Main Points :

- U.S. banking regulator OCC has confirmed that national banks may intermediate crypto trades as riskless principal—a major step toward mainstream crypto brokerage.

- Banks can match customer buy and sell orders without holding crypto on their own balance sheets, reducing regulatory burden while expanding service offerings.

- The decision signals a reversal from the restrictive “Operation Chokepoint 2.0”-era posture toward crypto.

- Under the Trump administration’s 2025 policy pivot, federal regulators now promote smoother integration of digital assets into traditional banking.

- This development accelerates institutional crypto adoption, opens new revenue streams, and provides safer, regulated trading environments for customers.

- For investors exploring new crypto assets and income opportunities, bank-backed crypto markets may unlock liquidity, trust, and broader access.

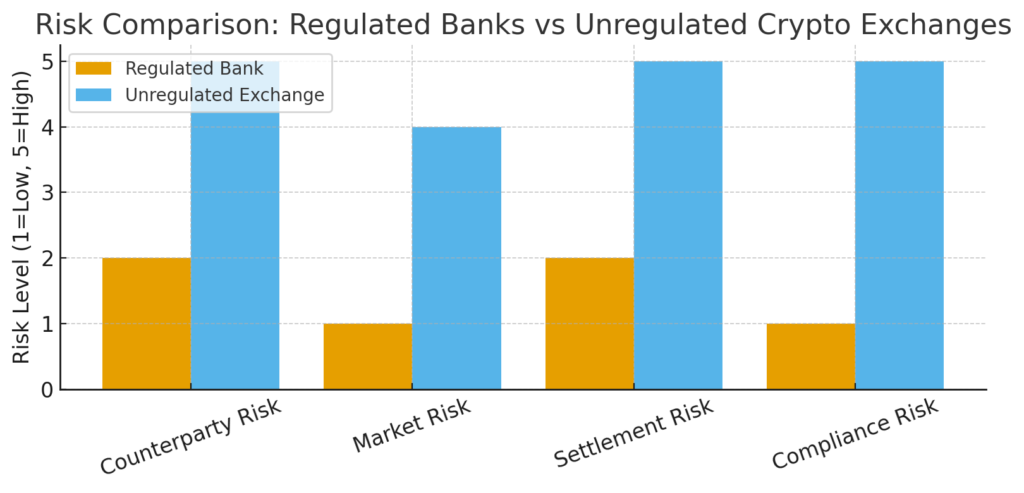

- Risk management—counterparty risk, settlement risk, and compliance controls—remains the foundation for banks entering crypto brokerage.

(Regulatory Timeline Chart)

Section 1: Introduction — A Watershed Moment for Crypto in the Banking Sector

In a landmark development, the U.S. Office of the Comptroller of the Currency (OCC) issued an interpretive letter confirming that national banks may legally facilitate cryptocurrency transactions as riskless principal. This means a bank may buy crypto from one customer and sell the same quantity to another customer at the same moment—essentially acting as a matched intermediary without taking market risk.

This interpretation aligns crypto brokerage with long-established practices in traditional financial markets. More importantly, it positions regulated banks as secure gateways for crypto investors seeking safer alternatives to offshore exchanges, unlicensed brokers, or loosely regulated trading platforms.

For audiences actively searching for new digital assets, new revenue models, and practical blockchain applications, this OCC stance signals a more stable environment for institutional crypto products, custody services, swaps, managed portfolios, tokenized deposits, and other advanced financial instruments.

Section 2: What Riskless Principal Crypto Transactions Mean for Banks

A. Definition and Market Significance

In traditional finance, riskless principal trading allows a bank or broker to fill two offsetting client orders without carrying the asset on its balance sheet. Extending this to crypto markets dramatically transforms how digital assets may be bought and sold:

- Banks do not need to hold volatile cryptocurrencies.

- Market exposure remains close to zero.

- Customer transactions occur under a fully regulated banking environment.

- Banks may earn revenue through spreads, fees, and liquidity services.

As OCC states, this type of intermediation “falls squarely within the business of banking” under 12 U.S.C. §24.

B. Benefits for the Market

- Institutional trust: Customers gain the ability to trade through entities with strict compliance, capital requirements, cybersecurity oversight, and legal accountability.

- Better pricing & liquidity: Banks interacting across deeper liquidity pools may tighten spreads.

- Onboarding for new digital assets: Banks could support emerging tokens earlier in their lifecycle, particularly if regulatory clarity improves.

For crypto seekers and blockchain-focused operators, this creates a new funnel: bank-driven exposure to curated crypto assets.

Section 3: Compliance Expectations — What Banks Must Prove Before They Enter Crypto

OCC emphasizes that approval does not mean “free entry” into crypto activities; instead, banks must verify that each activity:

- Is legally permissible under bank powers.

- Fits their risk profile and internal controls.

- Maintains ongoing monitoring of compliance, operational, market, and settlement risks.

Key Risk Components

- Counterparty credit risk: The main risk in riskless principal trading, especially settlement finality.

- Market conduct risk: Ensuring transparency and fairness in execution.

- AML/KYC/Travel Rule compliance: Fully applicable, especially for trades exceeding thresholds (converted to USD as needed).

- Cybersecurity: Banks must secure their integration points with exchanges, custodians, or blockchain networks.

This is fundamentally aligned with how a VASP or EMI (such as WIBS) structures internal controls—except banks operate under heavier prudential supervision.

Section 4: Distinguishing Crypto From Securities — A Long-Standing Legal Boundary

The interpretive letter clarifies that if a cryptocurrency is classified as a security, its riskless principal trading has always been permissible under existing securities regulations. What’s new is:

- OCC explicitly extends this logic to non-security digital assets.

- This harmonizes crypto with legacy financial instruments.

- Banks gain a stronger legal basis to support broader digital asset activities without relying on the SEC’s classification battles.

This reduces uncertainty for banks considering support for new digital assets and tokens outside the securities definition.

Section 5: Policy Shift — From “Chokepoint 2.0” to Federal Support of Crypto

During the Biden era, industry groups criticized regulators for what was coined “Chokepoint 2.0”—actions perceived as discouraging banks from offering services to crypto companies.

But the landscape changed dramatically when President Donald Trump took office in January 2025 with explicit pro-crypto commitments:

- Support for federal crypto licensing frameworks

- Encouragement of bank participation

- Reduction of adversarial regulatory pressure

- Integration of digital assets into federal financial modernization plans

OCC’s announcement the day after Comptroller Jonathan Gould commented that crypto firms should be treated “the same as traditional financial institutions” highlights a deliberate federal strategy shift.

Institutional Impact

- Banks now feel safer entering crypto markets.

- Large financial institutions may accelerate tokenization projects.

- Payment companies and remittance operators gain clearer regulatory pathways.

For investors and innovators, this environment fosters new opportunities for staking-derived products, yield mechanisms, token issuance platforms, and cross-border stablecoin settlements.

Section 6: How This Affects Investors Seeking New Crypto Assets

A. Banks as Gateways to Emerging Tokens

Traditional banks historically adopt only mature assets (BTC, ETH). With regulatory clarity and lower risk barriers, banks may now explore:

- Curated altcoin offerings

- Institutional launchpads for compliant token projects

- Bank-backed liquidity pools for approved assets

- Tokenized real-world assets (RWAs), including U.S. Treasury-backed tokens

This creates a new path for emerging assets to gain legitimacy and early liquidity.

B. Enhanced Consumer Safety

Bank-facilitated crypto trading may reduce:

- Custodial risk from offshore exchanges

- Fraud and wash-trading common in unregulated platforms

- Counterparty risk

- Compliance uncertainty for cross-border transfers

In effect, it normalizes crypto investment the way ETFs normalized equity exposure.

C. New Revenue Models Enabled by Riskless Principal Operations

Potential bank revenue sources include:

- Trading spreads

- Transaction fees

- Premium execution services

- Integrated wealth management for digital assets

- Subscription-based analytics and advisory

- Stablecoin issuance or settlement services

For builders, exchanges, and fintech operators, this shift means new partnership models: API-based order routing, liquidity sharing, compliance outsourcing, or settlement integrations.

Section 7: Recent Market Developments from Other Sources

To strengthen the context, here are relevant movements in late 2024–2025:

1. BlackRock and Fidelity expanding institutional crypto products

Asset management giants continue to grow their BTC and ETH ETF ecosystems, creating demand for bank-grade settlement rails.

2. Global stablecoin regulation progress

The EU MiCA framework and Singapore’s MAS guidelines have accelerated competition in regulated stablecoin issuance. U.S. banks entering this arena may become issuers themselves.

3. Tokenized Treasury bills surpass $1.5B

RWAs remain the hottest institutional trend—banks are natural custodians for such tokenized instruments.

4. Exchange consolidation

Following compliance crackdowns, many mid-tier exchanges are merging or shutting down, increasing demand for regulated alternatives.

All these trends converge into one conclusion:

The OCC ruling is timely, necessary, and strategically aligned with global institutional adoption.

Section 8: Conclusion — Why OCC’s Decision Matters for the Future of Crypto

The OCC’s confirmation that national banks may act as riskless principals in crypto transactions represents a pivotal shift in U.S. financial regulation. It legitimizes crypto brokerage within the banking framework, strengthens customer protection, and accelerates the integration of digital assets into the core of financial services.

Combined with the Trump administration’s supportive stance, this opens a new chapter where:

- Banks can safely expand into digital assets.

- Consumers gain secure, regulated access to crypto.

- Emerging tokens find new routes to legitimacy.

- Fintech firms can partner with traditional institutions under clearer rules.

For readers exploring new crypto assets, revenue streams, or practical blockchain implementations, this regulatory milestone signals a profound expansion of opportunities in the months ahead.