Main Points :

- Aon has completed the first insurance premium settlement using stablecoins, marking a milestone in the insurance industry.

- The transaction involved collaboration with Coinbase and Paxos, using USDC on Ethereum and PYUSD on Solana.

- Regulatory clarity in the United States, especially the GENIUS stablecoin legislation, helped accelerate experimentation.

- Geopolitical instability, including the U.S.–Iran conflict, has caused dramatic increases in maritime insurance premiums, highlighting inefficiencies in legacy settlement systems.

- Blockchain-based settlement could transform the insurance sector by improving speed, transparency, and global accessibility.

1. A Historic First: Stablecoin Premium Payments Enter the Insurance Industry

The global insurance industry has long been known for its conservative adoption of new technologies. Yet in March 2026, a major milestone occurred when the multinational insurance brokerage giant Aon announced that it had successfully completed the industry’s first insurance premium payment using stablecoins.

This payment was carried out in collaboration with major crypto infrastructure companies Coinbase and Paxos, two firms that have become central players in the regulated digital asset ecosystem. The settlement used USDC, a dollar-pegged stablecoin operating on the Ethereum blockchain, and PYUSD, another dollar-linked stablecoin issued by Paxos and operating on the Solana network.

By executing an insurance premium payment through blockchain-based digital dollars, the companies demonstrated that large-scale financial contracts traditionally handled through banking rails can now settle via decentralized networks.

For an industry built on risk management, actuarial modeling, and long-term financial commitments, the adoption of blockchain technology represents more than a technical experiment—it signals the potential start of a structural transformation in global insurance infrastructure.

The implications are enormous. Insurance premiums, especially for large corporate policies such as maritime shipping coverage, energy infrastructure protection, or aviation liability insurance, often involve multi-million-dollar settlements and complex international payment flows.

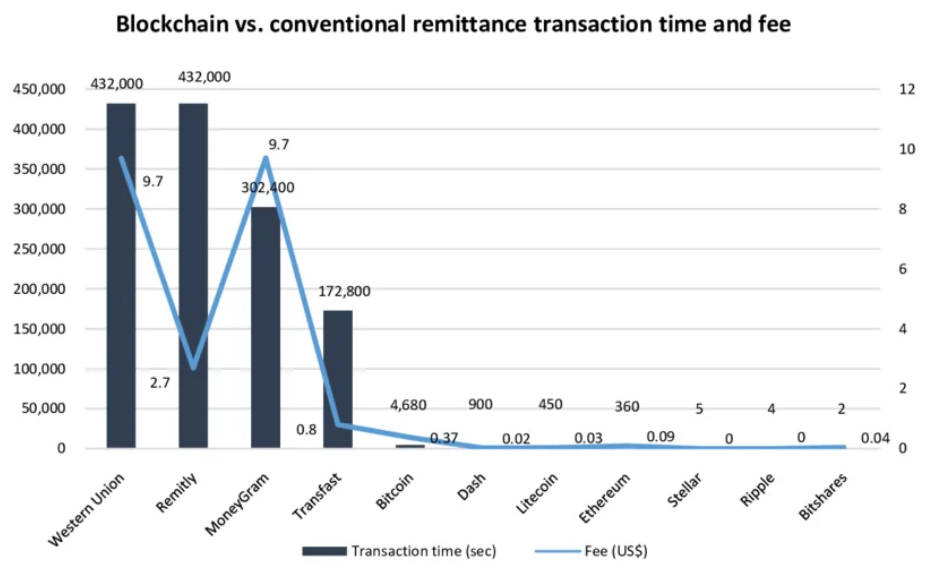

Historically, these payments have relied on traditional banking networks such as SWIFT. These networks can take days to process international transfers, incur high intermediary costs, and suffer from limited transparency.

Stablecoins, by contrast, allow near-instant settlement with full transaction traceability on public ledgers.

In this sense, Aon’s experiment represents a fundamental shift in how the insurance sector might operate in the coming decades.

2. The Role of Coinbase, Paxos, and Blockchain Infrastructure

The stablecoin payment executed by Aon involved two major digital dollar systems:

- USDC on Ethereum

- PYUSD on Solana

Both assets maintain a 1:1 peg to the U.S. dollar, meaning that $1 worth of stablecoin equals approximately $1 in fiat reserves.

The involvement of Coinbase and Paxos highlights an important trend in the crypto ecosystem: the institutionalization of blockchain infrastructure.

Coinbase has evolved from a retail cryptocurrency exchange into a comprehensive financial services platform offering custody, settlement, compliance, and payment infrastructure for institutional clients.

Paxos, meanwhile, has positioned itself as a regulated blockchain financial institution, specializing in the issuance of stablecoins and tokenized assets under regulatory oversight.

The collaboration between Aon, Coinbase, and Paxos demonstrates how traditional financial institutions increasingly rely on specialized crypto infrastructure providers rather than building blockchain systems internally.

From a technical standpoint, the use of both Ethereum and Solana networks also illustrates a growing multi-chain settlement environment.

Ethereum remains the dominant platform for institutional tokenized finance due to its mature developer ecosystem and security model. However, Solana offers significantly lower transaction fees and faster settlement speeds.

The coexistence of these networks suggests that the future of financial blockchain infrastructure will likely involve interoperable networks rather than a single dominant chain.

3. Regulatory Clarity: The Impact of the GENIUS Stablecoin Act

One of the major factors that enabled this experiment was regulatory progress in the United States.

In 2025, lawmakers passed the GENIUS Act, legislation designed to create a clear legal framework for stablecoin issuance and usage.

Before this legislation, the regulatory status of stablecoins was uncertain. Financial institutions faced legal risks related to compliance, custody, and reserve backing.

The GENIUS Act established guidelines covering several key areas:

- Reserve transparency requirements

- Licensing rules for stablecoin issuers

- Consumer protection measures

- Operational compliance standards

By clarifying the legal status of dollar-pegged digital assets, regulators effectively removed one of the largest barriers preventing traditional financial institutions from adopting blockchain payments.

This regulatory shift reflects a broader global trend.

Governments in regions such as the European Union, Singapore, the United Kingdom, and the United Arab Emirates have also begun introducing frameworks for digital assets and tokenized financial instruments.

As regulatory certainty increases, institutional adoption of blockchain infrastructure is accelerating.

4. Rising Insurance Costs and the Impact of Geopolitical Risk

The timing of Aon’s stablecoin settlement experiment is particularly significant given the current conditions in global insurance markets.

The U.S.–Iran conflict has recently escalated tensions in the Middle East, particularly around the Strait of Hormuz, one of the world’s most strategically important maritime chokepoints.

Approximately 20% of global oil shipments pass through this narrow waterway.

As military tensions rise, shipping companies face increasing risks of vessel attacks, seizures, or disruptions.

Insurance markets have responded by dramatically raising war-risk premiums for ships operating in the region.

In some cases, shipping insurance costs have reportedly increased by several hundred percent, creating significant pressure on global energy supply chains.

Because insurance premiums must often be paid quickly before vessels can enter high-risk zones, settlement speed becomes critically important.

Traditional banking transfers can delay payments for days.

Blockchain-based stablecoin settlements, however, can finalize transactions within minutes.

In a volatile geopolitical environment, this difference in speed can significantly impact shipping logistics and operational decision-making.

5. Stablecoins and the Future of Real-World Asset Finance

The adoption of stablecoins for insurance premiums is part of a much larger trend known as Real-World Asset (RWA) tokenization.

RWA tokenization refers to the process of representing traditional financial instruments—such as bonds, loans, commodities, or insurance contracts—on blockchain networks.

Over the past two years, this sector has expanded rapidly.

Major financial institutions including BlackRock, JPMorgan, Franklin Templeton, and Citi have begun exploring tokenized financial products.

Some examples include:

- Tokenized money market funds

- Blockchain-based bond issuance

- On-chain repo markets

- Tokenized treasury bills

The appeal of these systems lies in their ability to combine the transparency of blockchain with the legal structure of traditional finance.

Insurance contracts may be one of the next major asset classes to migrate onto blockchain rails.

The potential benefits include:

- Instant settlement

- Reduced operational costs

- Global payment accessibility

- Programmable risk contracts

For example, maritime insurance policies could eventually be represented as smart contracts that automatically trigger payouts when predefined conditions are met.

Satellite data, IoT sensors, and shipping logistics data could feed into these contracts in real time.

6. Remaining Challenges for Blockchain Insurance Infrastructure

Despite its promise, blockchain-based insurance settlement still faces several challenges.

Regulatory Fragmentation

While the United States and Europe have begun developing legal frameworks for digital assets, many countries still lack clear regulations.

Insurance contracts are heavily regulated, and cross-border payments must comply with multiple jurisdictions.

Market Scale

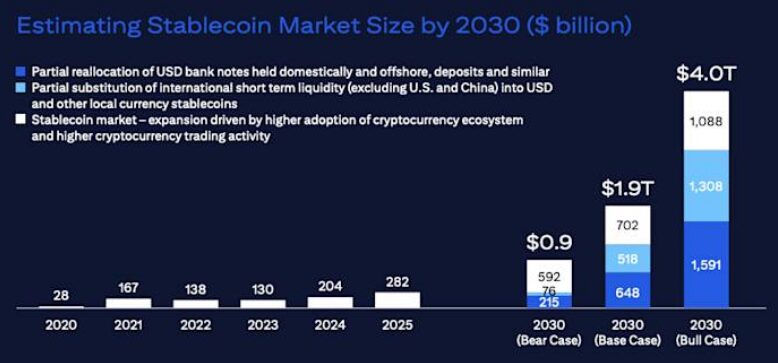

Current stablecoin markets are large—exceeding $150 billion globally—but insurance markets are vastly larger.

The global insurance industry generates over $7 trillion in annual premiums.

Scaling blockchain infrastructure to handle this volume will require further development.

Interoperability

Financial institutions currently operate across multiple blockchain networks.

Ensuring seamless interoperability between Ethereum, Solana, and other networks remains a technical challenge.

However, emerging technologies such as cross-chain bridges, token messaging protocols, and shared liquidity layers are beginning to address these issues.

7. A Glimpse into the Future of Insurance Payments

Aon’s stablecoin premium payment may appear small today, but it could represent the beginning of a major transformation.

If stablecoin payments become widely adopted, insurance markets could experience the same kind of technological disruption that fintech brought to banking.

Future insurance payments may occur entirely on blockchain networks, with policy issuance, premium payments, risk modeling, and claims processing all executed through programmable infrastructure.

The benefits could include:

- Faster settlement

- Lower transaction costs

- Global payment accessibility

- Increased financial transparency

For crypto investors and blockchain entrepreneurs, this development also highlights an important trend: the expansion of blockchain into traditional financial sectors.

As more industries adopt blockchain infrastructure, demand for stablecoins, decentralized finance protocols, and tokenized assets is likely to grow.

Conclusion

The successful completion of an insurance premium payment using stablecoins by Aon represents a landmark moment in the convergence of traditional finance and blockchain technology.

By leveraging USDC on Ethereum and PYUSD on Solana in collaboration with Coinbase and Paxos, the insurance industry has demonstrated that blockchain-based financial infrastructure is no longer theoretical—it is operational.

At the same time, geopolitical tensions and rising insurance costs highlight the need for faster and more efficient financial settlement systems.

Stablecoins offer a powerful solution by combining the stability of fiat currency with the speed and transparency of blockchain networks.

While challenges remain—including regulatory fragmentation, interoperability, and market scale—the trajectory is clear.

Blockchain technology is steadily moving beyond speculative cryptocurrency markets and entering the core infrastructure of global finance.

For investors, builders, and financial institutions alike, the message is unmistakable: the next phase of blockchain adoption will not merely involve digital assets—it will reshape how the world’s largest financial industries operate.