Key Takeaways :

- Public companies holding cryptocurrency treasuries (so-called “Bitcoin treasury firms”) have seen their Net Asset Values (NAVs) collapse, wiping out premiums once paid by investors.

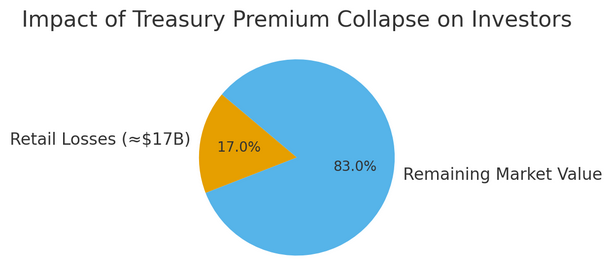

- Retail investors over-paid significantly: research from 10x Research estimates about US,$17 billion in losses.

- Firms such as Metaplanet (Japan) and Strategy (formerly MicroStrategy) exemplify the model breakdown: high share-issuance at inflated prices backed by limited actual Bitcoin holdings, followed by a sharp reset.

- The model is shifting: treasury companies must move from buying Bitcoin with over-valued equity to operating like arbitrage or trading firms, focusing on real yield rather than hype.

- For those new to crypto business models or seeking yield opportunities, this reset opens entry points into more disciplined treasury firms and signals that the landscape for blockchain-asset management is evolving.

1. The Illusion of the Treasury Premium

Companies that adopted the “Bitcoin treasury” strategy marketed themselves as ways to gain leveraged exposure to Bitcoin (BTC) by simply buying Bitcoin and reflecting it on their balance‐sheet. The mechanism often worked as follows: issue shares (or preferred stock), raise capital at a premium to the actual BTC holdings, then convert that raised capital into more BTC.

10x Research describes this phase as the “age of financial magic.” These firms “conjured billions in paper wealth by issuing shares far above their real Bitcoin value — until the illusion vanished.”

For example, Metaplanet once had a market cap of about US $8 billion while holding only about US $1 billion in Bitcoin. At peak hype, retail investors were said to pay 2× to 7× the value of the company’s actual Bitcoin holdings.

In effect, retail investors subsidised the corporate Bitcoin accumulation at their expense.

2. The Collapse: NAVs Normalize and Losses Mount

The problem: once the market shifted (lower volatility, diminished momentum, higher scrutiny), those large premiums could no longer be sustained. NAV (Net Asset Value) is defined here as: value of Bitcoin holdings / number of shares outstanding. If a firm issues shares at a huge premium over its actual BTC holdings, the share price reflects expectations rather than real backing.

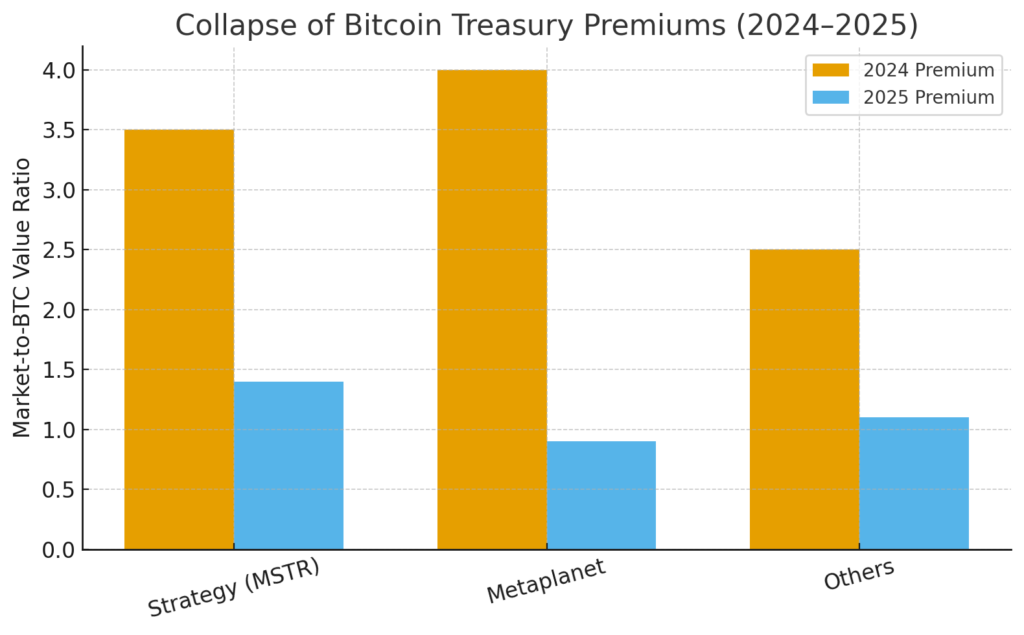

10x Research reports that this premium has collapsed across many Bitcoin-treasury firms:

- Retail investors have lost roughly US $17 billion chasing the high-premium shares.

- In some cases, market value of the firm fell below the Bitcoin value held — e.g., Metaplanet’s market cap fell to about US $3.1 billion while its BTC holdings rose to around US $3.3 billion, yielding an mNAV (market-to-Bitcoin holdings) ratio of ~0.99.

- Share prices of Strategy (MSTR) fell from highs around US $473.83 (November 2024) to around US $289.87 as of the report, a ~39 % drop.

The consequence: investors holding shares were hit hard, and companies that raised equity via the premium route now face diluted share bases and limited ability to issue more at elevated valuations.

3. Why This Matters for Crypto Practitioners and Seekers of New Yield

From hype-proxy to disciplined asset manager

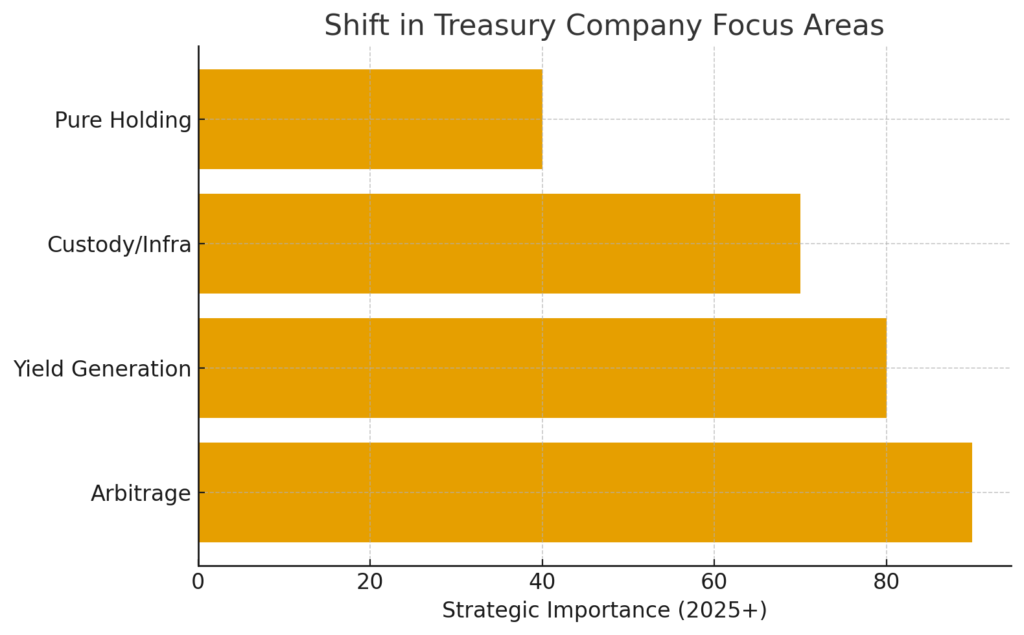

For those looking at blockchain, crypto assets or corporate treasuries as a potential new revenue source or strategic business model, the key takeaway is: the easy “buy Bitcoin and let the market do the work” model is fading. The firms that survive will be those that adapt. According to 10x Research:

“Bitcoin treasury firms should move away from buying Bitcoin at inflated NAVs and begin operating as asset arbitrage managers.”

What does that look like in practice?

- Focusing on arbitrage between crypto spot, futures, derivatives, or custody yield rather than just accumulation.

- Managing the balance sheet: issuance, dilution risk, cost of carry, operational overhead.

- Transparent governance and capital structure that justify trading or yield generation beyond mere Bitcoin accumulation.

- Acknowledging that the “premium-multiple” advantage is gone: the market now expects a near-1× or modest premium to Bitcoin holdings, not 3×-4×.

Opportunity for investors and innovators

For those researching new crypto projects, altcoins or blockchain use cases, the reset offers a clearing:

- Firms trading at or below Bitcoin-backing offer pure exposure to BTC with optional upside from operational alpha.

- Projects that previously piggy-backed on the treasury-model craze but lacked substance now face selection pressure, creating space for business models with deeper infrastructure or arbitrage focus.

- In terms of blockchain use, the era of “just buy Bitcoin and wait” is giving way to “use Bitcoin (and other crypto) plus trading, yield, strategy and active balance-sheet management.” That implies services around custody, derivatives, on-chain analytics, staking, arbitrage—areas where practical implementation matters.

4. Recent Developments & Emerging Trends

To enhance the original article’s “recent trend” layer, here are additional developments:

- The collapse of premiums coincides with slowing daily Bitcoin purchases by treasury firms: in September 2025 the average daily purchase by public treasury firms dropped to the lowest level since May.

- Some firms are hinting at new purchases: Strategy’s founder Michael Saylor posted a Bitcoin-tracker chart suggesting another accumulation of ~640,250 BTC (≈US $70 billion) … even when NAV pressures are high.

- European entry: In August 2025, Dutch crypto firm Amdax announced plans to launch a Bitcoin treasury company (AMBTS) aiming for at least 1 % of Bitcoin supply, to list on Euronext Amsterdam—underscoring institutional appetite despite the reset.

- Extended to other chains: Firms are now exploring treasury strategies beyond Bitcoin. Example: ETHZilla (formerly 180 Life Sciences) announced an Ether treasury strategy with ~US $350 million in ETH holdings.

- Academic work: Research indicates that firms holding crypto (like Strategy) expose investors to higher correlation with Bitcoin: one paper found average beta ~0.62 with some treasury firms exceeding beta >1 relative to BTC.

These trends suggest: although the treasury-model hype is over, there is still institutional interest; the business models are evolving; and the risks (and opportunities) shift from pure accumulation to execution, risk control, and alternative strategies.

5. What This Means for You: Strategy Recommendations

If you are interested in exploring new crypto assets, yield opportunities, or practical blockchain/treasury business, here are actionable takeaways:

- Do your due-diligence on treasury firms: If you are investing in or considering working with a company with “crypto treasury” in its model, check its NAV backing, share-issuance history, dilution risk, cost structure, and whether it has actual yield/trading operations rather than simple accumulation.

- Prefer firms trading at or below backing: With premiums collapsed, a company whose market cap is equal to or less than its crypto holdings may offer a cleaner value-entry, provided they have a viable business beyond HODL.

- Explore arbitrage and yield models: Instead of simply ownership of top coins, look at how companies or services generate income: trading spreads, derivatives, staking, lending, custody services, tokenized holdings, etc.

- Blockchain use-cases matter more than ever: In the wake of this reset, the value goes to operators who build infrastructure (custody, analytics, arbitrage engines) or leverage decentralised finance (DeFi) and on-chain mechanics—not just “we hold crypto on our balance sheet.”

- Consider alt‐coin treasury as strategic differentiation: As seen with ETHZilla and others, treasury strategies may expand beyond Bitcoin. Firms that anchor on other chains, or hybrid models (multi-chain treasury) may present differentiated value, but also higher risk.

- Be mindful of macro and market cycles: The collapse of premiums did not primarily come from Bitcoin dropping, but from market sentiment, issuance arbitrage exhaustion, and structural dilution. Crypto is still volatile; the business model now requires credible strategy rather than hope.

Summary

In summary, the era of easy profits for Bitcoin-treasury companies—where share issuances at large premiums funded massive Bitcoin accumulation—appears to have ended. The reset of NAVs has erased billions of dollars in shareholder value, transferred real Bitcoin into the hands of treasury firms (at the expense of retail investors), and exposed structural weaknesses in the model.

That said, this shift is not purely negative: it creates a more disciplined environment where the firms that adapt—those with strong capital, transparent governance, trading or arbitrage capability, yield generation, and real blockchain infrastructure—may define the next phase of crypto-treasury business. For practitioners and investors seeking new sources of revenue or looking to evaluate blockchain/treasury opportunities, the message is clear: focus on execution, business model, and real yield—not just crypto holdings.