Main Points :

- U.S. regulators including Financial Crimes Enforcement Network (FinCEN) and Office of Foreign Assets Control (OFAC) propose applying bank-level AML obligations to stablecoin issuers

- The framework is based on the GENIUS Act and aligns stablecoin issuers with traditional financial institutions

- Compliance costs are expected to rise, but institutional participation may accelerate

- The Federal Deposit Insurance Corporation (FDIC) is simultaneously tightening reserve and custody requirements

- The global stablecoin landscape is shifting toward regulated, institution-grade infrastructure

Introduction: A Turning Point for Stablecoins

The global cryptocurrency market is entering a decisive phase where regulatory clarity is no longer optional—it is foundational. The latest proposal from FinCEN and OFAC marks one of the most significant shifts in the evolution of digital assets, particularly for stablecoins, which have increasingly become the backbone of crypto liquidity and cross-border payments.

Stablecoins, once viewed as a relatively simple bridge between fiat currencies and digital assets, are now being repositioned as critical financial infrastructure. With this transformation comes heightened scrutiny. The United States, aiming to reinforce both financial integrity and geopolitical security, is now moving to impose full-scale Anti-Money Laundering (AML) and sanctions compliance obligations on stablecoin issuers.

This is not merely a regulatory update—it is a structural redesign of the digital financial system.

The Core Proposal: Bank-Level Compliance for Stablecoin Issuers

Under the proposed rule jointly issued by FinCEN and OFAC, permitted payment stablecoin issuers (PPSIs) will be treated as financial institutions under the Bank Secrecy Act (BSA). This classification carries profound implications.

Issuers will be required to implement:

- Comprehensive AML programs

- Real-time transaction monitoring systems

- Suspicious Activity Reporting (SAR) mechanisms

- Full sanctions screening aligned with OFAC requirements

- Ongoing cooperation with law enforcement agencies

In essence, stablecoin issuers will be expected to operate with the same level of compliance rigor as traditional banks.

This shift is grounded in the GENIUS Act, a legislative effort designed to formalize the role of stablecoins within the broader financial ecosystem. By embedding stablecoin issuers into the regulatory perimeter, the U.S. government aims to mitigate risks associated with illicit finance while legitimizing the sector.

Stablecoin Compliance Framework Evolution

(Create an image showing transition: “Unregulated → Light Compliance → Bank-Level AML Framework → Institutional Integration” with arrows indicating progression.)

Strategic Context: Why Now?

The timing of this proposal is not coincidental. It follows closely on the heels of the FDIC’s risk management framework released just one day prior, which emphasized stringent requirements for reserve backing and custody practices.

Together, these developments signal a coordinated effort across multiple U.S. regulatory bodies to establish a comprehensive governance structure for digital assets.

There are three key drivers behind this urgency:

1. National Security Concerns

Stablecoins, due to their speed and global accessibility, present potential channels for illicit finance. Ensuring compliance with sanctions regimes is a top priority.

2. Institutional Readiness

Major financial institutions have been cautiously exploring digital assets. However, a lack of regulatory clarity has been a barrier. This proposal aims to remove that uncertainty.

3. Global Competition

Other jurisdictions, including the EU with MiCA and regions in Asia, are advancing their own frameworks. The U.S. is positioning itself to maintain leadership in digital finance.

The Cost of Compliance: A Double-Edged Sword

While the benefits of regulatory clarity are evident, the cost implications for stablecoin issuers cannot be ignored.

Increased Operational Burden

Implementing bank-level AML systems requires significant investment in:

- Technology infrastructure

- Compliance personnel

- Legal advisory services

For smaller issuers, this could create barriers to entry or force consolidation within the market.

Margin Compression

Stablecoin issuers typically operate on thin margins, relying on reserve yield and transaction volume. Increased compliance costs could reduce profitability unless offset by scale.

However, this challenge also creates an opportunity.

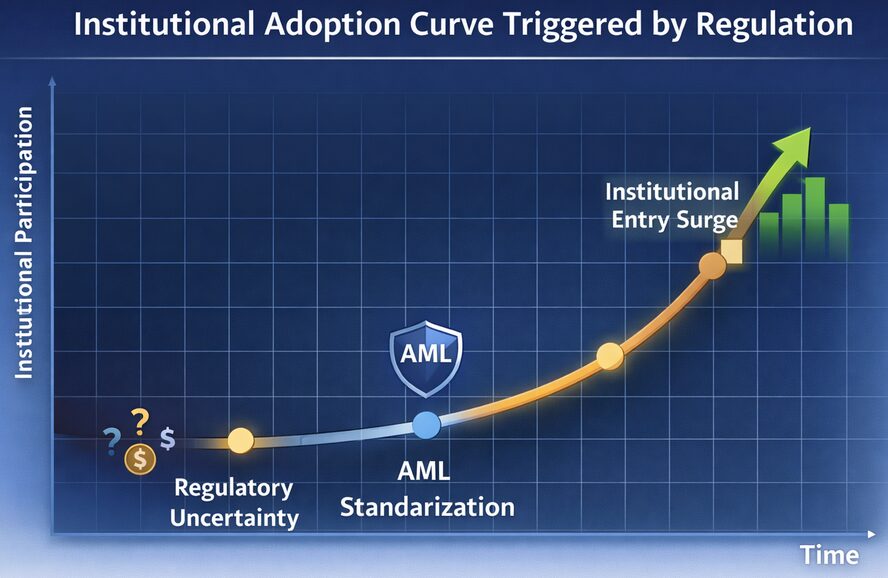

Institutional Capital: The Next Wave

One of the most important consequences of this regulatory shift is the potential influx of institutional capital.

Institutional investors—such as asset managers, banks, and sovereign funds—require robust compliance frameworks before entering any market. By aligning stablecoin issuers with traditional financial standards, regulators are effectively building the infrastructure necessary for large-scale participation.

This could lead to:

- Increased liquidity across crypto markets

- Greater price stability for digital assets

- Expansion of real-world asset (RWA) tokenization

- Growth in cross-border payment solutions

In this context, compliance is not merely a cost—it is an enabler of scale.

Institutional Adoption Curve Triggered by Regulation

(Graph showing X-axis: Time, Y-axis: Institutional Participation. Mark key points: “Regulatory Uncertainty,” “AML Standardization,” “Institutional Entry Surge.”)

Impact on the Global Stablecoin Ecosystem

The ripple effects of U.S. regulation will extend far beyond its borders.

Standardization of Compliance

Global issuers may adopt similar frameworks to maintain access to U.S. markets, effectively setting a new international standard.

Shift Toward “Regulated Stablecoins”

The market may increasingly differentiate between:

- Fully compliant, institution-grade stablecoins

- Unregulated or lightly regulated alternatives

This distinction could influence user trust and adoption patterns.

Competitive Pressure on DeFi

Decentralized finance (DeFi) platforms, which often rely on stablecoins, may face indirect pressure to enhance compliance mechanisms.

Recent Market Trends: A Converging Narrative

Recent developments across the crypto industry reinforce this regulatory trajectory:

- Major asset managers are expanding crypto ETF offerings

- Payment giants are integrating stablecoin settlement layers

- Central banks are accelerating CBDC research

- Tokenization of real-world assets is gaining momentum

Stablecoins sit at the center of all these trends.

The regulatory push from the U.S. can be seen as a foundational step toward integrating blockchain technology into the mainstream financial system.

Opportunities for Builders and Investors

For readers seeking new crypto assets and revenue opportunities, this shift presents several actionable insights:

1. Focus on Compliance-Ready Projects

Projects that proactively integrate AML and regulatory features are likely to attract institutional partnerships.

2. Infrastructure Plays

Opportunities exist in building tools for:

- Transaction monitoring

- Identity verification

- Risk scoring

These are essential components of the new financial stack.

3. Cross-Border Payment Solutions

Stablecoins with strong compliance frameworks are well-positioned to disrupt traditional remittance systems.

4. Tokenization Platforms

As regulation stabilizes, tokenized assets—from real estate to commodities—could see accelerated adoption.

Conclusion: From Experimentation to Infrastructure

The proposal by FinCEN and OFAC represents more than a regulatory adjustment—it marks the transition of stablecoins from experimental financial instruments to core infrastructure of the global economy.

By imposing bank-level AML and sanctions compliance, the United States is effectively drawing a line in the sand: the future of digital finance will be both innovative and regulated.

For market participants, the message is clear. The era of unchecked growth is ending, but in its place emerges a more mature, scalable, and institutionally integrated ecosystem.

Those who adapt early—by embracing compliance, building robust systems, and aligning with regulatory expectations—will be best positioned to lead in this new era.