Main Points :

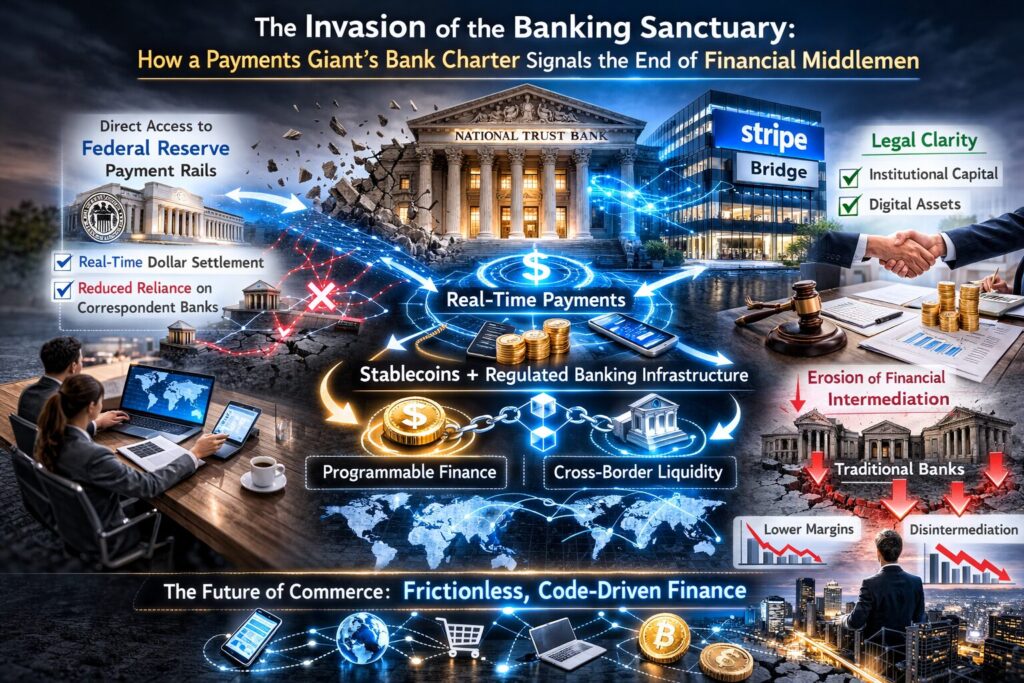

- Stripe’s subsidiary Bridge obtaining a U.S. national trust bank charter marks a structural shift in the balance of power between technology firms and traditional banks.

- Direct access to Federal Reserve payment rails enables real-time dollar settlement, reducing reliance on correspondent banking networks.

- The fusion of stablecoins and regulated banking infrastructure accelerates programmable finance and cross-border liquidity.

- Legal clarity removes barriers for institutional capital, opening the floodgates for large-scale digital asset integration.

- The long-term consequence is the erosion of financial intermediation margins and the emergence of frictionless, code-driven commerce.

1. Silicon Valley Hacks Sovereign Credit: The Inevitability of Banking Privilege Collapse

Stripe, long recognized as one of the most influential payment infrastructure companies in the world, has crossed a symbolic and strategic Rubicon. Through its subsidiary Bridge, it has secured approval to establish a U.S. national trust bank. This is not merely a regulatory milestone; it is a tectonic shift in the architecture of finance.

For decades, Silicon Valley firms operated at the periphery of banking. They optimized user experience, simplified checkout flows, and built APIs that wrapped around the fortress walls of regulated financial institutions. They innovated—but always outside the core monetary engine. The sovereign privilege of money creation, settlement, and custodianship remained inside the banking citadel.

With a national trust bank charter, that boundary dissolves.

A trust bank charter provides direct access to payment systems and the legal framework required to custody digital assets and hold reserves. In practical terms, this means Stripe can embed programmable finance inside a regulated banking entity. Instead of relying entirely on partner banks, it can integrate core financial functions directly into its technological stack.

Traditional banks historically relied on complexity, opaque fee structures, and multi-layered correspondent networks to sustain profit margins. Cross-border payments could take days and cost significant percentages in spread and fees. These inefficiencies were not bugs; they were features of a system protected by regulatory moats.

But technology compounds faster than regulation.

Bridge’s charter represents a wedge driven into the sanctum of banking privilege. Code is now positioned not outside the fortress—but inside it. Programmable ledgers and API-based financial primitives begin to overwrite paper-based processes and legacy infrastructure.

This moment echoes broader financial history: when settlement times compress and intermediaries thin out, value accrues to infrastructure providers. Stripe’s move signals that the future battleground is not consumer apps but monetary plumbing.

The collapse of entry barriers is no longer theoretical. It is operational.

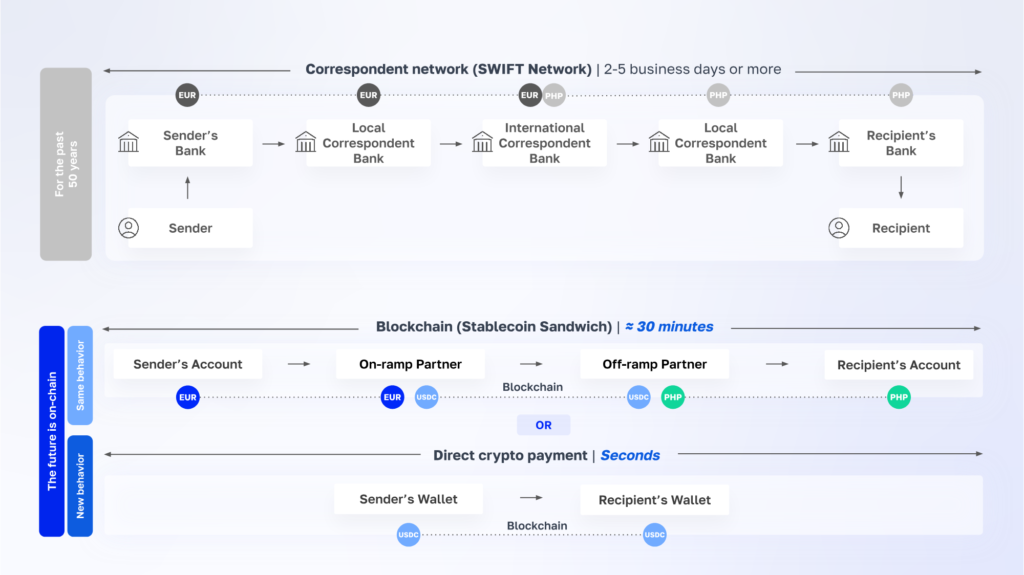

2. Real-Time Dollar Liquidity: The Shockwave to Legacy Remittance Systems

Access to Federal Reserve payment rails transforms Stripe from a payments processor into a liquidity orchestrator.

Historically, international transfers moved through correspondent banking chains. Bank A sends to Bank B via intermediary Bank C; each step extracts fees, imposes compliance checks, and adds settlement delay. A transfer of $100,000 could incur cumulative costs and take multiple business days.

Real-time settlement infrastructures—combined with stablecoins backed by dollar reserves—disrupt this chain.

When regulated entities issue or custody dollar-backed stablecoins, settlement no longer depends on interbank reconciliation. Funds can move at the speed of block confirmation or internal ledger updates. Cross-border commerce shifts from T+2 or T+3 timelines toward near-instant execution.

Below is a simplified comparison of legacy correspondent banking vs. real-time programmable settlement:

[Insert Figure 1 Here – “Legacy vs Real-Time Settlement Architecture Comparison”]

The efficiency delta is not incremental—it is structural. Corporations can automate payroll across jurisdictions, suppliers can receive funds instantly, and treasury management can become algorithmic.

For emerging markets and cross-border SMEs, the implications are enormous. Lower friction means tighter working capital cycles. Instead of tying up liquidity in transit, firms can deploy capital immediately.

For your audience—those exploring new crypto assets and blockchain applications—the critical insight is this: value migrates toward systems that eliminate friction. Whether through stablecoin infrastructure, Layer 2 networks, or tokenized deposits, the objective is identical—compress settlement time to near-zero.

Once users experience real-time global liquidity, reverting to legacy rails becomes economically irrational.

3. The Legal Breakwater Collapses: Institutional Capital Enters the Programmable Credit Era

The conditional approval granted by U.S. regulators is perhaps the most underappreciated catalyst.

Institutional investors historically cited regulatory uncertainty as the primary barrier to digital asset exposure. Questions around custody, reserve backing, systemic risk, and compliance created friction that discouraged large-scale participation.

When a regulated payments giant obtains a bank charter to integrate stablecoins and digital asset custody, it reframes the conversation. Digital assets cease to be fringe experiments; they become embedded within recognized financial infrastructure.

The impact unfolds in phases:

- Infrastructure Legitimization – Trust bank status provides institutional-grade custody and reserve management.

- Liquidity Expansion – Corporate treasuries gain confidence in programmable dollar instruments.

- Capital Inflow – Asset managers allocate toward tokenized deposits, stablecoin yield strategies, and blockchain settlement layers.

- Margin Compression – Traditional banks face erosion of cross-border and FX spread revenues.

Below is a conceptual capital flow model illustrating potential reallocation trends:

[Insert Figure 2 Here – “Projected Capital Flow Shift Toward Programmable Financial Infrastructure (2024–2028)”]

As legal clarity improves, capital follows. This pattern was visible in the ETF era for Bitcoin; it will repeat in payment and settlement infrastructure.

The deeper transformation is philosophical: credit becomes programmable.

Instead of manual approvals and siloed ledgers, smart contracts can enforce covenants. Instead of delayed reconciliation, transactions settle atomically. Instead of centralized gatekeeping, compliance can be embedded in code.

This does not eliminate regulation—it digitizes it.

Strategic Implications for Crypto Investors and Builders

For readers seeking new crypto assets and revenue streams, several actionable themes emerge:

1. Infrastructure Tokens Gain Strategic Value

Projects that provide settlement layers, interoperability, and compliance tooling stand to benefit as regulated entities integrate blockchain rails.

2. Stablecoin Ecosystems Expand

Dollar-backed stablecoins with transparent reserves and regulatory alignment will likely capture disproportionate transaction volume.

3. Tokenized Treasury and Yield Products

As real-time liquidity improves, programmable yield instruments—backed by short-duration assets—become attractive alternatives to idle capital.

4. Developer-Centric Financial APIs

The next wave of opportunity lies not in speculative tokens alone, but in programmable finance stacks that enterprises can integrate directly.

For fintech operators—especially those navigating EMI and VASP regulatory frameworks—the lesson is clear: regulatory compliance and technological innovation are no longer opposing forces. They are converging.

Conclusion: The First Strike of a New Financial Epoch

Stripe’s banking charter through Bridge is not a corporate footnote. It is the opening move in a broader campaign to redefine finance.

When technology companies gain lawful access to sovereign monetary rails, the distinction between “bank” and “platform” dissolves. Intermediation margins shrink. Settlement accelerates. Transparency increases.

The disappearance of middlemen is not ideological—it is mathematical. If friction can be removed, competition will remove it.

We are witnessing the early stages of a programmable trust era—one in which value moves as quickly as information, and credit is enforced by code rather than paperwork.

Those who adapt—investors, developers, institutions—will not merely survive the transformation; they will shape it.

The banking sanctuary has been breached. The shockwave has only just begun.