Main Points :

- President Donald Trump criticized major U.S. banks for allegedly obstructing cryptocurrency regulatory reform.

- He urged Congress to quickly pass the Clarity Act, a bill intended to define market structure for digital assets.

- Large banks such as JPMorgan have demanded stricter regulation of stablecoin yields offered by crypto platforms.

- The regulatory delay risks pushing crypto innovation and investment to other countries, including China and Singapore.

- The debate highlights a broader struggle between traditional finance and decentralized finance over the future of global financial infrastructure.

Introduction: A Political Fight Over the Future of Crypto

In early March 2026, U.S. President Donald Trump publicly criticized the American banking sector for what he described as deliberate attempts to block cryptocurrency reform. Through a post on the social media platform Truth Social, Trump accused major financial institutions of protecting their own interests while hindering innovation in the rapidly growing digital asset sector.

At the center of the debate is a proposed piece of legislation known as the Clarity Act, which seeks to define the regulatory framework for cryptocurrencies in the United States. Trump has urged Congress to pass the bill quickly, arguing that regulatory clarity is essential if the United States hopes to remain competitive in the global blockchain economy.

The controversy reveals a deep conflict between traditional financial institutions and the emerging crypto industry. Banks worry that decentralized finance platforms and high-yield stablecoin products could undermine their core business models. Meanwhile, crypto entrepreneurs argue that outdated regulations and lobbying from the banking sector are preventing technological innovation.

For investors, developers, and entrepreneurs searching for new crypto opportunities, the outcome of this political battle could shape the next decade of digital finance.

The Core Political Issue: Why the Clarity Act Matters

The Clarity Act is designed to solve one of the biggest problems facing the cryptocurrency industry in the United States: regulatory uncertainty.

For years, crypto companies have struggled with overlapping jurisdiction between agencies such as the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC). This regulatory confusion has created legal risks for startups and discouraged institutional investment.

The Clarity Act aims to address these issues by establishing a clear framework for how digital assets should be classified and regulated. The bill would define whether tokens should be treated as securities, commodities, or a new category of digital assets.

If implemented, such a framework could significantly reduce compliance risks for crypto exchanges, DeFi platforms, and blockchain developers.

For entrepreneurs building new blockchain businesses, regulatory clarity is often more valuable than regulatory leniency. Venture capital firms and institutional investors tend to avoid markets where legal definitions are unclear.

In that sense, the Clarity Act could unlock billions of dollars in investment by providing a stable legal environment for innovation.

Trump’s Argument: Banks Are Protecting Their Profits

In his public statement, Trump accused large banks of attempting to sabotage cryptocurrency legislation in order to protect their own financial dominance.

He pointed out that many banks are reporting record profits while simultaneously holding large unrealized losses in their investment portfolios. Despite their financial strength, he argued, these institutions are lobbying against crypto legislation that could give individuals access to higher-yield financial opportunities.

Trump emphasized that Americans should have the freedom to earn higher returns on their savings through digital financial services. According to his view, crypto platforms offering yield-generating stablecoins or decentralized lending services represent a competitive alternative to traditional banking.

This argument resonates with many crypto advocates who believe that decentralized finance can democratize financial services. By removing intermediaries, blockchain networks allow users to directly participate in lending, liquidity provision, and staking.

However, from the perspective of banks, these innovations pose a threat to their business model.

The Banking Sector’s Concerns

Large financial institutions have responded to crypto industry proposals with skepticism. Banks argue that many digital asset products offer yields that appear attractive but could carry hidden systemic risks.

One of the central concerns revolves around stablecoins, which are cryptocurrencies designed to maintain a stable value relative to the U.S. dollar.

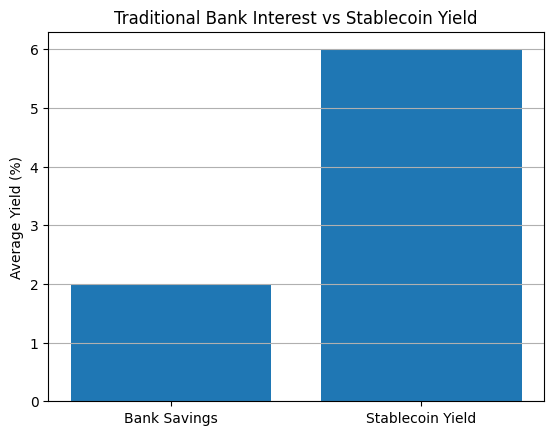

Some crypto exchanges and DeFi platforms offer yield-bearing stablecoin accounts that can generate annual returns of several percentage points. In contrast, traditional bank savings accounts often provide much lower interest rates.

Major banks such as JPMorgan have argued that these products should be regulated under the same strict framework applied to banking deposits.

Their reasoning is straightforward: if stablecoins begin functioning like bank deposits, they should be subject to similar capital requirements and risk controls.

Without such regulations, banks argue, the financial system could face instability if large stablecoin issuers collapse or experience liquidity crises.

This regulatory debate has become a key obstacle to passing the Clarity Act.

The Crypto Industry’s Response

Crypto companies, including major exchanges like Coinbase, have pushed back strongly against the banking sector’s demands.

They argue that applying bank-level regulation to blockchain platforms would stifle innovation and create barriers for startups.

Unlike banks, many crypto protocols operate through decentralized networks where governance is distributed among token holders. Traditional regulatory frameworks designed for centralized institutions may not easily apply to these systems.

Industry leaders have also emphasized that blockchain technology can increase transparency compared to traditional finance.

On-chain data allows regulators and analysts to monitor transactions in real time, potentially reducing the risk of hidden liabilities.

For many crypto entrepreneurs, the Clarity Act represents a chance to establish rules tailored specifically to digital assets rather than forcing them into outdated legal categories.

Global Competition: The Risk of Innovation Leaving the U.S.

One of Trump’s central warnings was that delays in regulatory reform could push crypto innovation overseas.

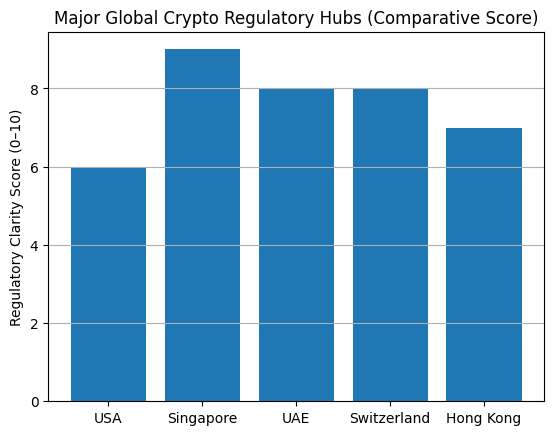

Countries such as Singapore, the United Arab Emirates, and Switzerland have already established clearer regulatory frameworks for blockchain companies.

Singapore, for example, has become a hub for crypto startups thanks to its licensing system under the Monetary Authority of Singapore (MAS). The UAE has also introduced specialized crypto regulatory zones in Dubai and Abu Dhabi.

Meanwhile, Hong Kong has reopened its digital asset market in an attempt to attract global crypto firms.

If the United States fails to implement clear legislation, blockchain companies may choose to relocate to jurisdictions that provide legal certainty.

For investors searching for the next generation of crypto opportunities, geographic shifts in innovation hubs could become increasingly important.

Stablecoins and the Next Phase of Digital Finance

The dispute over stablecoin regulation highlights a larger transformation occurring within the financial system.

Stablecoins have become one of the most widely used tools in the cryptocurrency ecosystem. They enable traders to move funds quickly between exchanges, participate in DeFi protocols, and hedge against market volatility.

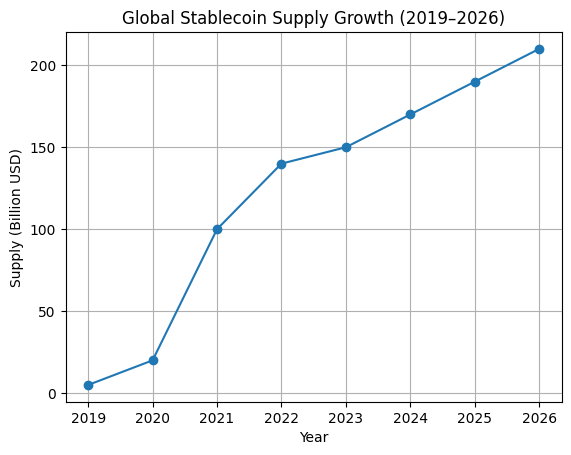

In 2025 and 2026, global stablecoin supply surpassed $200 billion, making them a major component of the digital asset economy.

For traditional banks, this growth raises concerns about deposit competition. If consumers move funds into stablecoin platforms offering higher yields, banks could lose a portion of their funding base.

However, many analysts believe that stablecoins could also complement the traditional banking system by improving cross-border payments.

For example, blockchain-based settlement systems can process transactions within minutes rather than days.

This capability has attracted interest from fintech companies and even central banks exploring digital currency initiatives.

Opportunities for Investors and Builders

For readers interested in identifying the next wave of crypto opportunities, the regulatory debate itself creates several areas worth watching.

First, companies focused on compliance infrastructure could benefit significantly from clearer rules. Tools for blockchain analytics, identity verification, and transaction monitoring will likely become essential components of the industry.

Second, stablecoin infrastructure providers may emerge as key players in the global financial system.

Third, the intersection between decentralized finance and traditional finance could produce hybrid financial platforms combining blockchain technology with regulated financial services.

Entrepreneurs who can bridge these two worlds may capture significant market opportunities.

Suggested Graph and Visual Materials

Below are suggested visuals to help readers better understand the trends discussed in this article.

Global Stablecoin Supply Growth (2019–2026)

Description:

A line chart showing the growth of global stablecoin supply from approximately $5 billion in 2019 to over $200 billion in 2026.

Global Crypto Regulatory Hubs

Description:

A world map highlighting major crypto-friendly regulatory jurisdictions including Singapore, UAE, Switzerland, Hong Kong, and the United States.

Traditional Bank Interest vs Stablecoin Yield

Description:

A comparison chart showing average bank savings interest rates (around 1–3%) versus stablecoin yields (often 4–8% depending on platform).

Conclusion: The Future of Crypto Regulation in the United States

The political confrontation between President Trump, the banking sector, and the cryptocurrency industry reflects a deeper transformation underway in global finance.

At stake is not only the fate of the Clarity Act but also the broader question of how digital assets will integrate into the financial system.

Banks fear that decentralized technologies could undermine their traditional role as financial intermediaries. Meanwhile, crypto advocates argue that blockchain networks can create a more open and efficient financial infrastructure.

If the United States succeeds in passing clear and balanced legislation, it could become the global center for blockchain innovation.

However, if regulatory uncertainty persists, the next generation of crypto entrepreneurs may build their companies elsewhere.

For investors and builders searching for the next wave of opportunities in digital finance, the outcome of this debate could shape the direction of the entire industry.