Main Points :

- S&P downgraded USDT’s peg stability rating to the lowest tier (“5 – Weak”), citing exposure to Bitcoin and other high-volatility assets.

- Tether CEO Paolo Ardoino rejected the downgrade, emphasizing billions in surplus reserves and nearly $30B in group equity.

- Tether’s total assets ($215B) exceed total liabilities ($184.5B), strengthening its claim of over-collateralization.

- The company now ranks among the world’s largest holders of U.S. Treasuries—above South Korea—at $135B.

- Tether also holds approximately 116 tons of gold, making it the largest non-central-bank holder globally.

- Analysts disagree about whether Bitcoin exposure introduces systemic risk if risk assets fall sharply.

- The broader context: the stablecoin market is shifting rapidly as institutional adoption grows, U.S. regulation nears, and yield-bearing stablecoins emerge.

1. Introduction: A New Phase in Stablecoin Scrutiny

In December 2025, the stablecoin market entered a new spotlight after S&P Global Ratings downgraded the peg stability evaluation of Tether’s USDT, the world’s largest dollar-backed stablecoin. As institutions increasingly integrate blockchain-based settlement and investors search for new crypto assets with real-world utility, scrutiny over backing, risk exposure, and liquidity mechanisms is intensifying.

The downgrade triggered immediate global discussion. But the response from Tether CEO Paolo Ardoino was unusually strong—accusing S&P of misunderstanding the company’s balance sheet, ignoring billions in surplus reserves, and failing to account for the company’s extraordinary profitability.

This article breaks down the dispute, adds current market context, and analyzes what this means for investors, builders, and institutions exploring stablecoins as infrastructure for the next wave of blockchain adoption.

2. S&P’s Assessment: Why USDT Was Downgraded

S&P downgraded USDT to the lowest score in its evaluation framework, arguing:

- Tether holds Bitcoin as part of its reserves.

- Bitcoin represents 5.6% of the circulating USDT market cap.

- A sharp drop in BTC—combined with declines in other risk assets—could in theory reduce the value of USDT reserves below its liabilities.

S&P’s logic follows a simple stress-test philosophy:

Stablecoin collateral should withstand severe market conditions. If certain assets cannot reliably weather extreme downturns, peg risk rises.

S&P has historically placed higher trust in cash and short-dated U.S. Treasuries, which remain the global standard for risk-free collateral. Bitcoin, by comparison, is volatile even in mature markets.

But critics argue that S&P evaluated only the reserve composition, not the entire corporate balance sheet, which is where Tether says S&P went wrong.

3. Tether’s Rebuttal: “You Ignored Our Surplus Capital”

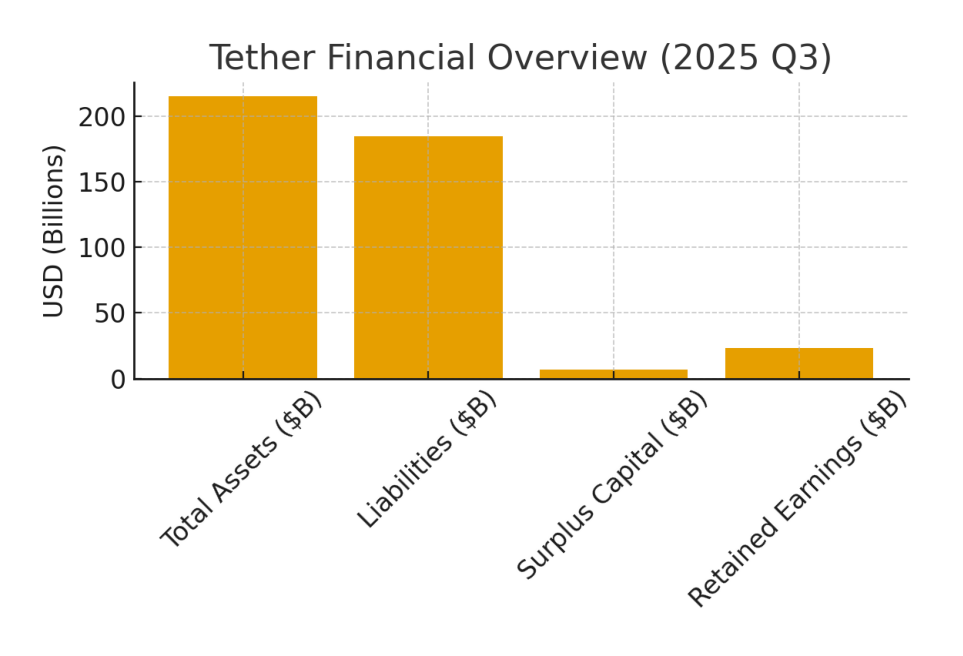

Ardoino responded by highlighting financial data from Tether’s Q3 2025 reserve attestation, stating:

- Total stablecoin reserves: $184.5B

- Surplus reserves: $7B

- Retained earnings within the Tether Group: $23B

- Total corporate assets: $215B

- Liabilities related to issued USDT: $184.5B

In simple terms:

Tether claims its assets exceed liabilities by nearly $30B.

This surplus is significant for three reasons:

(1) It absorbs volatility from non-core assets.

If Bitcoin loses value, the surplus is theoretically designed to cushion losses.

(2) It reflects high profitability.

Tether earns roughly $500M per month—almost entirely from U.S. Treasury yields.

(3) It strengthens long-term solvency.

Few financial institutions, even banks, maintain this scale of retained earnings relative to liabilities.

Tether argues that stablecoin ratings should reflect the company’s ability to absorb reserve volatility, not focus solely on asset composition.

4. Chart: Tether Financial Overview

(Shows Assets vs. Liabilities vs. Surplus vs. Retained Earnings)

5. Analysts Debate: Is Bitcoin Exposure Good Risk Management or a Hidden Weakness?

The crypto analyst Arthur Hayes has repeatedly suggested that Tether increases exposure to Bitcoin and gold as a hedge against future declines in U.S. Treasury yields. According to Hayes:

- If U.S. rates drop, Tether’s profit margin falls.

- Bitcoin and gold could provide alternative yield or capital appreciation.

- However, these assets introduce volatility that could jeopardize the peg in downturn scenarios.

On the other side, industry researcher Joseph argues:

- Not all of Tether’s assets appear in the reserve attestation.

- Corporate assets, equity, and retained earnings sit in a separate balance sheet.

- Tether’s equity is “massively valuable” and could be sold to cover losses if necessary.

Ardoino publicly endorsed this view, reinforcing Tether’s position that it is not a fragile, single-layer collateral pool but a global financial enterprise with multilayered capital structures.

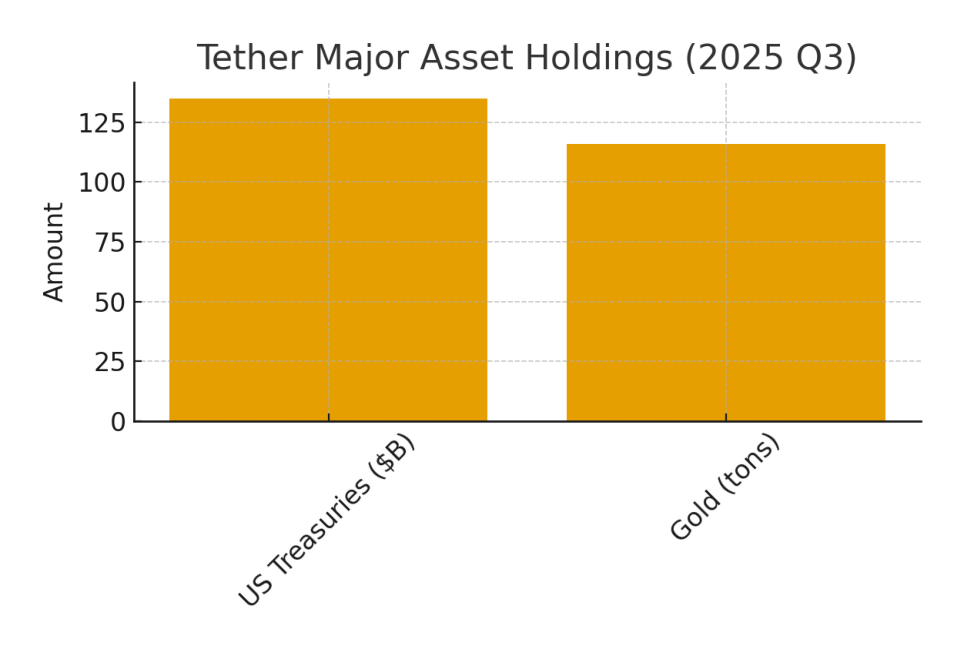

6. Tether as a Global Financial Power: Treasuries and Gold at National Scale

One of the most striking data points is Tether’s rise as a major holder of U.S. Treasuries:

- $135B in treasuries as of September 2025

- Larger than South Korea’s national holdings

- Ranked #17 in the world among sovereign and institutional holders

For perspective, this places Tether above many G20 nations.

Gold holdings further emphasize Tether’s scale:

- Approx. 116 tons of gold

- Largest non-central-bank holder

- Backing its gold-pegged token XAUt

- Over $300M invested in precious-metal production companies this year

These metrics demonstrate that Tether has evolved from a crypto startup into a quasi-sovereign financial institution—one that materially influences U.S. Treasury demand and global liquidity.

7. Chart: Tether’s Major Asset Holdings (Treasuries vs. Gold)

8. The Broader Context: Regulation, Institutional Adoption, and Yield-Bearing Stablecoins

The debate between S&P and Tether reflects a much larger transformation in the stablecoin industry:

(1) U.S. stablecoin legislation is nearing completion.

Multiple committees in the U.S. government have been drafting regulatory frameworks for fully backed stablecoins—potentially requiring:

- 1:1 cash or Treasury backing

- Daily reporting

- Capital requirements similar to money-market funds

Tether, being offshore, may face new competitive pressure if U.S.-regulated stablecoins like USDC or PayPal USD become more attractive for institutional clients.

(2) Institutional adoption of blockchain settlement is accelerating.

Banks, payment processors, FX desks, and global remittance companies increasingly integrate stablecoins for instant settlement.

USDT remains dominant in emerging markets (Asia, LATAM, Africa), where users prefer high-liquidity tokens.

(3) A new category: yield-bearing or “rebasing” stablecoins.

Projects such as Mountain USD, UXD, and Ondo’s U.S.-regulated products are exploring ways to pass Treasury yield back to users—something Tether does not do.

This shift may disrupt USDT long-term unless Tether adapts by offering yield products or diversifying revenue further.

9. Implications for Crypto Investors and Builders

For investors seeking new revenue opportunities or blockchain applications, the S&P–Tether dispute highlights several trends:

(A) Stablecoins are becoming infrastructure, not just trading tools.

Payment rails, remittances, institutional FX, and on-chain treasury management now rely heavily on USDT and USDC.

(B) Risk models will become more sophisticated.

Expect more rating frameworks assessing:

- Reserve composition

- Liquidity under stress

- Corporate equity buffers

- Exposure to risk assets

- Chain concentration

- Market depth

(C) Decentralized money and sovereign-scale issuers are colliding.

Tether’s gold and treasury holdings show how crypto companies are evolving into geopolitical financial entities.

(D) New assets and new opportunities will emerge.

As regulation increases and institutional demand rises, expect:

- More asset-backed tokens (real estate, commodities, FX baskets)

- New stablecoin competitors with transparent yield models

- Blockchain-native liquidity systems replacing traditional market-making

For builders and investors who target practical blockchain use cases, this shift marks one of the most important structural changes since DeFi’s rise in 2020.

10. Conclusion: What the Downgrade Really Means

S&P’s downgrade does not threaten USDT’s dominance in the short term. Its liquidity remains unmatched, and Tether’s capital structure appears stronger than many expected.

However, the controversy underscores a new reality:

Stablecoins are now global financial institutions—and they will be judged like banks.

The next few years will bring:

- Regulatory pressure

- Competition from U.S.-regulated stablecoins

- Demand for transparency

- Increased expectations for risk management

For investors searching for new assets and builders creating next-generation crypto applications, understanding the stability and structure of dominant stablecoins is essential.

USDT remains powerful—but the era of minimal scrutiny is over.