Main Points :

- The Dutch House of Representatives has approved a proposal to impose a 36% tax on unrealized capital gains, including cryptocurrencies.

- The measure is designed to address an estimated $260 million fiscal shortfall (converted from €240 million).

- If enacted, long-term compounding could be significantly impaired, reducing projected retirement portfolios by over $1.5 million equivalent in long-horizon scenarios.

- Unrealized losses would only be offset against future gains, creating liquidity and timing risks.

- The proposal raises broader global questions: Will mark-to-market taxation spread to other EU states? What does this mean for crypto investors, founders, and capital mobility?

- For crypto participants, this may accelerate structural migration toward self-custody, tokenized real-world assets, and jurisdictional arbitrage strategies.

1. A Turning Point in European Tax Policy

In February 2026, the Dutch House of Representatives approved a proposal introducing a 36% tax on unrealized capital gains, explicitly including cryptocurrencies alongside equities and other assets. The measure now advances to the Senate, where the supporting coalition reportedly holds a majority, making final approval highly probable.

At first glance, the policy is framed as a fiscal correction. The Dutch government seeks to close a projected $260 million budget deficit. However, the structural implications extend far beyond short-term revenue stabilization.

Traditionally, most developed tax systems—including those in the United States, Germany, and Japan—tax capital gains upon realization. In other words, investors are taxed when they sell. The Dutch proposal shifts toward a mark-to-market framework: assets are revalued annually, and gains are taxed regardless of whether the investor has liquidated the position.

For cryptocurrency holders, this shift is particularly consequential. Crypto markets are volatile. Unrealized gains can fluctuate dramatically within a single quarter. Under a 36% mark-to-market system, investors could owe taxes on paper gains that later disappear.

This changes the fundamental incentive structure of long-term investing.

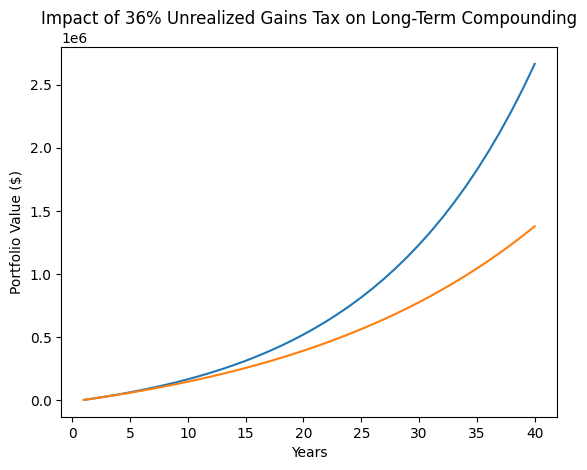

2. The Mathematics of Destroyed Compounding

One widely circulated projection demonstrates the magnitude of impact. Consider an investor who contributes approximately $1,080 per month (converted from €1,000) beginning at age 25 and continues for 40 years. Under a traditional tax-on-realization model, the projected portfolio could grow to roughly $3.6 million equivalent (converted from €3.32 million).

Under the proposed Dutch system, the final value could decline to approximately $2.0 million equivalent (converted from €1.88 million).

That represents a difference of more than $1.5 million equivalent over a lifetime.

[“Compounding Comparison Chart”]

Graph Description:

A line chart comparing two curves over 40 years:

- Blue Line: Tax on Realization (Traditional Model)

- Red Line: 36% Annual Unrealized Gain Tax

The divergence widens exponentially after year 20, illustrating how compounding is disproportionately damaged in later decades.

This is not merely a political argument. It is a mathematical one. Compounding is nonlinear. Taxing annual appreciation effectively truncates exponential growth.

For readers focused on building wealth through digital assets, staking yields, tokenized equity, or long-horizon Bitcoin exposure, this represents a structural compression of expected outcomes.

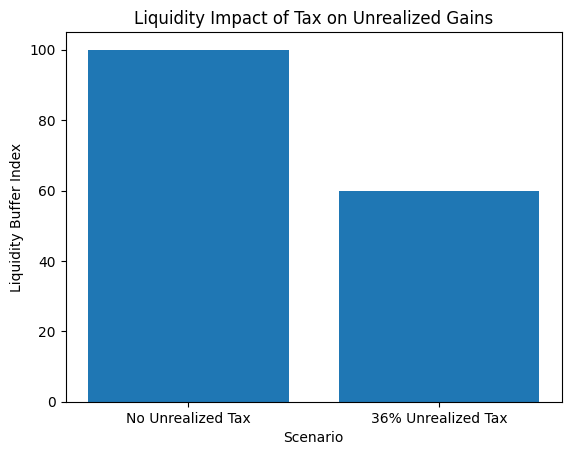

3. Liquidity Risk: The Forced-Sale Problem

The proposal includes provisions allowing unrealized losses to offset future gains. However, those losses cannot be immediately refunded in cash. They can only reduce future tax liabilities.

This asymmetry creates liquidity risk.

Imagine a crypto investor holding $500,000 in Bitcoin that appreciates to $800,000 during a bull cycle. A 36% tax on the $300,000 unrealized gain would require $108,000 in tax—even if no coins were sold.

To meet the obligation, the investor may be forced to liquidate part of the position. If the market subsequently corrects, the investor could suffer:

- Realized liquidation losses

- Reduced future upside exposure

- Limited ability to recover tax paid

This transforms volatility into a tax accelerant.

[“Forced Sale Flow Diagram”]

Diagram Description:

- Asset Appreciation

- Unrealized Gain Tax Assessment

- Tax Payment Required

- Partial Asset Liquidation

- Reduced Exposure During Recovery Phase

The structure penalizes illiquid and high-volatility assets more severely than stable ones. Cryptocurrencies, early-stage tokens, venture equity, and even tokenized real-world assets would be disproportionately impacted.

4. Capital Mobility and Jurisdictional Arbitrage

Experts have warned that such taxation could incentivize capital flight. The Netherlands has historically been viewed as business-friendly within the EU. Introducing aggressive mark-to-market taxation risks repositioning it as hostile to long-term capital accumulation.

In the crypto sector, capital mobility is not theoretical—it is operational.

High-net-worth individuals, founders, and even DAO participants can relocate with relative ease. We have already seen migration patterns:

- From China to Singapore (post-crypto ban)

- From the UK to Dubai (post-regulatory tightening)

- From the United States to Puerto Rico (tax incentives)

If enacted, the Dutch model could accelerate European internal migration toward:

- Portugal (if favorable regimes persist)

- Switzerland (crypto valley ecosystem)

- UAE free zones

For builders and investors seeking regulatory clarity, jurisdictional stability becomes a competitive advantage.

5. Implications for Crypto Strategy

For readers exploring new digital assets and income models, the question is strategic rather than ideological:

How should portfolios adapt?

A. Increased Appeal of Yield-Based Structures

If appreciation is taxed annually, yield-bearing structures (staking, DeFi lending, tokenized treasury bills) may gain relative attractiveness. The rationale: if taxes are unavoidable, generating cash flow to cover liabilities becomes essential.

B. Tokenized Real-World Assets (RWA)

RWA platforms issuing tokenized bonds, real estate cash flows, or structured products could gain traction. Income-producing assets provide liquidity to meet tax obligations without forced principal liquidation.

C. Corporate Wrappers and Holding Structures

Professional investors may increasingly use:

- Investment holding companies

- Jurisdictionally optimized SPVs

- On-chain DAOs with geographic flexibility

This shifts crypto from a retail-dominated narrative to a structurally engineered capital strategy.

6. Broader European and Global Context

While the Dutch proposal is advanced, it is not entirely isolated. Discussions around wealth taxation and unrealized gains have appeared in:

- U.S. political proposals targeting ultra-high-net-worth individuals

- European wealth tax debates

- OECD frameworks on global tax harmonization

However, full implementation at national scale remains rare.

If the Netherlands successfully enforces this without mass capital flight, other EU states may study it as a blueprint.

Conversely, if the policy leads to reduced investment inflows, startup relocation, and decreased asset ownership domestically, it may serve as a cautionary case.

7. A Structural Inflection Point for Long-Term Investors

The most profound impact is psychological and structural.

Long-term investing relies on:

- Time in the market

- Deferred taxation

- Compounding growth

Mark-to-market taxation interrupts that triangle.

For crypto holders, particularly those who view Bitcoin as digital property or Ethereum as programmable capital infrastructure, the proposal reframes ownership from long-term strategic allocation to annually taxed exposure.

The distinction matters.

Conclusion: Adaptation Over Reaction

The Dutch 36% unrealized gain tax proposal represents more than a domestic fiscal measure. It challenges one of the core mechanisms of capital formation: deferred compounding.

For cryptocurrency investors, founders, and capital allocators, the response should not be panic—but structural adaptation.

Key strategic considerations include:

- Jurisdictional diversification

- Income-generating digital assets

- Liquidity planning under mark-to-market frameworks

- Legal structuring of long-term holdings

If implemented, this policy may mark a shift toward a more surveillance-based, annually assessed financial system. In that world, blockchain’s transparency, portability, and programmability may paradoxically become even more valuable.

For those seeking new crypto assets, income opportunities, and practical blockchain applications, the message is clear:

Tax policy is becoming a market variable.

And in the coming decade, jurisdiction may matter as much as asset selection.