Main Points :

- Japan’s B2B payment market exceeds $7 trillion annually, yet remains largely undigitalized.

- Tokenized deposits such as DCJPY aim to place bank deposits directly on-chain for real-time corporate settlement.

- The fusion of commercial flow and financial flow enables full automation from order to accounting entry.

- Regional SMEs face acute labor shortages, making AI-driven financial automation economically urgent.

- AI agents may soon negotiate contracts and execute payments autonomously.

- Cross-border tokenized settlement could transform international corporate payments within existing AML frameworks.

1. The Undigitalized Giant: Japan’s $7 Trillion Corporate Payment Market

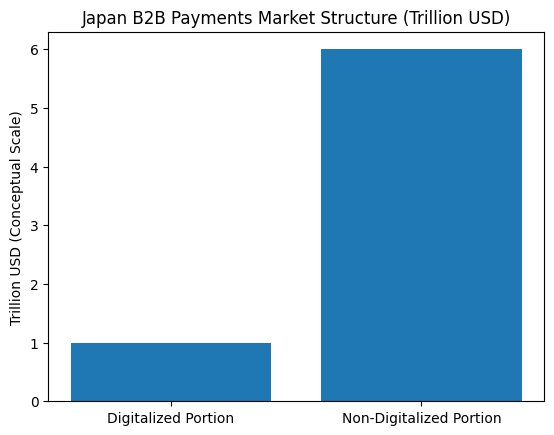

At MoneyX 2026 in Tokyo, industry leaders gathered to address a structural inefficiency hiding in plain sight: Japan’s corporate payments system. While the annual B2B transaction volume exceeds approximately $7 trillion, the overwhelming majority of these payments remain processed through traditional banking rails, manual reconciliation, paper invoices, and batch settlement systems.

This gap between transaction scale and digital modernization represents one of the largest untapped infrastructure opportunities in advanced economies.

The above conceptual visualization illustrates the imbalance between the total B2B payment market and the currently digitalized portion.

Despite Japan’s reputation for technological sophistication, internal enterprise processes — ordering, invoicing, reconciliation, and settlement — still rely heavily on fragmented systems and human intervention. This inefficiency translates into hidden costs: labor, error risk, delayed cash cycles, and capital inefficiency.

Tokenized deposits and blockchain-based settlement are emerging as potential structural solutions rather than incremental upgrades.

2. Tokenized Deposits: Placing Bank Money On-Chain

Unlike stablecoins issued by private entities, tokenized deposits represent regulated bank deposits recorded on blockchain infrastructure. DCJPY, introduced by DeCurret DCP in collaboration with GMO Aozora Net Bank, exemplifies this approach.

The critical distinction is legal and systemic: tokenized deposits remain bank liabilities. They are not shadow money; they are digitized bank money.

This architecture allows enterprises to transact directly on a shared ledger while maintaining compliance within existing AML/CFT frameworks. Because participating banks remain within the regulatory perimeter, the system can preserve KYC integrity while gaining blockchain-level programmability.

The strategic implication is profound: instead of building parallel crypto rails, financial institutions embed programmable settlement into existing banking infrastructure.

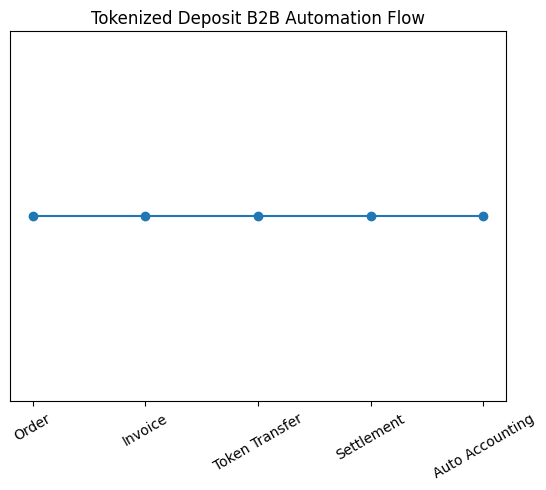

3. The Fusion of Commercial Flow and Financial Flow

Traditionally, commercial flow (orders, invoices, contracts) and financial flow (payment, settlement) operate as separate systems.

MoneyX 2026 speakers emphasized the structural inefficiency of this separation. In today’s B2B environment:

- Orders are issued manually or via ERP.

- Invoices are generated separately.

- Payment instructions are processed through banking portals.

- Accounting entries are recorded after reconciliation.

Each stage involves human oversight, introducing latency and cost.

Tokenized deposits enable a different architecture: payment becomes embedded in the commercial logic itself.

In a tokenized B2B model:

- An order triggers invoice logic.

- Invoice approval automatically releases on-chain token transfer.

- Settlement finality occurs in real time.

- Accounting entries are recorded instantly.

This eliminates reconciliation layers. Commercial intent and financial execution become synchronized.

For readers seeking practical blockchain applications, this is not speculative DeFi — it is enterprise-grade programmable finance.

4. Regional SMEs and the Labor Crisis

One of the most striking themes at MoneyX 2026 was not technological — it was demographic.

Regional small and medium enterprises (SMEs) face acute workforce aging. Administrative staff responsible for billing, payment confirmation, and ledger entries are retiring. Successors are scarce.

This labor shortage is not merely inconvenient; it is existential.

If invoicing and payment operations stall, business continuity risks escalate. For many SMEs, the digital transformation decision is no longer optional cost optimization — it is survival infrastructure.

However, regional companies often view IT investment as cost rather than strategic asset. This is where regional banks and ERP vendors play catalytic roles. By embedding tokenized deposit functionality directly into ERP systems, automation becomes invisible and frictionless.

The most compelling value proposition is not blockchain ideology — it is workforce replacement through automation.

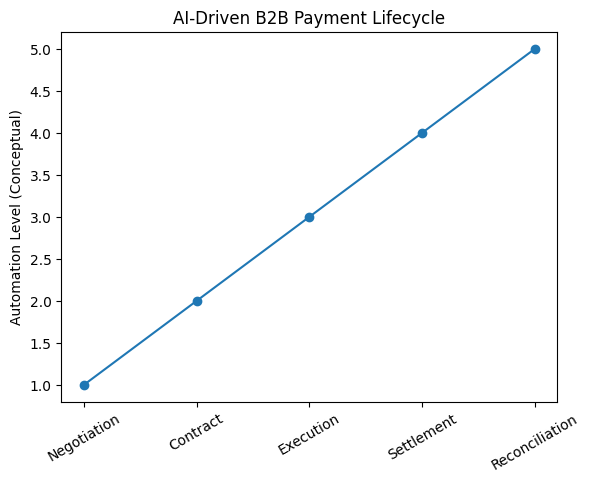

5. AI as the Next Financial Actor

The discussion expanded into the role of AI in B2B payments. The next phase is not simply programmable settlement — it is autonomous financial decision-making.

Imagine AI agents that:

- Negotiate supply contracts.

- Optimize payment timing based on cash flow forecasts.

- Prioritize receivable collection.

- Execute settlement when conditions are met.

This progression moves from automation to delegation.

Today’s AI assists humans. Tomorrow’s AI may represent corporate intent within defined parameters.

The infrastructure requirement is clear: banks must become “AI-friendly.” Payment APIs, transaction validation frameworks, and programmable token logic must accommodate non-human actors.

This shift could redefine treasury management. Instead of CFOs manually optimizing liquidity, AI agents dynamically manage working capital in real time.

For investors and blockchain builders, this intersection of AI and tokenized deposits may become one of the most scalable enterprise use cases of the decade.

6. Cross-Border Implications

Cross-border corporate settlement remains expensive and slow. Traditional correspondent banking introduces delays and FX costs.

Tokenized deposits could enable 24/7 real-time settlement between regulated institutions without abandoning AML/CFT compliance.

If banks in different jurisdictions interoperate via blockchain-based tokenized deposits, international B2B payments could bypass multiple reconciliation layers.

This would not eliminate regulation — it would streamline execution within regulation.

Given rising geopolitical fragmentation and increasing scrutiny on payment systems, programmable bank-issued digital money may provide a compliant alternative to both private stablecoins and wholesale CBDCs.

7. Strategic Implications for Crypto and Blockchain Investors

For readers exploring new digital asset opportunities, several signals emerge:

- Enterprise blockchain adoption is shifting from pilot to commercialization.

- Tokenized deposits may compete with or complement stablecoins in B2B contexts.

- AI-integrated finance could generate demand for programmable digital liquidity infrastructure.

- ERP vendors integrating blockchain natively represent overlooked equity opportunities.

This is not retail speculation. It is structural payment infrastructure.

Conclusion: From Infrastructure Upgrade to Financial Re-Architecture

MoneyX 2026 highlighted a fundamental shift: B2B payments are moving from digitization toward programmability.

Tokenized deposits do not merely accelerate settlement — they collapse the distinction between commercial agreement and financial execution.

AI agents may soon negotiate and settle transactions autonomously.

Regional labor shortages are accelerating adoption pressure.

Cross-border interoperability is becoming technically feasible.

Three years from now, tokenized deposits may become invisible infrastructure — embedded in ERP systems, triggered by AI agents, settling instantly across borders.

The fusion of commercial flow and financial flow is not a feature upgrade.

It is a re-architecture of corporate finance.