Key Takeaways :

- 72% of financial leaders believe the digital asset revolution is already happening

- 74% see stablecoins as critical for cash flow efficiency and treasury operations

- Fintech firms are leading adoption, with deeper integration across operations

- Custody and infrastructure decisions are becoming the defining competitive edge

- Institutional demand is shifting from experimentation to full-scale implementation

1. From Experimentation to Execution: The Financial Industry Crosses the Threshold

The financial industry is no longer debating whether digital assets matter—it is rapidly transitioning into a phase of execution and strategic deployment. According to a recent global survey conducted by Ripple on March 19, 2026, involving over 1,000 financial leaders across banks, asset managers, fintech firms, and corporates, a decisive shift is underway.

A striking 72% of respondents acknowledged that the digital asset revolution is already in progress, highlighting a growing urgency among institutions to act—not later, but now.

This shift reflects a broader structural transformation. For years, blockchain and digital assets were treated as experimental technologies—sandboxed within innovation labs. Today, however, they are moving into core infrastructure, influencing how value is stored, transferred, and managed globally.

Financial institutions are increasingly recognizing that delaying adoption is no longer a neutral decision—it is a competitive risk.

2. Stablecoins: From Payments Tool to Treasury Backbone

One of the most significant insights from the survey is the rapid rise of stablecoins—not just as a payments mechanism, but as a foundational tool for treasury management.

A notable 74% of respondents stated that stablecoins improve cash flow efficiency and unlock working capital, signaling a major shift in how institutions perceive liquidity management.

Stablecoins are evolving beyond simple cross-border payment tools. They are now being integrated into:

- Real-time treasury operations

- Settlement optimization

- Liquidity pooling across jurisdictions

- On-demand FX conversion

For example, instead of locking capital in multiple correspondent banking accounts, companies can now centralize liquidity in stablecoins and deploy it instantly across markets, reducing idle capital and operational friction.

This transformation is particularly relevant in emerging markets, where access to efficient banking infrastructure remains uneven. Stablecoins offer a programmable, always-on financial layer that bypasses traditional bottlenecks.

3. Fintech vs Traditional Institutions: A Growing Capability Gap

The survey highlights a widening gap between fintech firms and traditional financial institutions in terms of digital asset adoption.

Fintech companies are significantly more aggressive and integrated in their approach:

- 31% use stablecoins for payment collection

- 29% accept stablecoins directly from customers

- 47% prefer building their own infrastructure rather than outsourcing

In contrast, traditional enterprises are more cautious:

- 74% plan to partner with external providers

- Focus is on reducing complexity rather than building in-house capabilities

This divergence reflects two fundamentally different strategies:

- Fintechs: Build, control, and differentiate

- Traditional firms: Partner, integrate, and mitigate risk

However, this gap may not persist indefinitely. As regulatory clarity improves and infrastructure matures, traditional institutions are expected to accelerate their adoption—potentially leapfrogging through strategic partnerships.

4. Custody, Tokenization, and Infrastructure: The New Battleground

As digital asset adoption scales, the importance of custody and infrastructure is becoming paramount.

Among institutions evaluating partners:

- 89% identified secure custody as the top priority

- 82% of banks emphasized lifecycle services

- 80% of asset managers prioritized primary issuance capabilities

This underscores a critical reality: digital assets are not just about trading—they require a full-stack infrastructure.

This includes:

- Secure custody (cold/hot wallet architecture)

- Token issuance frameworks

- Compliance and reporting systems

- Lifecycle management (issuance → trading → settlement → redemption)

In addition, advisory services are gaining importance:

- 85% of banks and 76% of asset managers value pre-issuance structuring support

This indicates that institutions are not just buying technology—they are seeking strategic guidance on how to design digital asset products correctly from the outset.

5. Platform Wars: Integrated vs Modular Infrastructure

Another key trend is the growing preference for integrated platforms.

- Over 50% of fintechs and financial institutions favor integrated solutions

- 71% of enterprises prefer unified providers to reduce vendor fragmentation

This shift is driven by operational realities. Managing multiple vendors across custody, compliance, trading, and settlement introduces:

- Integration complexity

- Security risks

- Operational inefficiencies

As a result, institutions are increasingly seeking end-to-end platforms that can handle the full digital asset lifecycle.

Vendor Selection Criteria (Top Priorities)

- Security certifications (97%)

- Post-integration support (88%)

- Industry expertise (80%)

- Financial strength (79%)

This ranking clearly shows that trust, reliability, and long-term viability are now more important than pure technological innovation.

6. XRP and Institutional Liquidity: The Expanding Role of Ripple’s Network

Beyond the survey data, broader market developments reinforce Ripple’s positioning.

Ripple’s global payments network continues to expand, strengthening the role of XRP as a bridge asset for institutional liquidity. Financial institutions are increasingly exploring blockchain-based settlement systems to reduce costs and improve speed.

Compared to traditional systems like SWIFT, blockchain networks can:

- Settle transactions in seconds instead of days

- Reduce intermediary fees

- Provide transparency and traceability

This is particularly relevant for cross-border payments, where inefficiencies remain significant.

As more institutions join these networks, network effects could accelerate adoption, further embedding digital assets into the global financial system.

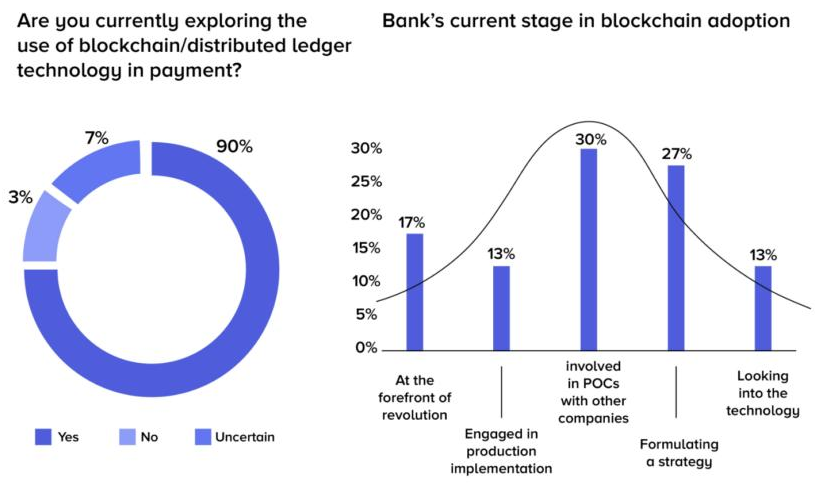

7. Insert Figure 1 Here — Digital Asset Adoption Trend (2020–2026)

Explanation:

This figure illustrates the rapid acceleration of digital asset adoption across financial institutions, highlighting the transition from experimentation to large-scale deployment.

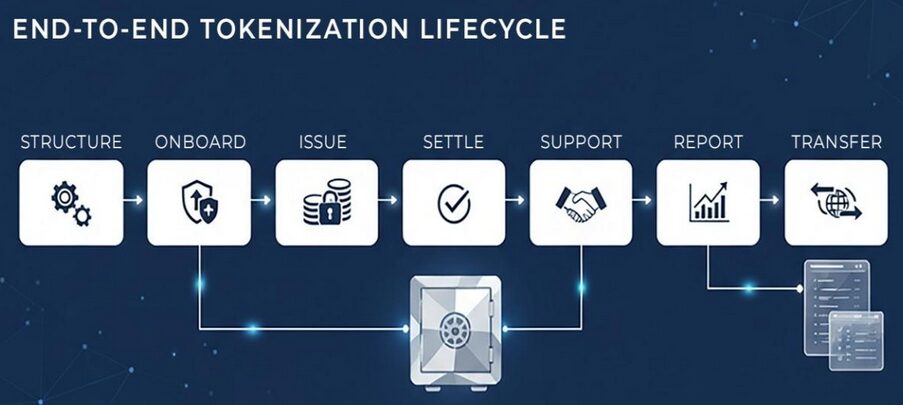

8. Insert Figure 2 Here — Digital Asset Infrastructure Stack

Explanation:

This diagram shows the full-stack architecture required for digital asset deployment, from custody and issuance to compliance and settlement.

9. Strategic Implications for Investors and Builders

For readers seeking new crypto assets, revenue streams, and practical blockchain applications, the implications are profound.

For Investors:

- Focus is shifting toward infrastructure plays (custody, compliance, tokenization platforms)

- Stablecoin ecosystems are becoming core financial rails

- Institutional adoption may drive long-term demand for utility-based assets

For Builders:

- Opportunities lie in:

- API-first financial infrastructure

- Compliance automation tools

- Cross-border payment optimization

- Tokenization platforms for real-world assets (RWA)

The key is to align with institutional needs, not just retail speculation.

10. Conclusion: Infrastructure Decisions Will Define the Next Decade

Ripple’s conclusion is clear and difficult to ignore:

“The message is clear. The infrastructure decisions made today will shape tomorrow’s competitive advantage.”

The financial industry is at a critical inflection point. Digital assets are no longer optional—they are becoming foundational.

Institutions that move decisively will not only keep up—they will define the next generation of financial services.

Those that hesitate risk being left behind in a system that is rapidly being rebuilt—on-chain.