Main Points :

- The proposed CLARITY Act in the United States aims to clarify regulatory jurisdiction between financial regulators but could unintentionally strengthen centralized intermediaries.

- Critics, including leadership from Gnosis, warn that regulations assuming intermediary-based markets could undermine the core ownership model of blockchain.

- Debate over stablecoin yield restrictions, DeFi protections, and tokenized real-world assets (RWA) has stalled progress in Congress.

- Major crypto firms such as Coinbase have withdrawn support for the bill due to concerns about innovation suppression.

- The global race for crypto regulation continues, with the EU, Asia, and emerging markets exploring alternative frameworks that may shape the industry’s next phase.

Introduction: The Battle Over Crypto’s Future Infrastructure

In the rapidly evolving world of digital assets, regulation has become one of the most decisive factors shaping the industry’s long-term trajectory. Governments around the world are attempting to strike a delicate balance: protecting consumers and financial stability while preserving the innovative potential that decentralized technologies promise.

One of the most closely watched legislative efforts in this space is the proposed CLARITY Act, formally known as the Digital Asset Market Structure Transparency Act. Designed to bring regulatory certainty to the U.S. crypto market, the bill seeks to define how digital assets should be regulated and which agencies—primarily the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC)—should oversee them.

However, critics within the blockchain industry warn that the bill could fundamentally reshape the architecture of the crypto ecosystem in unintended ways. According to Dr. Friederike Ernst, co-founder of the blockchain protocol Gnosis, the regulatory structure proposed by the CLARITY Act risks pushing crypto markets back toward centralized intermediaries—precisely the system blockchain technology was designed to replace.

This debate is not merely technical or legal. It represents a deeper philosophical conflict about what cryptocurrency is supposed to be: a decentralized financial infrastructure owned by users, or simply a new technological layer integrated into the existing financial system dominated by banks and institutional actors.

For investors, developers, and businesses exploring the practical use of blockchain, the outcome of this debate could define the next decade of digital finance.

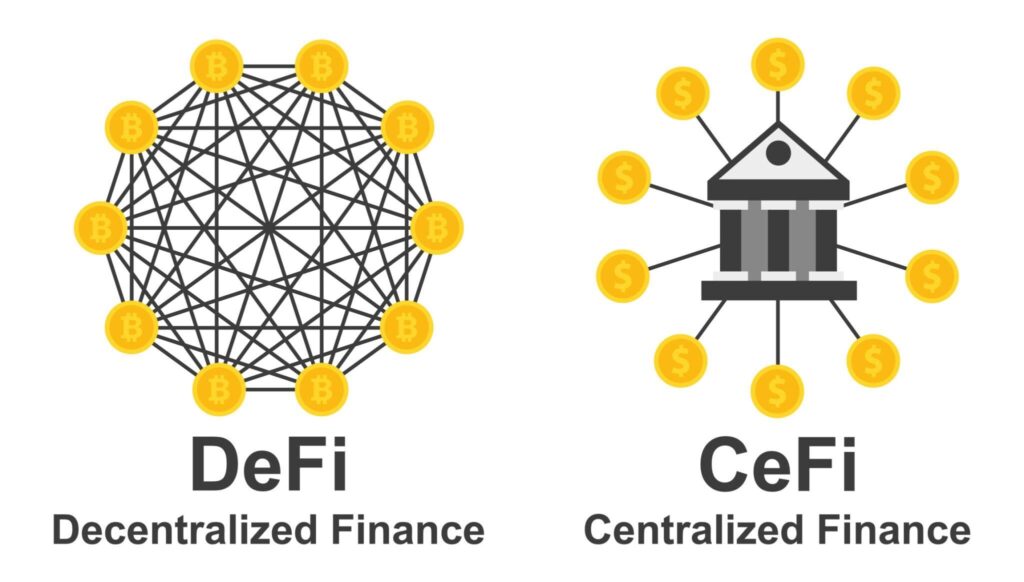

The Ownership Model of Blockchain

One of the most revolutionary aspects of blockchain technology lies in the concept of user ownership. Unlike traditional financial infrastructure—where users rely on banks, brokers, and payment processors—blockchain networks allow participants to interact directly with the system itself.

Users can hold their own private keys, validate transactions, and even participate in network governance. In many decentralized systems, token holders effectively become stakeholders in the network they use.

According to Dr. Ernst, this ownership model is what truly distinguishes blockchain from previous financial innovations.

“The real breakthrough of blockchain is not just new financial infrastructure. It is the ability for users themselves to become owners of the networks they depend on.”

If regulatory frameworks assume that transactions must pass through licensed intermediaries—such as exchanges, custodians, or broker-dealers—this model could gradually erode. Instead of being stakeholders in decentralized networks, users could once again become customers dependent on centralized institutions.

Such a shift would fundamentally alter the dynamics of the crypto economy.

In the early days of Bitcoin, peer-to-peer transactions were the norm. But over time, centralized exchanges became the dominant gateway into the market. If legislation reinforces intermediary-centric structures, critics argue that the same pattern could extend across the entire digital asset ecosystem.

How the CLARITY Act Could Centralize Crypto Infrastructure

The CLARITY Act aims to solve a long-standing regulatory conflict between U.S. agencies. For years, the SEC and CFTC have disagreed about whether certain cryptocurrencies should be classified as securities or commodities.

This uncertainty has created significant challenges for companies operating in the United States. Exchanges, developers, and investors often face unclear compliance requirements.

The CLARITY Act attempts to address this problem by:

- Defining categories of digital assets

- Clarifying regulatory oversight

- Establishing rules for digital asset markets

While these goals are broadly welcomed by the industry, critics say the bill’s market structure assumptions may inadvertently favor centralized intermediaries.

Many provisions in the proposed framework appear to assume that digital asset transactions occur through regulated entities such as exchanges, broker-dealers, and custodians.

However, this model does not fully reflect how decentralized systems operate.

In decentralized finance (DeFi) protocols, for example, users interact directly with smart contracts without relying on intermediaries. Automated market makers, liquidity pools, and on-chain governance mechanisms allow financial services to function without centralized operators.

If regulations are designed primarily around intermediary-based market structures, DeFi protocols could face compliance challenges that effectively push activity back toward centralized platforms.

This could consolidate power in the hands of large financial institutions—exactly the outcome many blockchain advocates hoped to avoid.

The DeFi and Stablecoin Controversy

One of the most contentious aspects of the CLARITY Act involves stablecoins and yield-bearing assets.

Stablecoins have become a cornerstone of the digital asset ecosystem, facilitating trading, remittances, and decentralized finance applications. The total market capitalization of stablecoins now exceeds $150 billion globally.

However, policymakers have expressed concerns about how stablecoin issuers manage reserves and distribute returns.

Some versions of the CLARITY Act include provisions that could restrict stablecoin issuers from sharing interest earned on reserves with token holders. This has sparked strong opposition from parts of the crypto industry.

Critics argue that banning yield distribution would:

- Reduce the competitiveness of stablecoins

- Limit innovation in decentralized finance

- Push users toward less regulated jurisdictions

Major crypto exchange Coinbase publicly withdrew its support for the bill after reviewing the draft legislation.

CEO Brian Armstrong stated that if the bill suppresses innovation or weakens DeFi, it may be preferable to have no legislation at all.

Real-World Asset Tokenization and Market Innovation

Another emerging area of concern involves tokenized real-world assets (RWA).

Tokenization allows physical or financial assets—such as bonds, real estate, or commodities—to be represented on blockchain networks. This innovation has the potential to dramatically improve market efficiency by enabling:

- Fractional ownership

- 24-hour global trading

- Automated settlement

Major financial institutions including BlackRock, JPMorgan, and Franklin Templeton have already launched tokenization initiatives.

However, critics argue that restrictive regulations could slow the development of RWA markets.

If compliance requirements become too burdensome for decentralized protocols, traditional financial institutions could dominate tokenization infrastructure.

This would effectively recreate the traditional financial system on blockchain rails.

Why the CLARITY Act Has Stalled in Congress

Despite strong interest from both lawmakers and industry participants, the CLARITY Act has faced significant political hurdles.

One major point of contention is the relationship between the crypto industry and the banking sector.

Banks have expressed concerns about stablecoins competing with traditional deposit products. Yield-bearing stablecoins, in particular, could attract capital away from bank accounts.

As a result, banking lobby groups have pushed for stricter restrictions on stablecoin issuers.

At the same time, crypto companies argue that excessive restrictions would undermine the economic viability of decentralized financial systems.

This conflict has contributed to legislative delays.

Some policymakers remain optimistic that the bill could pass in the near future, potentially reaching the president’s desk for approval.

However, analysts warn that if the legislation does not advance soon, its chances of passage may decline significantly.

Global Competition in Crypto Regulation

While the United States debates the CLARITY Act, other regions are moving ahead with their own regulatory frameworks.

The European Union’s MiCA regulation, for example, has already established comprehensive rules for digital asset markets.

Asia is also emerging as a major regulatory innovation hub.

Countries such as:

- Singapore

- Hong Kong

- Japan

- South Korea

are developing frameworks that aim to balance investor protection with technological innovation.

In many cases, these jurisdictions are actively competing to attract crypto businesses.

This global regulatory competition could influence how the United States ultimately shapes its own policies.

The Strategic Implications for Investors and Builders

For entrepreneurs, investors, and developers, the outcome of the CLARITY Act debate carries enormous implications.

If regulatory frameworks heavily favor centralized intermediaries, the next phase of crypto adoption may be led primarily by large financial institutions.

On the other hand, if lawmakers successfully protect decentralized infrastructure, blockchain technology could continue to evolve into a more open and user-owned financial system.

This distinction matters not only for ideological reasons but also for economic opportunities.

Entire sectors—including decentralized finance, tokenized securities, decentralized identity systems, and blockchain-based payment networks—depend on regulatory environments that allow permissionless innovation.

Conclusion: A Defining Moment for Digital Finance

The debate surrounding the CLARITY Act reflects a broader turning point for the cryptocurrency industry.

On one side lies the possibility of integrating blockchain technology into the existing financial system, where banks and institutional players remain the dominant actors.

On the other side lies the original vision of decentralized networks—where users themselves hold ownership and control over financial infrastructure.

Both paths offer potential benefits. Institutional involvement could bring stability, regulatory clarity, and large-scale adoption. Decentralization, meanwhile, promises openness, resilience, and user empowerment.

The challenge for policymakers is to design regulatory frameworks that achieve consumer protection without undermining the technological breakthroughs that made blockchain possible in the first place.

For investors and builders exploring new revenue opportunities and practical blockchain applications, understanding these regulatory dynamics will be essential.

The decisions made today may determine whether the future of finance is merely digitized—or truly decentralized.