Key Takeaways :

- Tesla, Inc. continues to hold ~11,509 BTC (~US $1.3 billion) at the end of Q3 2025.

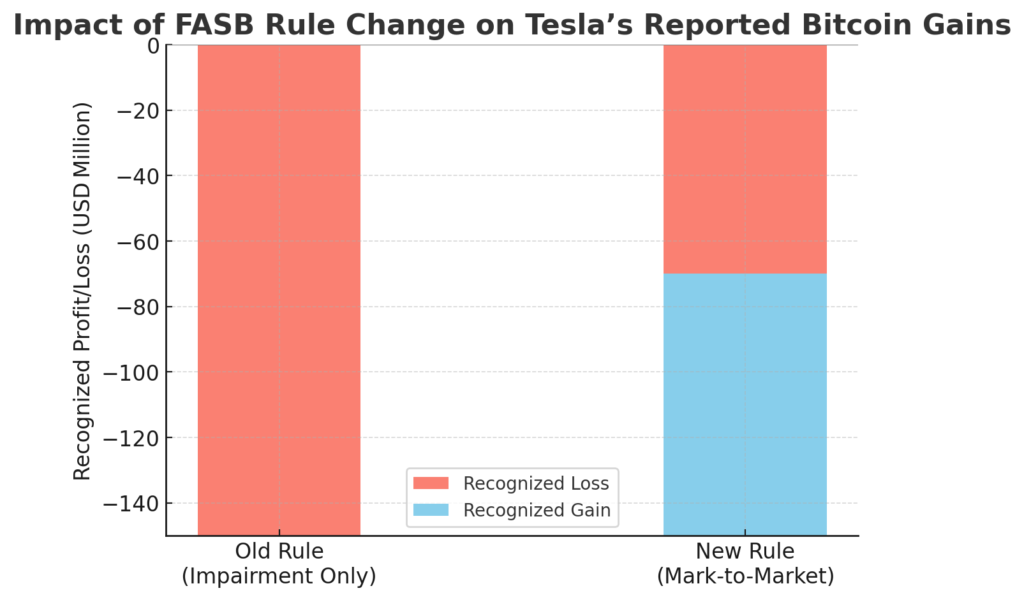

- Thanks to the Financial Accounting Standards Board (FASB) new rule (ASU 2023-08), Tesla recognized ~US $80 million in unrealized gains on its Bitcoin holdings in Q3 2025.

- The accounting shift from “impairment only on drop” to “mark-to-market real-time gains and losses” increases both risk and transparency for firms holding crypto.

- Tesla’s adoption of Bitcoin as a treasury asset provides a model of how corporate balance sheets may integrate digital assets—relevant for crypto investors seeking the next wave.

- While Tesla’s automotive business missed EPS expectations in Q3, its crypto strategy provides a differentiator and signals broader institutional acceptance of crypto-treasury use.

1. Tesla’s Bitcoin Position: Strategic and Steady

Tesla’s decision to hold roughly 11,509 BTC (valued at about US $1.3 billion at the end of Q3 2025) demonstrates its steady commitment to the asset. Unlike some earlier years when the company sold portions of its holdings, the current stance is “no sale this quarter,” signalling long-term treasury orientation rather than opportunistic trading. This gives the crypto community and potential investors in blockchain-enabled projects important context: a major corporate entity sees strategic benefit in long-term digital asset exposure.

For practitioners and crypto-asset hunters, the implication is two-fold: one, major firms can hold crypto without needing to liquidate for gains, and two, the presence of a large corporate holder adds a stabilising layer to the broader market ecosystem.

2. The Accounting Game-Changer: FASB’s ASU 2023-08

One of the biggest macro developments for crypto adoption in the corporate world has been the accounting reform by FASB. Historically, crypto assets on corporate books were treated under “indefinite-lived intangible assets” rules, meaning you could only recognise a loss when the value dropped (impairment), but you could not recognise a gain unless you sold the asset. Under ASU 2023-08 (effective for many companies beginning 2025), firms can mark to market crypto assets each quarter and recognise both unrealised gains and losses in net income.

For Tesla, this meant their BTC holdings generated ~US $80 million in recognised gain in Q3 2025, even without a sale. The accounting change thus unlocks latent value in corporate crypto holdings and elevates crypto from peripheral footnote to a strategic treasury item.

3. Why This Matters to Crypto Investors

For anyone hunting new crypto opportunities or seeking productive yield, Tesla’s example offers a blueprint. Here’s why:

- Legitimacy boost: A large, high-profile company publicly disclosing crypto gains adds to institutional legitimacy of digital assets.

- Treasury use-case: Beyond speculative trading, crypto becomes part of corporate financial strategy (hedge, reserve, asset class) which may lead to more stable, long-term flows into the space.

- Volatility & accounting channel: The mark-to-market rule means crypto price moves can directly impact a company’s earnings—hence price swings in assets like BTC matter not just for traders but for investor perceptions of corporate health.

- Secondary signal for alt projects: If companies treat Bitcoin as treasury, similar logic might eventually be applied to other tokenised assets or blockchain-based reserves—meaning projects with real business adoption may gain traction.

In short: the move elevates crypto from niche to integrated, suggesting that the next wave of value may come from projects tied to real-world asset integration, treasury management, or corporate finance utility, not just “meme-coin” hype.

4. Market Context & Broader Trends in 2025

Beyond Tesla, a few other signals reinforce the trend:

- The total corporate Bitcoin treasury holdings grew significantly in 2025, supporting the notion of deeper institutional integration.

- Firms are increasingly comfortable holding crypto without liquidating, as market participants recognise internal transfers ≠ sales, dampening panic-selling responses to on-chain movements.

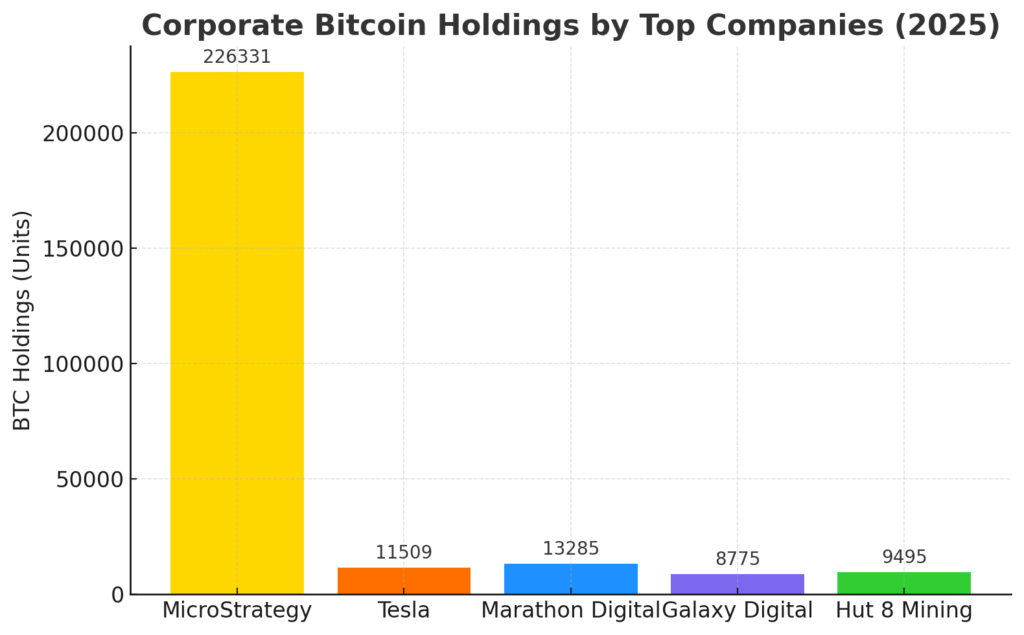

- The accounting reforms have implications beyond recognising gains: for example, firms like MicroStrategy Incorporated may face large tax burdens from unrealised gains recognized under the Corporate Alternative Minimum Tax (CAMT) in the U.S.

- The trend suggests we’re moving toward a new paradigm where digital assets may be treated like other corporate treasury assets (e.g., foreign exchange reserves, commodities, strategic hedges)—a major shift for blockchain builders and investors alike.

For anyone exploring blockchain projects, this shift means thinking not just about token price but how tokenised assets might plug into corporate finance, treasury, or balance-sheet applications.

5. The Risks & Cautions

While Tesla’s case is encouraging, there are important caveats:

- Price volatility: Even with mark-to-market accounting, crypto values fluctuate wildly. A sudden down-move could hurt earnings more dramatically than under the old rules. The flip side of recognition of gains is recognition of losses.

- Regulatory/tax risk: As seen with MicroStrategy’s tax exposure, recognising unrealised gains could trigger tax events or regulatory burdens which many companies may not yet fully internalise.

- Core business distraction: For Tesla, the primary business remains electric vehicles, energy solutions, and autonomy. Crypto plays are secondary—investors should keep the core business health in view. In Q3, Tesla’s automotive EPS missed expectations despite the crypto gain.

- Adoption timing: Tesla’s strategy may not transfer neatly to smaller companies or projects without deep balance sheets. The infrastructure, disclosure regime, and capital scale matter.

For blockchain project investors, the takeaway is: while the tailwinds are strong, token utility must tie into real value-creation, not just balance sheet exposure. A theoretically great token without real application or corporate adoption may still underperform.

6. Practical Implications for Blockchain Project Hunters

Given the above, how should someone interested in new crypto assets or blockchain use-cases think? Consider the following:

- Prioritise projects that aim at corporate treasury/asset-reserve use-cases: For example, tokenised commodities, real-world asset tokenisation, or projects designed to serve enterprise balance sheets may be advantaged.

- Look for transparency & reporting: The shift towards mark-to-market accounting means institutional investors will favour projects with clear disclosures, auditability, and predictable financial relationships.

- Mind integration with existing infrastructure: A project that plugs into treasury management software, corporate finance flows, or tokenised asset platforms may stand out.

- Be aware of macro/regulatory impact: Changes in rules (like FASB’s) can create opportunities. One rule change opened the door for Tesla’s gains—your next investment might hinge on a different regulatory lever.

- Balance risk & utility: Just because a token has corporate treasury appeal doesn’t guarantee price appreciation. The core business must make sense, the token utility must be real, and market timing still matters.

7. Conclusion: A Shift in the Crypto Landscape

Tesla’s Bitcoin treasury strategy and the accompanying accounting reform mark a meaningful inflection point for crypto-asset adoption in the corporate world. What was once fringe speculation is now increasingly woven into balance sheets, investor narratives, and corporate disclosures. For blockchain enthusiasts, developers, and investors hunting the next wave, the message is clear: focus on utility, transparency, and integration rather than pure hype.

The shift from “crypto as speculative trade” to “crypto as strategic treasury tool” may usher in a wave of tokens and projects designed for enterprise integration, corporate finance, and real-world asset representation. If you’re exploring new assets or business models, this is exactly the context you need to understand.

In short: Tesla’s US $1.3 billion holding and US $80 million mark-to-market gain aren’t just numbers—they signal a maturation of corporate crypto use-cases, and your next investment strategy should reflect that.