Main Points :

- Nine major U.S. banks—including JPMorgan, Bank of America, Citi, and Wells Fargo—were found to have restricted services to crypto companies and other lawful industries without risk-based justification.

- The OCC frames this as “financial weaponization”, echoing concerns long raised by the crypto industry under the label Operation Chokepoint 2.0.

- The restrictions also affected oil & gas, firearms, private prisons, and other lawful industries.

- A new federal executive order requires fair banking access for all Americans, prompting strict review and possible DOJ referrals for illegal debanking.

- The event has immediate implications for crypto liquidity, institutional adoption, compliance strategies, and the competitive landscape for exchanges and fintechs.

- Recent developments in 2024–2025 suggest increasing political and regulatory pressure to normalize and protect banking access for digital asset firms.

I. Introduction: A Turning Point in Crypto–Bank Relations

In December 2025, the U.S. Office of the Comptroller of the Currency (OCC) released preliminary findings indicating that nine of America’s largest banking institutions may have systematically denied or restricted access to lawful businesses based solely on industry classification—most notably cryptocurrency firms.

For readers exploring new crypto investment opportunities or blockchain-based business models, this development is more than regulatory news; it represents a foundational shift in how digital asset companies can obtain stable bank relationships, liquidity channels, and compliance infrastructure.

The OCC’s announcement could mark the beginning of a new era—one where access to core financial services is treated not as a political favor, but as a legal obligation.

II. Background: Operation Chokepoint 2.0 and the Battle for Access

Between 2020 and 2023, banks allegedly applied enhanced restrictions—frequently citing AML risk—to crypto companies regardless of their individual compliance posture. This echoes earlier controversies commonly referred to as Operation Chokepoint, where regulators were accused of informally pressuring banks to avoid certain industries.

The crypto industry called the newer version Operation Chokepoint 2.0, arguing that banks were being quietly discouraged from servicing VASPs (Virtual Asset Service Providers), exchanges, custodians, OTC desks, and on/off-ramp operators.

The OCC’s findings validate many of these claims for the first time.

III. The OCC’s Findings: What the Banks Actually Did

According to the preliminary report:

- Banks restricted account openings for crypto companies.

- Some banks terminated or refused correspondent relationships.

- Additional layers of review were imposed, often unrelated to measurable financial risk.

- The restrictions were applied uniformly across entire industries, violating principles of risk-based supervision.

This is important:

U.S. regulations require AML controls to be risk-based and individualized—not blanket bans.

The investigation spans major financial institutions such as:

- JPMorgan Chase

- Bank of America

- Citibank

- Wells Fargo

- And five others yet to be disclosed publicly

If enforced, corrective measures could significantly loosen banking access for crypto firms.

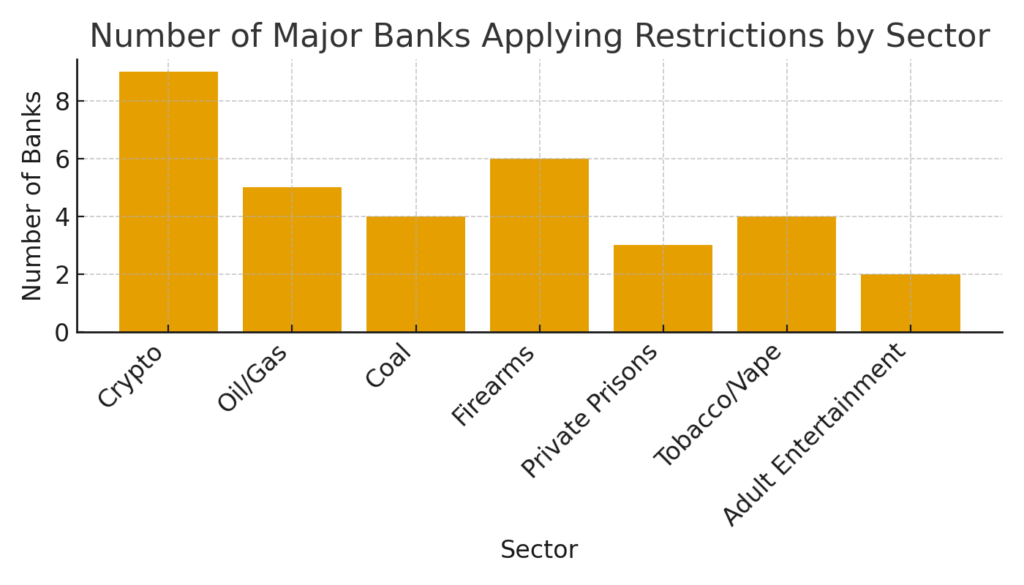

IV. Affected Industries: Crypto Was Not Alone

Beyond cryptocurrency, the OCC found that several lawful industries faced similar scrutiny:

- Oil & gas exploration

- Coal mining

- Firearms businesses

- Private prisons

- Tobacco & e-cigarette companies

- Adult entertainment

This demonstrates that the issue is broader than crypto; rather, it concerns whether banks can use ideology or political pressure to override regulatory standards.

V. Political Context: The Executive Order on Fair Banking Access

The investigation follows the August 2025 presidential executive order ensuring all Americans receive fair and equal access to financial services.

Under this order, federal agencies—including the OCC—must:

- Investigate claims of unfair debanking

- Identify politically or religiously motivated discrimination

- Recommend enforcement actions

- Refer illegal cases to the Department of Justice

This dramatically raises the stakes for banks:

Compliance failures could now trigger civil or even criminal liability.

VI. Impact on the Crypto Industry Today

1. Liquidity Redefined

For exchanges, OTC desks, and EMIs/VASPs, reliable banking access is essential for:

- fiat on-and-off ramps

- customer settlement flows

- corporate treasury operations

- compliance reporting

- segregated customer funds requirements

If banks begin reopening their doors, crypto companies could enjoy:

- Reduced fiat delays

- Lower fees

- Better FX spread efficiency

- Faster settlement cycles

2. Greater Institutional Legitimacy

2024–2025 already saw major institutions re-enter crypto:

- BlackRock and Fidelity expanded BTC/ETH ETF operations

- European banks (e.g., Santander, BBVA) launched crypto custody

- Asian regulators approved stablecoin frameworks and licensed exchanges

The OCC investigation amplifies this momentum by removing one of the last major operational bottlenecks.

3. Enhanced Compliance Expectations

Banks are still required to perform AML screening, Travel Rule compliance checks, sanctions controls, and transaction monitoring.

But the key shift is:

these controls must be risk-based—not industry-based.

This aligns with what leading VASPs already implement:

- automated KYB/KYC

- blockchain analytics (Chainalysis, TRM Labs)

- Travel Rule integration (e.g., Sumsub, Notabene)

- stablecoin reserve attestations

Firms that adopt strong controls may now find fewer obstacles when approaching banks.

VII. Global Trend: Regulators Are Normalizing Crypto Banking

Crypto-friendly regulatory movements in 2024–2025 include:

- UK: FCA’s new crypto promotion regime clarified approval routes, enabling banks to re-enter the market.

- EU: MiCA created standardized licensing for exchanges, custodians, and stablecoin issuers.

- Japan: Banks began piloting stablecoin issuance under the revised Payment Services Act.

- Singapore: MAS expanded institutional digital asset custody frameworks.

- Philippines: BSP continues to support EMIs and VASPs with strong AML frameworks and Travel Rule compliance.

The U.S. investigation now acts as a counterpart to these regulatory evolutions.

Rather than isolating crypto firms, regulators are shifting toward structured integration.

VIII. Investment Implications for Crypto Traders and Builders

1. Increased Capital Inflows Expected

If mainstream banking access stabilizes, U.S. crypto liquidity could rise significantly.

This tends to support:

- Bitcoin and Ethereum price stability

- Growth in altcoin liquidity

- Increased institutional allocations

2. On-Ramp/Off-Ramp Businesses Become More Valuable

If the banking barrier is removed, companies offering payment rails—including stablecoins—may become the infrastructure of choice.

3. VASPs and EMIs Could Expand Services

With consistent banking support, firms can:

- launch new tokens

- build remittance networks

- offer staking or yield products

- integrate cross-chain swaps

- expand to multi-jurisdiction operations

4. An Opening for New Tokens

As banking friction decreases, user onboarding becomes smoother, making it easier for new tokens or blockchain applications to gain traction.

IX. Strategic Recommendations for Crypto Businesses

- Reassess U.S. banking relationships immediately

New opportunities may emerge as banks adjust policies. - Demonstrate above-baseline compliance

Presenting strong AML/KYC/KYB data can accelerate account approvals. - Prepare documentation referencing OCC findings

Banks may now be obligated to justify any denial of service. - Leverage USD-denominated settlements

With more open banking access, USD liquidity becomes even more central. - Prepare for DOJ-linked enforcement environment

Banks may become more cautious about unfair denials—which can benefit compliant VASPs.

X. Conclusion

The OCC’s investigation into nine major U.S. banks marks one of the most consequential developments for crypto in years.

By labeling unjustified debanking as a form of financial weaponization, regulators are acknowledging what the industry has long argued: that access to financial services should not be dictated by politics or ideology, but by measurable risk.

For investors, exchanges, VASPs, and blockchain innovators, this represents a structural shift.

Stable banking access means:

- smoother fiat flows

- greater liquidity

- faster product development

- stronger institutional participation

- a more reliable compliance landscape

If the trend continues, the next phase of crypto growth could be defined not by speculative cycles, but by the maturation of infrastructure—bridging traditional finance and digital assets in a more transparent and equitable system.