Main Points :

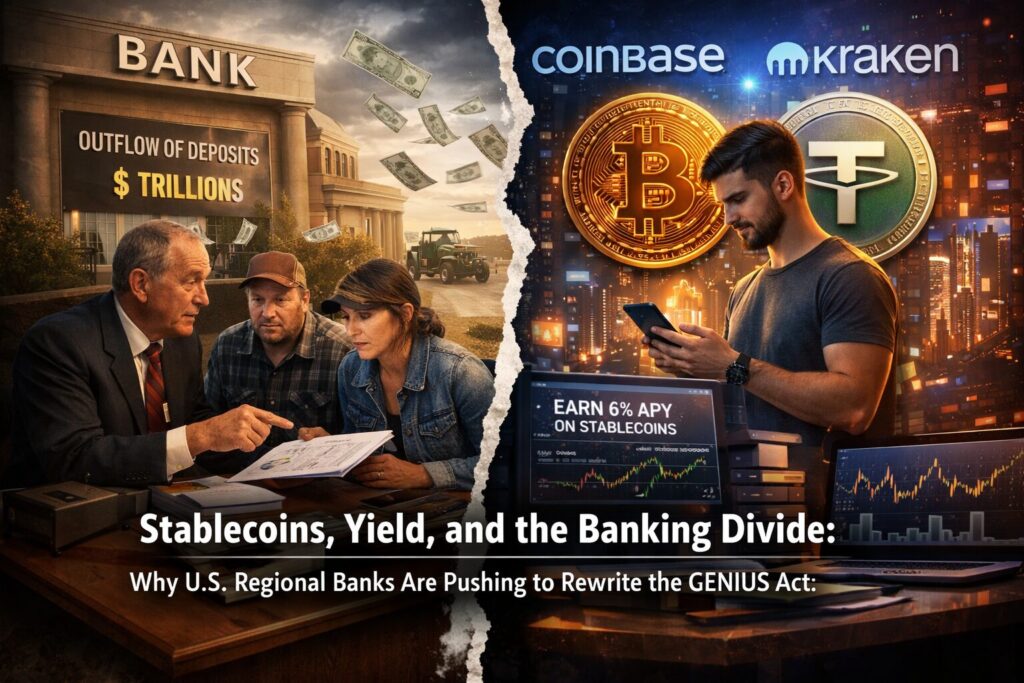

- U.S. regional banks are urging lawmakers to tighten the GENIUS Act, arguing that crypto exchanges are exploiting regulatory loopholes to provide yield on stablecoins.

- While stablecoin issuers are legally barred from paying interest directly, exchanges like Coinbase and Kraken offer indirect rewards, intensifying tensions with the banking sector.

- Banking groups warn that large-scale deposit outflows—potentially reaching trillions of dollars—could undermine lending to local businesses, farmers, and households.

- Crypto industry advocates counter that there is no evidence of disproportionate deposit flight and argue that banning yield would stifle innovation and competition.

- For investors and builders, the debate signals a crucial inflection point in stablecoin regulation, with implications for yield strategies, DeFi integration, and real-world payments.

1. The GENIUS Act and Its Original Intent

The GENIUS Act, a U.S. legislative proposal aimed at establishing a comprehensive regulatory framework for stablecoins, was designed to strike a careful balance between innovation and financial stability. One of its most important provisions prohibits stablecoin issuers from paying interest or yield directly to token holders.

This clause was inserted largely at the request of the traditional banking sector. Lawmakers were concerned that interest-bearing stablecoins could function as de facto bank deposits without being subject to the same prudential regulation, deposit insurance, or supervisory oversight. In short, Congress sought to prevent stablecoins from becoming unregulated substitutes for savings accounts.

From the banks’ perspective, this was a critical safeguard. Deposits are the foundation of bank lending, especially for regional and community banks, which rely heavily on stable deposit bases to fund loans to small and medium-sized enterprises (SMEs), agricultural operations, students, and homebuyers.

2. The “Loophole” Problem: Exchanges and Indirect Yield

Despite the GENIUS Act’s restrictions on issuers, regional banks argue that the spirit of the law is being undermined. In early January 2026, the American Bankers Association (ABA) Community Bankers Council sent a formal letter to the U.S. Senate demanding amendments to close what it calls a regulatory loophole.

According to the council, while stablecoin issuers themselves are not paying interest, crypto exchanges are stepping in as intermediaries. Platforms such as Coinbase and Kraken offer rewards, incentives, or yield-like benefits to users who hold certain stablecoins on their platforms.

From the banks’ standpoint, this distinction is purely technical. Whether yield is paid directly by an issuer or indirectly via an exchange partner, the economic effect is the same: stablecoins become yield-bearing instruments that compete head-to-head with bank deposits.

“The exception is swallowing the rule,” the council warned, arguing that billions of dollars could be siphoned away from community banks into crypto platforms.

3. Why Regional Banks Are Particularly Concerned

Unlike large global banks, regional and community banks play a specialized role in the U.S. financial system. Their business models are deeply intertwined with local economies:

- SME Lending: Small manufacturers, retailers, and service providers often depend on local banks for credit.

- Agriculture: Farmers rely on seasonal and equipment loans structured around local conditions.

- Housing and Education: Mortgages and student loans in rural and suburban areas are frequently financed by regional institutions.

The ABA argues that if stablecoins—especially those offering yield—absorb a significant share of deposits, these lending activities could suffer. Banks stress that crypto exchanges and “stablecoin-related corporate groups” are not designed to replace this function. They do not engage in relationship-based lending, nor do they offer government-backed protections such as deposit insurance.

4. Escalating Pressure: Trillions at Stake

This latest letter is not an isolated action. Since mid-2025, banking industry lobbying around the GENIUS Act has intensified.

In August, the Bank Policy Institute, led by JPMorgan Chase CEO Jamie Dimon, cited a U.S. Treasury report warning that as much as $6.6 trillion in bank deposits could theoretically migrate to stablecoins under certain adoption scenarios.

By December, the ABA and banking associations from all 52 U.S. states issued a joint statement accusing exchanges of offering rewards through “high-risk strategies.” ABA President Rob Nichols publicly warned that “trillions of dollars could leave the banking system.”

These figures are likely worst-case scenarios, but they underscore the level of anxiety within the banking sector.

5. The Crypto Industry’s Rebuttal

The crypto industry has pushed back strongly. In December, the Blockchain Association released its own analysis, arguing that there is no empirical evidence of disproportionate deposit outflows caused by stablecoin adoption.

From this perspective:

- Stablecoins are primarily used for payments, trading, and settlement, not as long-term savings vehicles.

- Yield programs on exchanges often reflect marketing incentives or operational efficiencies rather than systemic risk.

- Prohibiting yield entirely would entrench incumbent banks and reduce consumer choice.

Crypto advocates argue that competition from stablecoins could actually encourage banks to innovate, improve digital services, and offer more attractive products.

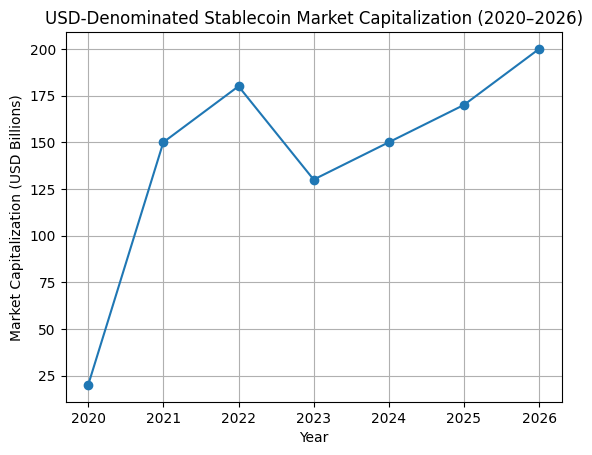

6. Broader Market Context: Stablecoins in 2026

To understand why this debate matters, it is essential to view it in the broader context of stablecoin adoption.

Growth of the Global Stablecoin Market (USD-denominated)

(A line chart showing total stablecoin market capitalization in USD from 2020 to 2026.)

By early 2026, the total market capitalization of USD-pegged stablecoins has rebounded strongly, driven by:

- Increased on-chain settlement in DeFi and centralized exchanges

- Cross-border payments and remittances

- Corporate treasury experimentation

Stablecoins are no longer a niche product. They are becoming core infrastructure for digital finance, which explains why traditional banks are increasingly alarmed.

7. Implications for Investors and Builders

For readers interested in new crypto assets, yield opportunities, and practical blockchain use, the outcome of the GENIUS Act debate is critical.

Yield Strategies

If lawmakers side with the banks and extend the prohibition to exchanges and affiliates, yield on stablecoins may shift further toward:

- DeFi protocols

- Synthetic or tokenized money-market products

- Offshore or non-U.S. platforms

Product Design

Projects building wallets, exchanges, or payment systems in the U.S. will need to carefully separate:

- Payments and custody functions

- Yield-generating features

- Affiliate and partner relationships

Regulatory Arbitrage

Tighter U.S. rules could accelerate innovation in jurisdictions with clearer or more permissive frameworks, intensifying global competition.

8. Conclusion: A Defining Moment for Digital Dollars

The clash over the GENIUS Act highlights a fundamental question: Should stablecoins remain neutral payment instruments, or are they evolving into yield-bearing financial products?

Regional banks see existential risk in the latter scenario, fearing erosion of their deposit base and lending capacity. Crypto firms see an opportunity to modernize money, improve efficiency, and expand access.

For investors and practitioners, this is not merely a regulatory skirmish—it is a signal of how digital dollars will be allowed to function in the world’s largest economy. The final shape of the GENIUS Act will likely influence global standards for stablecoins, yield, and the future relationship between banks and blockchain.