Main Points :

- Strategy (formerly MicroStrategy) raised its March 2026 STRC preferred dividend from 11.25% to 11.50%.

- STRC is a perpetual preferred stock with monthly adjustable yield targeting price stability around $100 par.

- The company is shifting capital strategy from common equity issuance to preferred equity issuance.

- Strategy accumulated approximately $7 billion via preferred shares, representing 33% of the total preferred market.

- Bitcoin has declined approximately 23.2% year-to-date.

- Strategy reported a $12.4 billion net loss in Q4 2025.

- Strategy holds 717,722 BTC, acquired at an average cost of $76,020 per BTC.

- The structural shift may redefine corporate crypto treasury financing models.

A New Capital Engineering Phase in Bitcoin Treasury Strategy

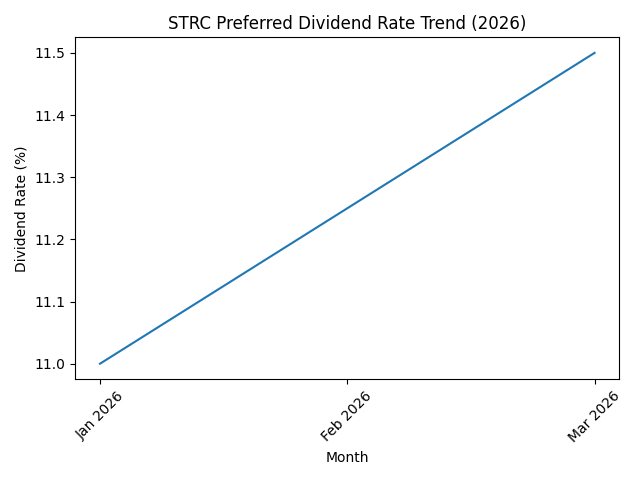

Strategy, the world’s largest corporate holder of Bitcoin, announced through Executive Chairman Michael Saylor that it will raise the dividend rate of its STRC preferred shares to 11.50% for March 2026, up from 11.25%.

STRC, known internally as “Stretch,” is structured as a perpetual preferred equity instrument. Unlike traditional bonds, it does not carry a mandatory redemption date. Instead, its dividend rate adjusts monthly to maintain trading stability near its $100 par value.

This design is critical. Rather than exposing investors to excessive volatility in price, the dividend mechanism acts as a stabilizer. When the share price deviates from par, the yield adjusts to incentivize equilibrium.

[STRC Dividend Rate Trend (2026)]

The dividend increase to 11.50% signals two things:

- Management’s confidence in sustaining high yield obligations.

- Market demand pressure requiring incremental yield to maintain par stability.

Monthly dividend payments further enhance its appeal to income-oriented investors, especially during volatile crypto cycles.

From Common Equity Dilution to Preferred Capital Architecture

CEO Phong Le stated in February earnings commentary that Strategy is transitioning away from reliance on common stock issuance to fund Bitcoin purchases. Instead, it is scaling preferred equity issuance.

Last year alone, Strategy and its perpetual preferred structures raised approximately $7 billion — accounting for 33% of the entire preferred stock market issuance volume.

This is extraordinary.

Rather than diluting common shareholders during volatile Bitcoin cycles, Strategy is effectively securitizing yield expectations into preferred instruments. The capital stack is becoming layered:

- Common equity absorbs volatility.

- Preferred equity monetizes yield demand.

- Bitcoin remains the reserve asset.

This structural innovation may represent a blueprint for future Bitcoin treasury corporations.

Market Context: Bitcoin Drawdown and Corporate Exposure

Despite continued Bitcoin accumulation, the broader market backdrop has deteriorated.

Bitcoin has declined approximately 23.2% year-to-date. Simultaneously, equity vehicles providing exposure to corporate Bitcoin holdings have fallen sharply.

The Bitwise Bitcoin Standard Corporations ETF (OWNB) declined approximately 16.1% during the same period.

Strategy itself reported a staggering $12.4 billion net loss in Q4 2025. Although quarterly revenue increased 1.9% year-over-year to approximately $123 million, the market focused on unrealized Bitcoin losses.

The stock reacted violently.

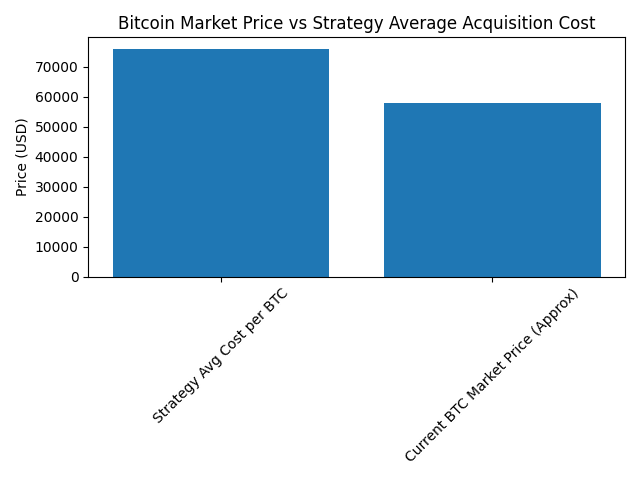

[Bitcoin Market Price vs Strategy Average Cost]

Strategy’s average acquisition cost per Bitcoin stands at $76,020. Current market prices trade significantly below that level.

This creates:

- Mark-to-market accounting losses.

- Equity valuation compression.

- Heightened volatility.

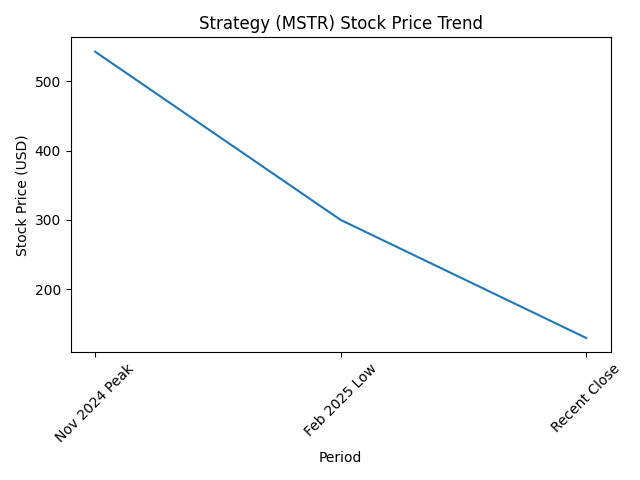

Equity Collapse: From $543 to Below $130

Strategy’s stock peaked at $543 intraday in November 2024. By February 2025, it fell below $300. Recent closing price: approximately $129.50.

That represents roughly a 75% drawdown from peak levels.

[Strategy (MSTR) Stock Price Trend]

Such volatility reflects leveraged exposure to Bitcoin price cycles combined with accounting treatment under GAAP rules.

Yet notably, despite losses and equity decline, Strategy continues to accumulate Bitcoin.

In the week ending February 16, it purchased 592 BTC for approximately $39.8 million. Total holdings now stand at 717,722 BTC, marking its 100th Bitcoin acquisition.

Why Raise the Dividend During a Downturn?

The dividend increase is counterintuitive at first glance. Why increase payout obligations while reporting multi-billion-dollar losses?

The answer lies in capital engineering:

- Preferred investors demand yield compensation for volatility risk.

- Maintaining price stability around $100 par prevents loss of confidence.

- High yield sustains capital inflows without diluting common equity.

In essence, Strategy is converting Bitcoin volatility into structured yield products.

This mirrors structured finance techniques historically used in mortgage-backed securities and hybrid capital instruments.

Implications for Crypto Treasury Companies

Strategy’s shift from common equity to preferred equity suggests an emerging model:

- Bitcoin as treasury reserve.

- Preferred shares as yield instruments.

- Common shares as leveraged upside exposure.

This tri-layered capital stack could inspire:

- Corporate Bitcoin treasury adoption.

- Tokenized preferred equity models.

- On-chain yield securitization.

In fact, future iterations may involve blockchain-native issuance of preferred shares or tokenized dividend-bearing instruments.

Broader Industry Trends

Recent trends across the digital asset ecosystem reinforce this structural evolution:

- Spot Bitcoin ETFs have normalized institutional exposure.

- Corporations increasingly explore Bitcoin treasury allocation.

- Stablecoin yield products and on-chain credit markets are expanding.

- Tokenized real-world assets (RWAs) are gaining traction.

Strategy’s move aligns with financial engineering convergence between TradFi and crypto-native capital markets.

For investors seeking new revenue sources, this hybridization of Bitcoin exposure and yield structure may represent the next frontier.

Risk Considerations

However, risks remain substantial:

- Continued Bitcoin price decline could stress dividend sustainability.

- Regulatory changes could alter accounting frameworks.

- Preferred share overhang could pressure capital structure.

Moreover, if Bitcoin falls significantly below average acquisition cost for extended periods, market confidence may weaken.

Strategic Outlook

Despite short-term drawdowns, Strategy’s continued accumulation suggests long-term conviction.

By increasing the STRC dividend to 11.50%, management signals commitment to:

- Maintaining investor confidence.

- Stabilizing preferred share pricing.

- Expanding alternative capital channels.

If Bitcoin enters a new macro expansion cycle, the current capital structure may amplify upside dramatically.

If downturn persists, the preferred structure must withstand stress tests.

Either way, Strategy is not merely accumulating Bitcoin — it is experimenting with financial architecture.

Conclusion

Strategy’s decision to raise its March 2026 STRC dividend to 11.50% marks more than a yield adjustment. It represents a structural transformation in corporate crypto finance.

Amid Bitcoin’s 23.2% year-to-date decline and a $12.4 billion quarterly loss, the company is pivoting away from common equity dilution toward preferred capital engineering.

With 717,722 BTC on its balance sheet and a $76,020 average acquisition cost, Strategy remains the most aggressive institutional Bitcoin accumulator in history.

For readers seeking new crypto assets, yield opportunities, and practical blockchain financial applications, the key takeaway is clear:

The next phase of crypto evolution may not be about price alone — it may be about structure.

Capital stack design, yield securitization, and hybrid TradFi-crypto instruments could define the coming decade.

Strategy is building that model in real time.