Main points:

- World Mobile has partnered with Indonesia’s Protelindo to launch World Mobile Stratospheric, a blockchain-enabled 5G network delivered from hydrogen-powered aircraft flying at ~60,000 ft, each using 450 steerable beams to cover up to 15,000 km² and support hundreds of thousands of direct-to-handset connections.

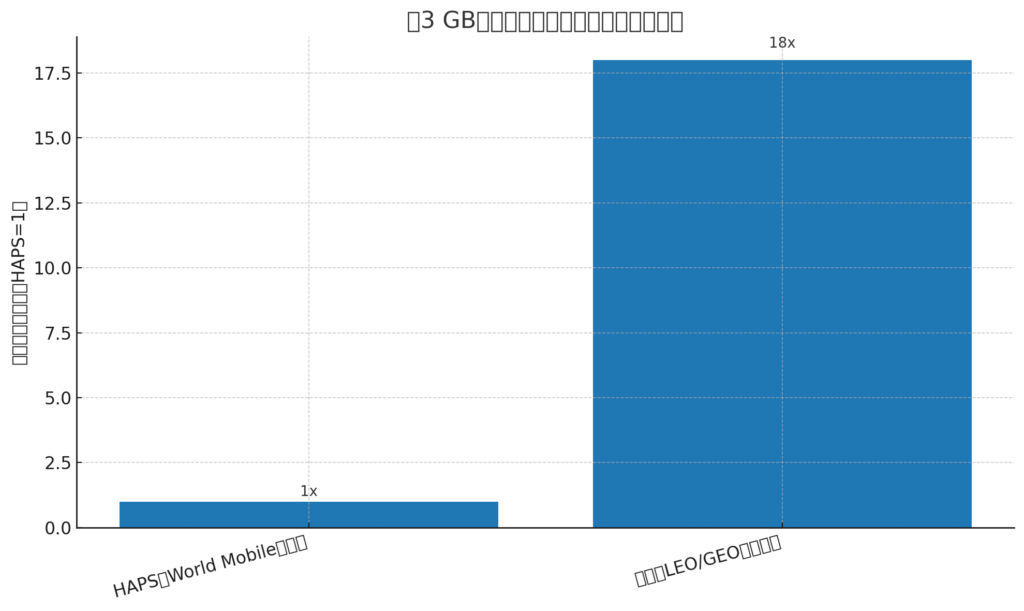

- The company claims ~6 ms total latency and up to 18× lower cost per GB than satellite, positioning stratospheric platforms (HAPS) as a middle ground between towers and LEO satellites.

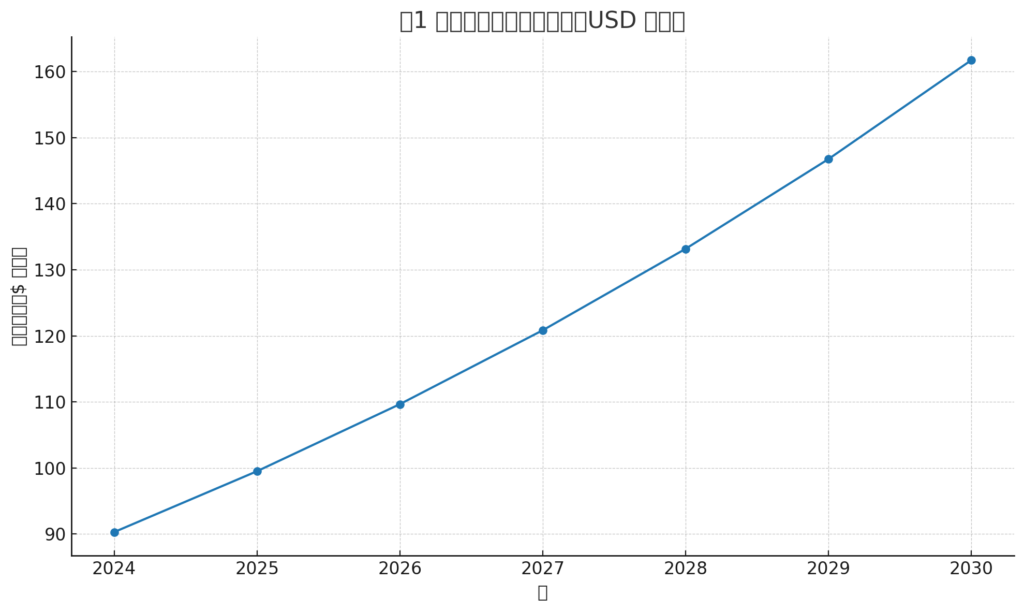

- The broader satellite-communications market is projected to reach $159.6B by 2030—a target addressable pool that HAPS and DePIN-style wireless projects can tap. [Insert Figure 1 here.]

- Competitively, Starlink Direct-to-Cell began texting services in 2024 and is rolling out data in 2025; U.S. regulators approved higher-power D2C in 2025. Helium signed a 2025 Wi-Fi offload deal with AT&T, underscoring momentum for decentralized/alt-infrastructure models.

- Regulation is catching up: the FAA just released a BVLOS drone operations proposal (Aug 2025), while EASA/JARUS documents outline certification guidance for HAPS—key enablers for commercial scale.

- For investors and builders, watch for aircraft certification milestones, spectrum & 3GPP alignment (NTN Releases 17/18), carrier partnerships, and usable economics (CAPEX/OPEX per covered user).

1) What’s new: drones, 5G, and a DePIN business model

World Mobile announced World Mobile Stratospheric, a stratospheric telecom platform built with Protelindo, Indonesia’s largest digital infrastructure provider. The platform uses hydrogen-powered, fixed-wing unmanned aircraft to beam cellular service directly to standard mobile handsets, with 450 guidable beams per aircraft and claimed coverage of ~15,000 km² per vehicle at ~60,000 ft. The company frames this as blockchain-enabled telecom—mesh economics and community operation on the ground, with tokenized incentives and settlement via its WMTX token.

According to World Mobile’s chief business officer, the stratospheric link can deliver ~6 ms total latency and a cost per GB up to 18× cheaper than satellites. If delivered in production, those numbers would be transformative for dense, underserved regions where terrestrial towers are sparse and satellite remains costly or device-constrained.

Beyond the aircraft, World Mobile has long pursued a DePIN (Decentralized Physical Infrastructure Network) strategy on the ground—community-deployed connectivity nodes, revenue sharing, and blockchain-based accounting. The stratospheric layer is an ambitious extension intended to fill coverage gaps economically where towers are impractical.

2) Why the stratosphere? A sweet spot between towers and satellites

Today’s options for wide-area connectivity trade off cost, latency, and density:

- Towers deliver great latency and capacity, but site acquisition, power, and fiber backhaul make rural expansion expensive.

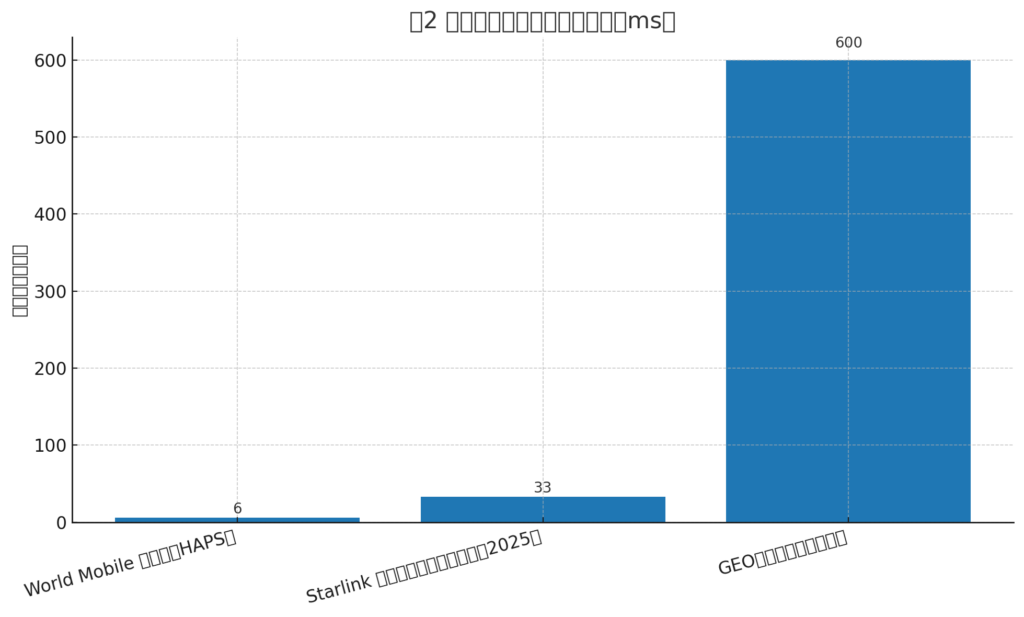

- LEO satellites (e.g., Starlink) push signals from space, expanding reach, with median U.S. latency now around ~33 ms and falling; however, high fleet CAPEX, spectrum constraints, device limitations, and beam geometry shape performance and economics. [Insert Figure 2 here.]

- GEO satellites offer broad coverage at the cost of physics—~600 ms round-trip latency typical for GEO internet, unsuitable for real-time apps.

HAPS (High-Altitude Platform Systems) aim to split the difference: aircraft above weather at ~18–20 km (≈60–65k ft), close enough to keep latency very low and beams tightly shaped for dense user clusters, while avoiding many tower-by-tower costs. World Mobile’s pitch is exactly that: tower-like latency, LEO-like reach, and lower cost per served user in dense but underserved markets.

Figure 2 (insert here): Indicative End-to-End Latency Comparison (ms).

3) The competitive backdrop: Starlink D2C and Helium’s carrier deals

Competition is intense across non-terrestrial and decentralized wireless:

- Starlink Direct-to-Cell (D2C). SpaceX’s Starlink is layering cell-tower-in-space capability into its LEO constellation. Texting began in 2024, data/IoT starts in 2025, and voice is “coming soon.” New Zealand’s One NZ has offered nationwide satellite texting since December 2024, while in the U.S., the FCC granted higher-power D2C authorizations in March 2025 for SpaceX/T-Mobile, despite objections from terrestrial carriers.

- Helium & carrier offload. In April 2025, AT&T struck a commercial arrangement with the Helium Network (a DePIN Wi-Fi network) to let subscribers roam onto community hotspots—an on-ramp for decentralized wireless into mainstream carrier operations. This follows earlier Helium partnerships (e.g., Movistar in Mexico). The carrier offload narrative—where community nodes carry traffic and earn rewards—has moved from concept to commercial pilots.

World Mobile’s stratospheric approach therefore enters a market where space-based D2C is scaling and DePIN offload is gaining validation with Tier-1 carriers. Its differentiation is direct-to-handset from the stratosphere plus a blockchain-based, sharing-economy ground model—potentially compelling in archipelagic or mountainous geographies where tower economics break.

4) Standards and regulation: the runway is clearing

Two things must be true for HAPS to scale commercially: the radio stack must interoperate with existing phones/networks, and the aircraft must be certifiable and operable at scale.

- 3GPP NTN (Releases 17/18). 3GPP Release 17—frozen in 2022—added Non-Terrestrial Networks (NTN) support for 5G NR and IoT (NB-IoT/eMTC), a necessary step for smartphone-class links from non-terrestrial platforms. Release 18 expands mobility and continuity. A HAPS platform aligning with these specs can integrate more easily with MNO cores and standard devices.

- FAA BVLOS rulemaking (U.S.). In August 2025, the FAA published a notice of proposed rulemaking to normalize Beyond Visual Line of Sight (BVLOS) operations and outline performance-based regs for aircraft, operations, UTM services, and reporting. While HAPS operate far above typical low-altitude UAS, a maturing BVLOS regime lowers operational friction across ferry, maintenance, and test operations in U.S. airspace.

- EASA/JARUS HAPS guidance (EU/Global). The JARUS CS-HAPS airworthiness recommendations (2024) and HAPS Alliance certification pathway papers give manufacturers and operators a concrete framework to approach type certification and acceptable risk levels—vital for national approvals.

5) The market: $159.6B satcom tailwind, DePIN momentum

The global satellite communications market is forecast to grow from ~$90.3B (2024) to ~$159.6B (2030), a 10.2% CAGR—a powerful secular tailwind for alternative architectures like HAPS that can plug into the same value chains (backhaul, enterprise private networks, mobility). Figure 1 visualizes this trajectory. [Insert Figure 1 here.]

Figure 1 (insert here): Global Satellite Communication Market Projection (USD Billions).

In parallel, DePIN is transitioning from thesis to deployment. Helium’s latest metrics show rising real traffic and Tier-1 partnerships; Messari’s Q2 2025 report cites 2,721 TB offloaded in the U.S. since inception and accelerating activity as carriers test decentralized offload at scale. Broader DePIN tracking shows dozens of active networks across compute, storage, and connectivity, with 2025 viewed as a pivotal year for mainstream integrations.

6) Engineering realities: what must work at 60,000 ft

Operating in the stratosphere presents unique aerospace and RF challenges:

- Radiation & thermal management. Electronic payloads must be hardened against space radiation effects and engineered to dissipate heat on the sun-facing side while enduring cryogenic temps on the dark side—nontrivial at 20 km altitude.

- Endurance & propulsion. World Mobile’s hydrogen aircraft must demonstrate multi-day endurance, reliable climb/loiter/landing profiles, and lightweight energy systems with rigorous safety cases.

- Certification and ops. Regulators will demand type certification, operational approvals, and robust detect-and-avoid/UTM integration—areas where JARUS/EASA documents and the FAA BVLOS proposal are directly relevant.

These are solvable, but they drive timelines and capital. Investors should thus track prototype hours, envelope expansion, and regulatory engagements as leading indicators.

7) Economics: what “18× cheaper per GB” could mean

World Mobile asserts up to 18× lower cost per GB versus satellite. Without the company’s full cost stack, we can’t verify the exact math; however, the claim reflects real levers: shorter link budgets, smaller payload mass than satellites, targeted beams for denser ARPU, and reusable vehicles. If the all-in cost per GB lands close to claims, a HAPS cell could profitably serve mid-density geographies that are uneconomic for towers and too costly for LEO/GEO.

Figure 3 (insert here): Relative Cost per GB (Claimed). It indexes HAPS = 1× vs Satellite = 18× for illustration.

8) Where this fits first: Indonesia and other archipelagic markets

Indonesia is an archetypal initial market: thousands of islands, significant rural population, and varied topography that make tower densification expensive. Protelindo brings on-the-ground infrastructure expertise and commercial routes into MNOs and enterprise. If World Mobile can demonstrate carrier-grade service (KPIs like latency, throughput per sector, handover, call-drop rates), MNOs could adopt HAPS as on-demand capacity or rural overlay, similar to how carriers see satellite D2C as a roaming-like extension.

Other near-term use cases:

- Disaster recovery: rapid comms restoration without trucking generators and towers.

- Maritime & offshore: fishing fleets, oil & gas platforms—where LEO is present but stratospheric beams could target lanes/fields.

- Mining/logistics: campus-scale private networks over vast concessions.

- Events/surge capacity: seasonal or event-driven demand spikes.

9) Competitive scorecard (2025 snapshot)

- World Mobile Stratospheric (HAPS). Differentiator: direct-to-handset HAPS, DePIN ground economics, low latency claims; challenges: aircraft certification, flight ops, scaling to fleets.

- Starlink Direct-to-Cell (LEO). Differentiator: global constellation, proven LEO economics, D2C approval momentum; constraints: spectrum coordination, device support ramp, urban blockage.

- Helium Mobile / Wi-Fi DePIN. Differentiator: AT&T offload, immediate device compatibility (Wi-Fi), low deployment cost; constraints: QoS variability, indoor bias, incentive sustainability.

Expect hybrid deployments: terrestrial + HAPS + LEO D2C + DePIN Wi-Fi offload. The winning stacks will optimize latency, coverage, and $/GB per geography and use case.

10) What to watch (KPIs & milestones)

- Aircraft & certification: flight hours at altitude, endurance achieved, certification pathway clarity (JARUS/EASA), and BVLOS operational approvals where relevant.

- 3GPP alignment: field demos with Tier-1 MNOs using NTN-aligned radios, mobility/handovers, and standard SIM/RAN integration.

- Carrier commitments: MoUs moving to commercial capacity buys (per-GB or per-covered-pop models), SLAs, and initial revenue.

- Unit economics: CAPEX per aircraft, lifecycle OPEX (energy, maintenance), ground gateway costs, and revenue per active user.

- Token utility (WMTX): actual settlement/utilization metrics (e.g., data paid, staking tied to uptime), rather than speculative flows.

11) Bottom line

World Mobile’s stratospheric pivot feels timely. Regulators are framing BVLOS rules, 3GPP NTN is in place, Starlink D2C is catalyzing handset-from-space expectations, and DePIN is proving it can carry real traffic with Tier-1s. If World Mobile can convert its 6 ms latency / 18× cost claims into carrier-grade deployments, HAPS could become an essential layer in the world’s connectivity stack—especially across the Global South and hard-to-serve regions.

For builders and investors seeking new crypto-native revenue streams, this is a credible real-world DePIN thesis: token-incentivized ground infrastructure + innovative airborne RAN delivering services users already pay for, in a $159.6B and growing market. Execution, not concept, is now the critical variable.