD strategy.

- Ripple’s Expansion: RLUSD + M&A — Ripple launched RLUSD in late 2024, integrated it into Ripple Payments in 2025, bought Hidden Road ($1.25B) and agreed to acquire Rail ($200M) to scale stablecoin settlement rails.

- Institutions Arrive: CME XRP Futures — CME launched XRP futures in May 2025, adding regulated hedging and price discovery that may deepen liquidity.

- Actionable Opportunities — Cross-border SME payments, RLUSD-denominated merchant settlement, on-chain treasury/payroll, and market-making/derivatives are the near-term, $-denominated revenue avenues builders can pursue now.

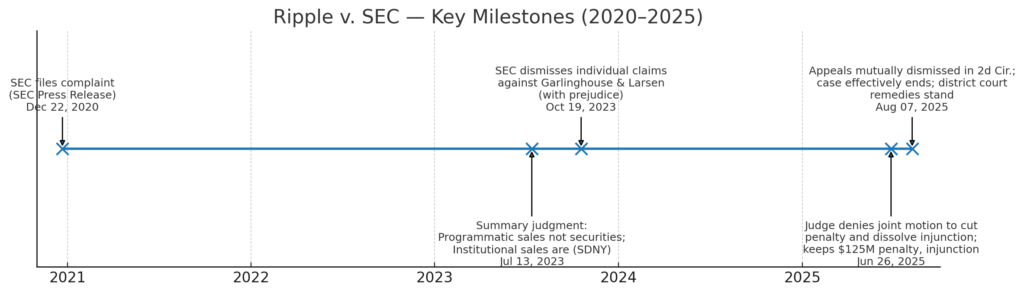

[Insert Figure 1: Ripple v. SEC — Key Milestones (2020–2025) here.]

What just happened—and why it matters

On August 7–8, 2025 (UTC), Ripple Labs and the U.S. Securities and Exchange Commission filed a joint stipulation to dismiss their respective appeals at the U.S. Court of Appeals for the Second Circuit. That filing ends the appellate fight and cements the district court’s split judgment as the operative law for this case: XRP’s programmatic sales on public exchanges were not securities transactions, while Ripple’s institutional sales violated securities laws. In short, the Torres framework stands—and the case is closed.

The closure follows a turbulent remedies phase. In June 2025, Judge Torres declined a joint request from Ripple and the SEC to relax a permanent injunction and cut the civil penalty from $125 million to $50 million. The court left both the injunction and the $125 million penalty intact—now the last word, with appeals withdrawn.

The immediate market reaction was positive: XRP rallied around the headlines, as traders priced in an end to legal overhang and the prospect of steadier U.S. liquidity.

The law that now governs XRP (for this case)

In July 2023, Judge Analisa Torres applied Howey to different categories of XRP distributions. She held that programmatic sales via blind bid/ask mechanisms on exchanges did not satisfy the investment-contract test, while sales directly to institutions did. That split ruling—criticized by some and celebrated by others—now remains the final word of this litigation due to the mutual dismissal of appeals.

For builders and exchanges, the practical implication is subtle but meaningful: secondary-market trading of XRP by retail users on exchanges did not, on these facts, constitute securities transactions. But primary, bespoke institutional deals require robust compliance. That line—programmatic vs. institutional—will shape how issuers structure future distributions and how counterparties paper transactions.

New policy backdrop: the U.S. stablecoin law

The U.S. just enacted a federal stablecoin statute (the “GENIUS Act”), requiring high-quality liquid reserves, monthly public attestations, and establishing a pathway for regulated issuance. That single policy shift dramatically improves legal certainty for dollar-pegged tokens—precisely where Ripple is leaning with RLUSD and its payments business.

This is crucial context for interpreting Ripple’s M&A spree: a $1.25 billion agreement to acquire multi-asset prime broker Hidden Road (April 2025) and this week’s agreement to acquire stablecoin payments platform Rail for $200 million. These deals—pending approvals—bolster institutional connectivity and stablecoin settlement capabilities across cross-border flows.

Ripple’s product posture: RLUSD + Ripple Payments

Ripple announced RLUSD in 2024 and integrated it into Ripple Payments in April 2025, citing rising enterprise demand. A compliant, attested, dollar-backed token that runs natively on the XRP Ledger and Ethereum can reduce FX leakage, shrink settlement windows, and enable always-on treasury rails for corporates. With a federal law now in place, U.S. banks and fintechs have clearer rules of the road to support RLUSD flows—subject to their own risk appetites and supervisory expectations.

Institutions get instruments: CME XRP futures

Another pillar of institutionalization: CME launched XRP futures in May 2025. Regulated, cash-settled contracts add hedging tools for market makers, exchanges, and corporate treasurers with XRP exposure. They also enhance price discovery and can draw in systematic flows familiar with CME’s benchmarks, potentially dampening volatility and improving liquidity over time.

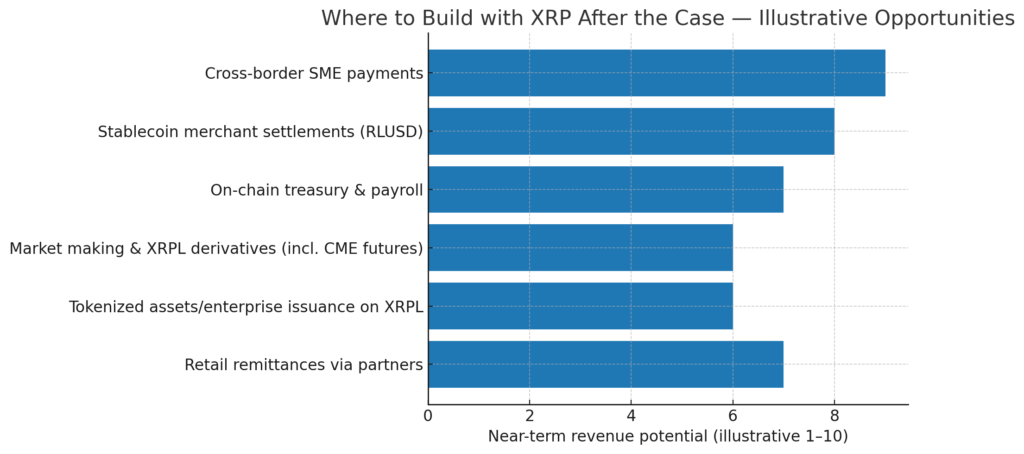

Where the opportunities are now (and how to monetize them)

[Insert Figure 2: Where to Build with XRP After the Case — Illustrative Opportunities here.]

1) Cross-border SME payments (near-term leader)

Mid-market corporates and marketplaces increasingly need sub-$50,000, high-frequency payouts across corridors where correspondent banking is expensive and slow. With legal overhang removed and RLUSD in the arsenal, providers can bundle XRP for liquidity and RLUSD for settlement to deliver lower FX spread + faster finality. Think automated supplier payouts, marketplace seller settlements, and ad-network remittances. Revenue: per-transaction spreads ($), subscription for treasury APIs ($), and float from operational balances (within new rules).

2) RLUSD-denominated merchant settlement

U.S. stablecoin law clarifies the reserve and disclosure regime. RLUSD can anchor merchant acquiring in e-commerce and cross-border card-not-present flows, with instant settlement to suppliers. Combine chargeback-resistant invoicing, programmable disbursements, and compliance guardrails. Monetization: basis-point interchange-like fees and SaaS for settlement dashboards (all $-denominated).

3) On-chain treasury & payroll

Finance teams want 24/7 liquidity, predictable fees, and automated controls. RLUSD on XRPL/Ethereum plus CME futures for hedging can support T+0 cash pooling, payroll in multiple currencies via stablecoins, and supplier financing. Value: API access fees, per-payment fees, and embedded FX. (Note: Institutional XRP sales remain subject to the injunction; structure flows as secondary-market liquidity plus regulated stablecoins.)

4) Market-making & derivatives strategy

The CME futures curve lets professional traders hedge inventory and run basis trades; exchanges can offer tighter spreads; treasury desks can dynamically manage exposure. Add regulated custody and a compliance wrapper, and you can pitch liquidity services to token issuers and venues that list XRP pairs.

5) Tokenized assets and enterprise issuance on XRPL

XRPL’s low fees and finality make it a practical ledger for tokenized invoices, loyalty points, and B2B settlement coupons. Ledger-level reserve reductions in late 2024 also improved usability (lower minimums to maintain accounts/objects), trimming onboarding friction for at-scale programs.

6) Retail remittances with bank/fintech partners

XRP’s deep exchange liquidity, combined with RLUSD cash-out, supports remittance operators targeting corridors in APAC, MENA, and LatAm. The compliance lift remains non-trivial (sanctions, travel rule, consumer protection), but the economics and speed can beat legacy rails for small values. Pricing can remain in $, with explicit FX markups.

Implementation pointers (builders + investors)

- Separate programmatic from primary: When designing issuance or sales, keep the Torres split in mind. Secondary-market liquidity and RLUSD-based settlement rails reduce legal risk for retail flows; bespoke institutional placements require careful securities analysis and may be barred by the injunction.

- Lean into stablecoin-first flows: The new U.S. law makes RLUSD-denominated settlements and B2B payables viable for mainstream treasuries—subject to KYC/AML and counterparties’ policies. Centralize audits, attestations, and reporting to enterprise standards.

- Use CME futures for risk: If you warehouse XRP (e.g., for market-making), hedge directionally with regulated futures and pass on the tighter spreads to clients.

- Regulatory portability: Map U.S. clarity to other hubs (EU, UK, HK, SG). Some jurisdictions (e.g., Hong Kong) are tightening KYC around stablecoins; design your product’s compliance envelope for the strictest regime you plan to serve.

The timeline in focus

Figure 1 (above) charts the case from Dec 22, 2020 (SEC complaint) through Jul 13, 2023 (summary judgment), Oct 19, 2023 (dismissal of individual claims with prejudice), Jun 26, 2025 (judge denies attempt to soften remedies) and Aug 7, 2025 (mutual dismissal of appeals). The figure is meant for board decks and investor memos; feel free to reuse it.

Market structure: what changes next

With legal finality, U.S. exchanges and prime brokers can plan beyond quarter-to-quarter litigation risks. Two dynamics to watch:

- Liquidity depth and derivatives basis — CME futures provide a standardized, CFTC-regulated hedge. If open interest grows, the spot-futures basis can anchor more sophisticated liquidity strategies around XRP, reducing volatility spikes around headlines.

- Stablecoin settlement in the enterprise — The U.S. law hits the two pain points—reserves and transparency. That unlocks procurement, payroll, and cross-border payables where finance chiefs insist on clear rules and monthly attestations. Ripple’s Rail acquisition, once closed, squarely targets this enterprise settlement stack.

What to watch (next 3–6 months)

- Post-judgment compliance — Expect Ripple to continue operating under the injunction’s constraints for institutional transactions; monitor for updated disclosures and controls.

- Bank connectivity — RLUSD’s bank partners, attestation cadence, and integration into treasury systems will be a leading indicator of mainstream adoption.

- Derivatives adoption — CME XRP futures volumes and OI will telegraph whether institutions are truly committing capital to the asset class.

- Global policy — As the U.S. clarifies stablecoins, other jurisdictions will respond—some looser, some tighter; product teams should build modular compliance for swift localization.

Conclusion

By withdrawing their appeals, Ripple and the SEC have ended one of crypto’s defining court battles. The district court’s 2023 reasoning now frames XRP’s legal posture for this case: retail exchange trading is outside Howey’s investment-contract zone on these facts, while unregistered institutional sales drew sanctions and a lasting injunction. That clarity—combined with a federal stablecoin law, CME-listed XRP futures, and Ripple’s RLUSD-centric M&A—creates a pragmatic runway for builders and treasurers.

For readers hunting new assets, the signal is institutionalization: regulated derivatives, stablecoin-based settlement, and compliant secondary-market liquidity. For those seeking new revenue, think like a payments company: monetize per-transaction spreads in $, treasury APIs in $, and premium enterprise workflows in $—with XRP and RLUSD doing the heavy lifting under clearer rules.