Main Points :

- The global stablecoin market has reached approximately $307 billion, up sharply from around $260 billion just months earlier.

- 39% of crypto users now receive income in stablecoins, with wages, remittances, and recurring payments leading adoption.

- Cross-border transfers via stablecoins reduce costs by around 40% compared to traditional banking channels.

- In emerging markets, adoption rates are significantly higher, with Africa showing 79% stablecoin ownership among crypto users surveyed.

- Stablecoins are evolving from trading tools into core infrastructure for payroll, savings, and global commerce.

Introduction: From Trading Tool to Global Financial Rail

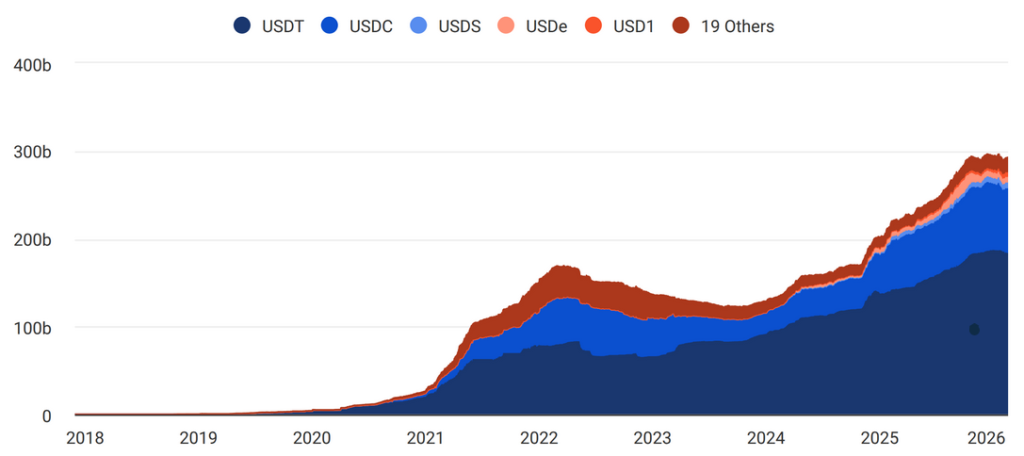

The stablecoin market has quietly crossed a historic threshold. According to data from DeFiLlama, the total market capitalization of stablecoins has climbed from approximately $260.4 billion to roughly $307.8 billion, signaling not just growth—but structural transformation.

At the same time, a new report titled Stablecoin Utility Report 2026, conducted by global research firm YouGov in partnership with international payment infrastructure provider BVNK, surveyed 4,658 crypto-aware adults across 15 countries between September and October 2025. The findings reveal something profound: stablecoins are no longer primarily investment vehicles—they are becoming income, savings, and payment infrastructure.

For readers searching for new crypto-based revenue opportunities or practical blockchain applications, this shift represents a generational turning point.

Global Stablecoin Market Growth ($260B → $307B)

1. 39% of Crypto Users Now Receive Income in Stablecoins

One of the most striking findings from the report is that 39% of surveyed crypto users receive income in stablecoins. This income includes:

- Salaries

- Freelance payments

- Cross-border compensation

- Recurring payments

Among those receiving wages in stablecoins, approximately 35% of their annual income is paid in these digital dollar equivalents.

This is no longer speculation about future adoption. This is payroll migration.

In higher-income countries, the average stablecoin balance per user is about $1,000, while globally the average sits around $200. In lower- and middle-income economies, the reliance on stablecoins is even more pronounced due to currency instability and limited banking access.

For many workers in emerging markets, receiving stablecoin payments denominated in dollar equivalents offers protection from inflation and local currency depreciation. Rather than converting earnings into volatile domestic currencies, individuals can hold digital dollars directly on-chain.

This development positions stablecoins not just as crypto assets—but as alternative banking rails.

Stablecoin Use Cases Breakdown (Salary, Savings, Daily Spending)

2. Cross-Border Efficiency: 40% Cost Reduction vs Traditional Banking

A central driver behind adoption is efficiency.

The report indicates that using stablecoins for cross-border transfers reduces transaction costs by approximately 40% compared to traditional bank-based remittance services.

This cost reduction is particularly impactful in:

- Emerging markets with high remittance inflows

- Regions where correspondent banking fees are elevated

- Countries with volatile local currencies

In many developing economies, more than 60% of respondents reported purchasing goods from vendors who accept stablecoins. Over half of all surveyed participants stated they completed purchases specifically because merchants accepted stablecoin payments.

This signals a growing merchant-side adoption curve, which is critical for sustained network effects.

Stablecoins eliminate intermediary banking layers, settlement delays, and foreign exchange friction. Instead of waiting multiple business days for wire transfers, transactions settle within minutes on blockchain networks.

For fintech operators, remittance startups, and payment processors, this cost advantage is not incremental—it is disruptive.

Regional Stablecoin Ownership Comparison

3. Emerging Markets Lead the Transformation

The geographical distribution of stablecoin ownership tells an important story:

- Lower- and middle-income countries: ~60% ownership among crypto users

- Wealthier nations: ~45%

- Africa: 79% (highest globally in survey)

In regions experiencing persistent inflation or currency depreciation, dollar-backed tokens function as accessible hedging instruments.

For many users, stablecoins represent:

- Protection against inflation

- Access to dollar exposure

- Financial inclusion without a bank account

- A store of value independent of local policy risk

This is not merely crypto adoption—it is parallel financial infrastructure emerging organically.

4. From Speculation to Utility

Historically, stablecoins were primarily used as trading pairs on crypto exchanges. Traders parked funds in digital dollars between volatile positions.

Today, the narrative is shifting:

- 27% of users report using stablecoins for everyday purchases

- 40% use them for cross-border savings

- 42% express interest in using them for large or lifestyle purchases

Current usage for major purchases stands at 28%, indicating strong room for growth.

This trajectory resembles early internet payment adoption curves. Initially niche, then cross-border, then mainstream retail.

Stablecoin Adoption Funnel – Investment → Income → Commerce

5. Infrastructure Expansion and Institutional Integration

Beyond user behavior, institutional signals reinforce this trend:

- Fintech platforms are integrating stablecoin rails for payroll.

- Payment processors are offering on/off-ramps linked to digital dollars.

- Traditional financial institutions are exploring tokenized deposits and settlement mechanisms.

Stablecoins are becoming programmable liquidity layers within broader financial systems.

For builders and entrepreneurs, this opens multiple revenue vectors:

- Stablecoin payroll infrastructure

- Cross-border B2B settlement solutions

- Merchant acceptance gateways

- Stablecoin-backed lending platforms

- Treasury management for emerging-market businesses

Strategic Implications for Investors and Operators

For readers focused on discovering new crypto assets or practical blockchain applications, consider the following strategic insights:

- Stablecoin infrastructure tokens may benefit from rising transaction volume.

- Layer-2 networks processing stablecoin settlements could capture fee flows.

- Payment-focused DeFi protocols may see structural demand growth.

- Emerging-market fintech integrations represent asymmetric opportunity zones.

The stablecoin market’s expansion from $260 billion to $307 billion is not a speculative bubble indicator—it is a usage-driven expansion signal.

Conclusion: The Quiet Monetary Revolution

Stablecoins have crossed a psychological and structural threshold.

With a market size exceeding $307 billion, nearly 40% of crypto users receiving income in digital dollars, and clear evidence of cost efficiency in cross-border transfers, stablecoins are no longer transitional tools within crypto—they are becoming foundational monetary infrastructure.

The transformation is particularly visible in emerging markets, where financial instability has accelerated adoption. What began as exchange liquidity tools are now wage rails, savings instruments, and merchant payment systems.

For investors, operators, and innovators, the key question is no longer whether stablecoins will integrate into mainstream finance—but how deeply and how quickly.

The stablecoin era has moved beyond theory. It is operational, measurable, and accelerating.