Main Points :

- RWA (Real-World Assets) are emerging as the next dominant narrative in crypto

- DeFi yields are declining, pushing capital toward stable, off-chain-backed returns

- Yield distribution is currently “barbelled” between low-risk and high-risk extremes

- Mid-tier RWA products (corporate bonds, CLOs) could unlock institutional scale

- Risk management—not yield—is now the core competitive advantage

- Security threats are shifting toward human-layer exploits

- Regulatory alignment (e.g., FINMA) will define the next phase of growth

1. From DeFi Fatigue to RWA Momentum

The cryptocurrency industry is entering a new phase—one defined less by speculative token appreciation and more by sustainable yield generation. Over the past cycle, decentralized finance (DeFi) promised high returns through lending, liquidity provision, and algorithmic strategies. However, as market volatility normalized and arbitrage opportunities compressed, yields across major protocols declined significantly.

This structural shift is now driving capital toward Real-World Assets (RWA), a sector that bridges traditional finance and blockchain infrastructure. RWAs refer to tokenized representations of assets such as U.S. Treasury bills, corporate bonds, real estate, and private credit. Unlike purely crypto-native yields, these assets derive returns from underlying economic activity in the real world.

For investors seeking stable income streams—especially institutions—this is a critical evolution. RWAs offer something DeFi increasingly cannot: predictable, non-correlated yield.

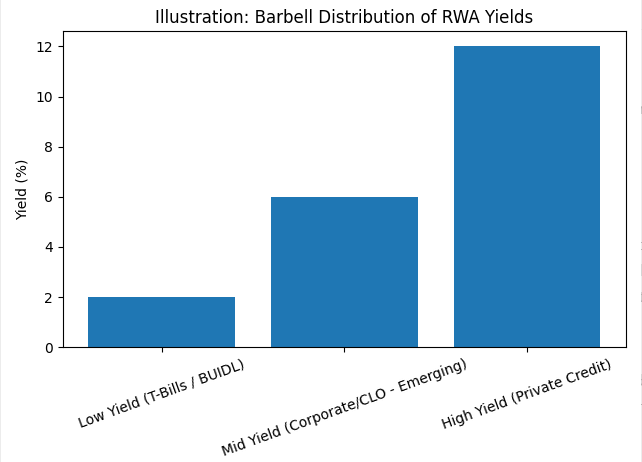

2. The Barbell Problem in Crypto Yields

A key observation highlighted by industry practitioners is the “barbell” distribution of current yields in the crypto ecosystem.

On one side, we have highly liquid, low-yield instruments such as tokenized Treasury funds (e.g., BlackRock’s BUIDL), offering stability but limited upside. On the other side lies high-yield, opaque risk exposure—primarily tokenized private credit with long durations and uncertain default risk.

What is missing is the middle.

This “middle layer” includes short-duration corporate bonds and structured credit products such as Collateralized Loan Obligations (CLOs). These instruments, if properly tokenized and made transparent, could deliver attractive yields without excessive risk. More importantly, they align closely with institutional portfolio construction models.

The absence of this middle tier is currently one of the biggest inefficiencies in crypto capital markets.

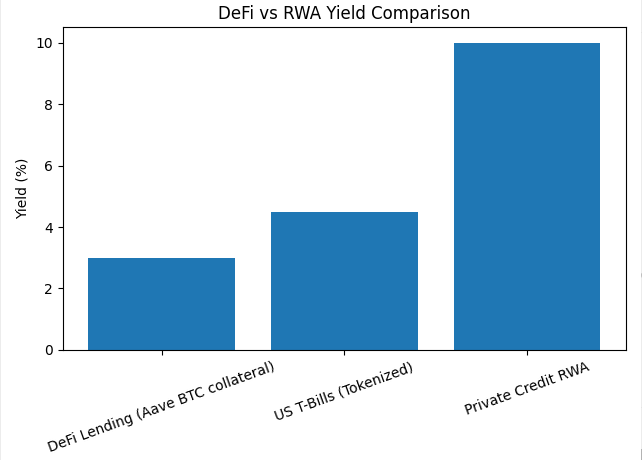

3. DeFi vs RWA: A Yield Reality Check

Consider a practical comparison: lending Bitcoin as collateral on platforms like Aave typically yields around 3%. This is roughly comparable—or even inferior—to tokenized U.S. Treasury bills, which offer similar liquidity with lower risk.

This raises a fundamental question: why should capital remain in DeFi if traditional assets can be accessed on-chain with better risk-adjusted returns?

This is the core driver behind the RWA narrative. Investors are no longer chasing yield blindly; they are optimizing for risk-adjusted efficiency.

4. Infrastructure Evolution: Vaults, Verification, and Strategy Control

To support this transition, new infrastructure is emerging.

One notable innovation is the cross-chain vault model, which integrates:

- On-chain accounting

- Hub-and-spoke asset routing

- Smart contract-enforced strategy constraints

These systems allow for verifiable Net Asset Value (NAV) calculations and reduce “strategy drift”—a major risk in actively managed DeFi strategies.

The importance of this cannot be overstated. Institutional capital requires transparency, auditability, and control. Without these features, large-scale adoption is impossible.

5. The New Alpha: Risk Management Over Yield

Perhaps the most important shift in the industry is philosophical: alpha is no longer generated primarily through yield, but through risk management.

Leading asset managers now allocate up to 80–90% of their operational resources to monitoring and mitigating risk. This includes:

- Real-time exposure tracking

- Counterparty risk analysis

- Liquidity stress testing

- Protocol-level monitoring

A recent example illustrates this well: a vault strategy identified excessive exposure to a specific lending pathway and exited the position before the underlying platforms collapsed.

This is not luck—it is infrastructure-driven risk awareness.

In the next phase of crypto, the winners will not be those who chase the highest yield, but those who avoid catastrophic losses.

6. Security: The Weakest Link is Human

While smart contract security has improved significantly, attackers are increasingly targeting the human layer.

One notable case involved an attacker posing as a hedge fund over several months, building trust with developers before ultimately compromising a multi-signature signing environment through social engineering.

This highlights a crucial reality:

No smart contract can protect against compromised keys.

As a result, institutional-grade security must now include:

- Operational security (OpSec)

- Device isolation for signing environments

- Behavioral monitoring of counterparties

- Multi-layer authentication beyond cryptography

Security is no longer just a technical problem—it is an organizational one.

7. Institutionalization and Regulation: The FINMA Path

Regulatory alignment is the next major catalyst.

Asset managers are increasingly pursuing licenses from regulators such as Switzerland’s FINMA. This move signals a transition from experimental DeFi strategies to fully compliant financial products.

The implications are significant:

- Access to institutional capital pools

- Ability to offer hedged products (e.g., CHF-denominated stablecoin strategies)

- Increased trust and credibility

This also aligns with broader global trends. Major financial institutions—including BlackRock, JPMorgan, and Franklin Templeton—are actively exploring tokenized asset platforms.

The convergence of traditional finance and blockchain is no longer theoretical—it is operational.

8. Market Outlook: Where the Opportunity Lies

Looking forward, several key trends are likely to define the RWA landscape:

1. Expansion of Tokenized Fixed Income

Short-duration corporate debt and structured products will fill the current “yield gap.”

2. Growth of On-Chain Asset Management

Vault-based strategies will become the standard for capital allocation.

3. Integration with Stablecoins

Stablecoins will serve as the primary settlement layer for RWA transactions.

4. Increased Institutional Participation

Regulatory clarity will unlock pension funds, sovereign wealth funds, and insurance capital.

5. Risk Infrastructure as a Service

Specialized platforms for risk monitoring will emerge as critical components of the ecosystem.

Conclusion: The Realignment of Crypto Value

The rise of Real-World Assets represents more than just a new trend—it is a fundamental realignment of what crypto is meant to achieve.

The first wave of crypto was about decentralization.

The second wave was about financial experimentation through DeFi.

The third wave—now unfolding—is about integration with the real economy.

For investors, this shift offers a new paradigm:

- Less speculation

- More stability

- Greater alignment with traditional finance

For builders, it presents a challenge:

- Can you create systems that meet institutional standards without sacrificing decentralization?

And for the industry as a whole, it raises a defining question:

Is crypto ready to become the infrastructure of global finance—or will it remain a parallel system?

The answer will determine where the next trillion dollars flows.