Key Points :

- Six major Swiss banks, including UBS, have launched a sandbox for a CHF-denominated stablecoin

- The initiative aims to build a fully regulated digital money infrastructure by 2026

- The project is supported by Swiss Stablecoin AG

- Focus areas include payment efficiency, programmability, and integration with traditional finance

- Switzerland’s strict AML/KYC framework presents both a challenge and a global benchmark

- The move reflects a broader trend: institutional adoption of stablecoins and tokenized finance

Introduction: From Experimentation to Financial Infrastructure

In a decisive step toward the future of regulated digital finance, six of Switzerland’s leading financial institutions—including UBS, PostFinance, and Sygnum—have jointly launched a sandbox experiment for a Swiss franc (CHF)-denominated stablecoin.

This initiative is not merely a technological test. It represents a strategic shift toward building a compliant, scalable, and institution-grade digital money ecosystem. Unlike speculative crypto projects, this effort is rooted in regulatory alignment, interoperability, and real-world financial utility.

At its core, the sandbox aims to answer a critical question:

Can stablecoins evolve from crypto-native tools into the backbone of modern financial infrastructure?

The Structure of the CHF Stablecoin Sandbox

The sandbox is a controlled experimental environment designed to simulate real-world financial conditions while maintaining strict oversight. Participants include six major banks:

- UBS

- PostFinance

- Sygnum

- Raiffeisen Switzerland

- Zürcher Kantonalbank

- Banque Cantonale Vaudoise

These institutions are collaborating with Swiss Stablecoin AG, which provides the issuance and technical backbone.

Key Design Principles

- 1:1 CHF Peg: Each token is backed by Swiss francs, ensuring stability (~$1.10 equivalent depending on FX)

- Permissioned Environment: Only approved participants can transact

- Transaction Limits: Controlled volumes to minimize systemic risk

- Open Expansion: Additional banks and enterprises may join

This approach balances innovation with risk control, allowing institutions to experiment without exposing the broader financial system.

Why Switzerland—and Why Now?

Switzerland has long been a global leader in crypto regulation. However, its strict compliance framework—particularly around anti-money laundering (AML) and identity verification—has paradoxically slowed the adoption of stablecoins.

The Core Problem

Despite its advanced financial system, Switzerland lacks a widely adopted, regulated CHF stablecoin. This creates inefficiencies in:

- Domestic digital payments

- Cross-border settlements

- Tokenized asset transactions

The Strategic Timing

Several macro trends are converging:

- Institutional Crypto Adoption

Major banks are increasingly entering digital asset markets, not as speculators but as infrastructure providers. - Stablecoin Market Expansion

According to Chainalysis, stablecoin transaction volumes could reach $1.5 quadrillion by 2035. - Rise of Tokenized Assets (RWA)

Tokenized bonds, equities, and funds require stable settlement layers—precisely what regulated stablecoins provide.

Stablecoin Market Growth Projection (USD)

Use Cases: Beyond Payments

The CHF stablecoin is not just about faster payments—it is about programmable finance.

1. Programmable Payments

Smart contracts enable:

- Automated payroll

- Conditional escrow

- Subscription-based financial flows

2. Institutional Settlement

Banks can settle transactions:

- Instantly (vs. T+2 or T+3)

- With reduced counterparty risk

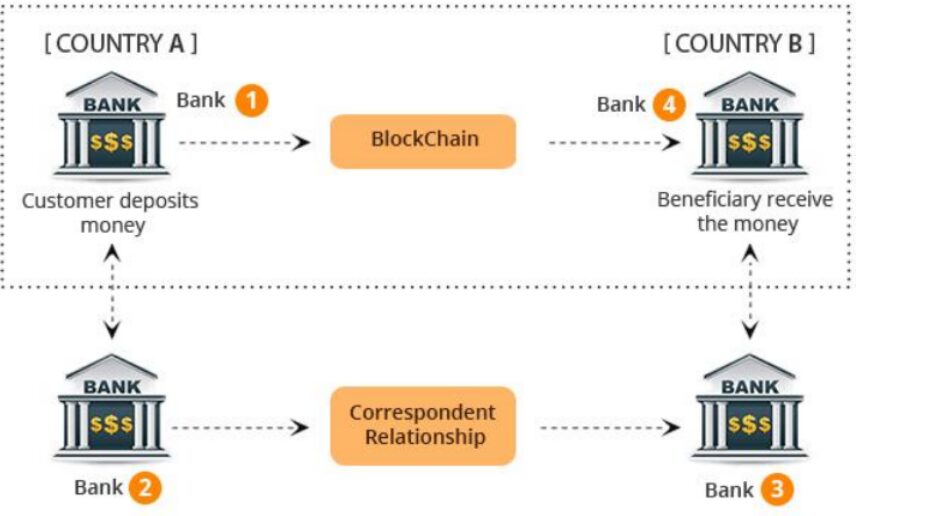

3. Cross-Border Efficiency

A CHF stablecoin could act as a bridge currency, reducing reliance on correspondent banking networks.

4. Tokenized Securities (RWA)

Stablecoins serve as the settlement layer for:

- Tokenized bonds

- Real estate shares

- Structured financial products

Traditional vs Blockchain Settlement Flow

Regulatory Challenge: Compliance vs Scalability

Switzerland’s regulatory strength is also its biggest constraint.

Key Barriers

- Mandatory identity verification for all holders

- Strict AML requirements

- Limited anonymity compared to crypto-native systems

These factors have historically limited adoption. However, the sandbox aims to turn compliance into a competitive advantage.

New Approach

- Embed compliance directly into the infrastructure

- Use blockchain transparency for auditability

- Align with global standards (FATF, EU frameworks)

This could position Switzerland as the global standard-setter for regulated stablecoins.

Competitive Landscape: A Global Race

Switzerland is not alone in this race.

United States

- USD stablecoins (USDC, USDT) dominate global markets

- Regulatory clarity is still evolving

European Union

- MiCA regulation is driving euro stablecoin development

Asia

- Japan and Singapore are piloting regulated stablecoins

- Strong focus on compliance and interoperability

Switzerland’s advantage lies in its bank-led approach, integrating stablecoins directly into the traditional financial system.

Strategic Implications for Investors and Builders

For readers seeking new crypto opportunities and revenue streams, this development signals several key trends:

1. Institutional Stablecoins Will Dominate

Retail-focused stablecoins may give way to:

- Bank-issued digital currencies

- Regulated settlement tokens

2. Infrastructure > Speculation

Value will shift toward:

- Payment rails

- Compliance layers

- Tokenization platforms

3. New Revenue Models

Opportunities include:

- Stablecoin issuance services

- Liquidity provisioning

- Cross-border payment optimization

Conclusion: The Beginning of Regulated Digital Money

The CHF stablecoin sandbox marks a pivotal moment in financial history. It represents the convergence of:

- Traditional banking trust

- Blockchain innovation

- Regulatory compliance

Rather than disrupting the financial system, this initiative seeks to upgrade it from within.

If successful, Switzerland could establish a blueprint for how stablecoins integrate into global finance—not as fringe assets, but as core infrastructure.

For investors, developers, and institutions alike, the message is clear:

The future of money is not just digital—it is programmable, regulated, and deeply integrated into the financial system.