Main Points:

- The New York State Department of Financial Services (NYDFS) has issued new guidance urging banks—both domestic and foreign branches operating in NY—to adopt blockchain analytics tools to better manage risks related to cryptocurrencies.

- These tools are expected to be used in wallet screening, verifying the source of crypto-linked funds, monitoring counterparty risk, and assessing risk before deploying new crypto products.

- The guidance emphasizes that risk-management frameworks must be tailored to each bank’s business model, risk appetite, and operations, and they should be reviewed and updated regularly.

- NYDFS frames this policy shift as a response to the growing exposure of traditional banks to crypto asset activities, and the fact that many licensed crypto companies are already using such analytics.

- The guidance is part of broader compliance and regulatory tightening: in parallel, NYDFS is enhancing cybersecurity requirements (e.g. MFA controls) for banks.

Background: Rising Regulatory Pressure in the Crypto Space

In recent years, the proliferation of digital assets has brought both opportunity and risk. Financial regulators globally have expressed increasing concern over the potential misuse of cryptocurrencies for illicit activities—money laundering, sanctions evasion, terrorist financing—and over operational vulnerabilities. New York has long stood at the forefront of U.S. crypto regulation, with licensing regimes (such as BitLicense) and guidance aimed specifically at virtual currency service providers. As banks more deeply engage with crypto—whether via customer exposure, custody, or third-party relationships—the NYDFS sees a growing need for banks to adopt tools and practices already common among crypto firms.

Guidance Details: What NYDFS Expects Banks to Do

Wallet Screening and Counterparty Due Diligence

Banks are now explicitly expected to screen wallets or blockchain addresses to detect linkages with sanctioned individuals or entities, or other signs of illicit activity. Similarly, counterparties—especially virtual asset service providers—must be subject to enhanced risk assessment, including background scrutiny and behavior monitoring.

Source of Funds and Transaction Behavior Monitoring

It’s not enough simply to monitor transactions; banks must validate the origins of funds tied to digital asset activity and compare expected customer behavior with actual one. Significant deviations should raise red flags and lead to further investigation.

Risk Assessments for New Products or Services

Whenever a bank contemplates offering new services involving digital assets—tokenization, custody, facilitating crypto trades, or partnering with exchanges—it should perform a risk evaluation specific to crypto assets. This includes exposure to regulatory, operational, reputational, and compliance risk. Blockchain analytics should be part of these evaluations.

Tailoring and Maintenance of Risk Frameworks

Not all banks are the same. Size, customer base, level of crypto involvement, geography, and business model differ. NYDFS requires that each bank’s risk-management framework reflect these differences. Moreover, the guidance expects periodic review and updating of compliance measures, tools, and policies as technology and market risk evolve.

Related Trends: Where This Policy Fits In

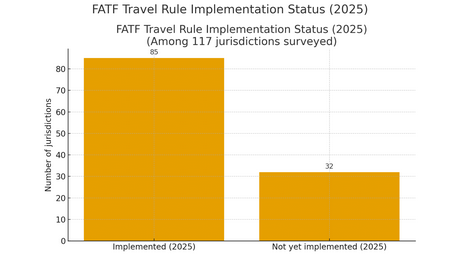

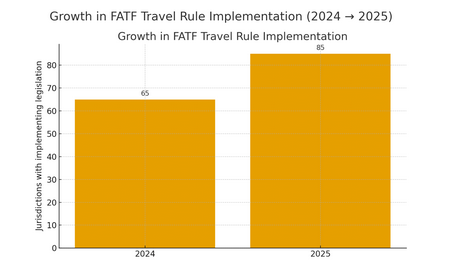

- FATF and Global Oversight: The Financial Action Task Force has highlighted that many jurisdictions are still behind in implementing effective regulation around crypto assets. In 2024 alone, illicit crypto wallet addresses received an estimated US$51 billion. Stablecoins are increasingly used in illicit finance.

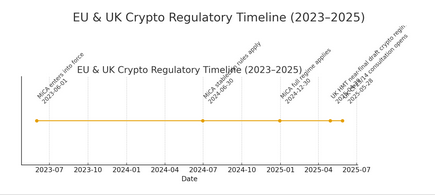

- Regulatory Movement in the UK/EU: In the UK, regulators are balancing consumer protection with the need for innovation; stablecoins, fund tokenization, and operational risk controls are under deep scrutiny. In the EU, the MiCAR framework continues to shape how crypto asset service providers are regulated, though cross-border enforcement and harmonization remain contentious.

- Institutional Use of Blockchain Infrastructure: Institutions are deploying blockchain in ways beyond speculative tokens—platforms for issuance, trading, settlement; tokenization of real-world assets; more efficient back-office operations. These changes increase the exposure of traditional finance to crypto-specific risks.

- Stablecoin Regulation Growing Stronger: Laws like the U.S. GENIUS Act signal that stablecoins are being treated more as part of the payments and financial infrastructure, not just speculative or fringe assets. Requirements for reserve backing, transparency, audits, and regulatory permissions are increasing.

What This Means for Innovators and Investors

If you’re looking for new crypto assets, use cases, or heading projects in blockchain, here are implications to keep in mind:

- Think compliance first: Building products with regulatory expectations in mind will avoid later roadblocks.

- Analytics tools as infrastructure: Vendors and platforms that provide blockchain analytics (on-chain tracking, risk scoring, wallet classification etc.) will be in higher demand.

- Transparency in tokenomics, partner selection, governance, and auditing will help gain trust from banks, regulators, and institutional investors.

- Jurisdiction matters: Regulatory regimes are diverging. Where you base your operations, whom you partner with, and where you market — all will affect risk profile.

- Innovation in regulatory tech: Opportunities exist in tools for automated risk assessment, monitoring, real-time compliance dashboards, proofs of reserve, or privacy-respecting analytics.

Conclusion

NYDFS’s latest guidance represents more than an incremental change—it is part of a broader shift where oversight of crypto and digital assets is becoming more formalized, rigorous, and technology-enabled. For banks, compliance is no longer optional; blockchain analytics are moving from “nice to have” to essential. For innovators, the message is that regulatory readiness must be baked into product design. And for investors, those projects with strong transparency, risk controls, and alignment with emerging compliance standards are likely to be positioned more safely and sustainably in the evolving landscape.