Key Points :

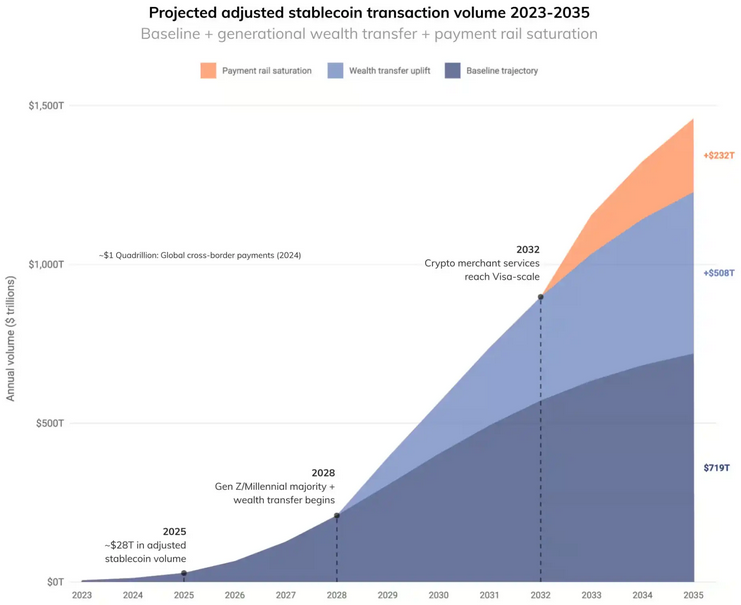

- Adjusted stablecoin transaction volume reached $28 trillion in 2025 and is growing rapidly

- Could reach $719 trillion baseline or $1.5 quadrillion ($1,500 trillion) by 2035

- Growth driven by real economic usage, not speculative trading

- $100 trillion generational wealth transfer is a major catalyst

- Stablecoins expected to rival Visa and Mastercard in transaction volume

- POS adoption may turn stablecoins into invisible payment infrastructure

1. A Structural Shift: From Speculation to Real Economic Infrastructure

The latest analysis from Chainalysis signals a profound transformation in the role of stablecoins within the global financial system. No longer confined to trading pairs on cryptocurrency exchanges, stablecoins are increasingly becoming a foundational layer for real-world economic activity.

What makes this report particularly important is its focus on “adjusted stablecoin transaction volume.” Unlike raw blockchain data—which is often inflated by bot activity, arbitrage loops, and internal exchange transfers—this adjusted metric isolates genuine economic transactions. This includes payments, remittances, settlement flows, and business-related transfers.

From this lens, the growth trajectory becomes far more meaningful. In 2025 alone, adjusted stablecoin volume reached approximately $28 trillion, already rivaling major traditional financial rails. Since 2023, this metric has grown at an astonishing compound annual growth rate (CAGR) of 133%, suggesting that adoption is not only accelerating but compounding.

This is not a speculative bubble—it is infrastructure being built in real time.

2. Forecasting the Future: From $719 Trillion to $1.5 Quadrillion

Looking forward, Chainalysis provides two scenarios:

Baseline Scenario

- By 2035, stablecoin transaction volume could reach $719 trillion annually

Macro-Accelerated Scenario

- With favorable macroeconomic and adoption conditions, this could expand to $1.5 quadrillion annually

To put this into perspective, the entire global cross-border payments market today is significantly smaller than these projections. If realized, stablecoins would not merely complement traditional finance—they would surpass it in scale.

Stablecoin Growth Projection

This projection reflects a deeper structural trend: financial infrastructure is being rebuilt on programmable, borderless systems.

3. The Generational Catalyst: $100 Trillion Wealth Transfer

One of the most underestimated drivers of this transformation is demographic.

Starting around 2028, a massive intergenerational wealth transfer is expected as assets move from Baby Boomers to Millennials and Generation Z. Estimates suggest this transfer could exceed $100 trillion globally.

This matters because:

- Younger generations are significantly more crypto-native

- Nearly 50% already have exposure to digital assets

- They are more comfortable with self-custody, digital wallets, and blockchain-based finance

According to the analysis, this wealth transfer alone could contribute approximately:

- $508 trillion in additional annual stablecoin transaction volume by 2035

This is not just capital moving—it is behavior changing. Wealth is shifting into the hands of individuals who fundamentally trust digital financial systems.

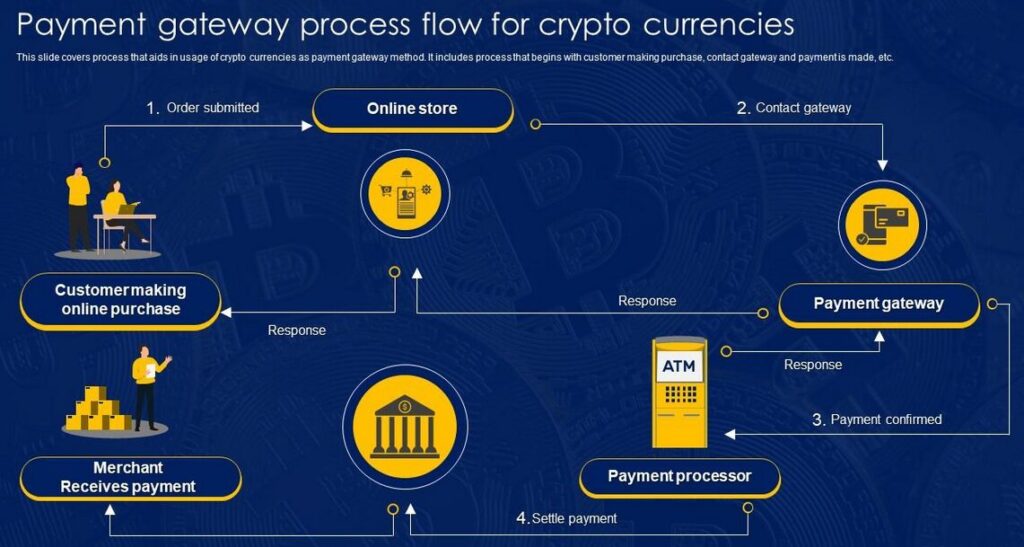

4. The POS Revolution: When Crypto Becomes Invisible

The next major turning point is Point-of-Sale (POS) adoption.

Today, paying with cryptocurrency is still a conscious choice. Users must decide to use crypto, often facing friction such as wallet management, gas fees, or conversion steps.

However, once stablecoins are integrated directly into merchant systems:

- Payments become seamless and automatic

- Users may not even realize they are using blockchain

- Stablecoins function similarly to credit cards or mobile payments

At this stage, stablecoins evolve into “invisible infrastructure.”

This mirrors the evolution of the internet:

- Early users were aware of protocols like HTTP

- Today, users simply “use apps”

The same will happen with money.

Stablecoin POS Integration Concept

5. Competing with Legacy Giants: Visa and Mastercard

Chainalysis projects that between 2031 and 2039, stablecoin transaction counts could reach parity with:

- Visa

- Mastercard

This is a critical milestone.

Unlike traditional networks, stablecoins offer:

- 24/7 settlement

- Near-instant cross-border transfers

- Lower fees (especially for remittance corridors)

- Programmability (smart contracts, conditional payments)

In effect, stablecoins are not just competing with payment networks—they are redefining what a payment network is.

6. Real-World Use Cases: Where Stablecoins Are Already Winning

Stablecoins are already dominating in several key areas:

1. Cross-Border Remittances

Traditional remittance systems can take days and charge 5–10% fees. Stablecoins reduce this to minutes and often less than 1%.

2. Emerging Markets

In countries with unstable currencies, USD-pegged stablecoins provide a store of value and medium of exchange.

3. Institutional Settlement

Financial institutions are beginning to use stablecoins for liquidity management and real-time settlement.

4. On-Chain Finance (DeFi)

Stablecoins are the backbone of decentralized finance, enabling lending, trading, and yield generation.

7. Risks and Constraints: What Could Slow Growth

Despite the bullish outlook, several risks remain:

- Regulatory uncertainty across jurisdictions

- Central bank digital currencies (CBDCs) competing with stablecoins

- Issuer risk (e.g., reserve transparency and redemption guarantees)

- Fragmentation across chains and ecosystems

However, even under conservative assumptions, growth remains substantial.

8. Strategic Implications for Builders and Investors

For your target audience—those seeking new crypto assets, revenue streams, and practical blockchain applications—the implications are clear:

1. Infrastructure Is the Opportunity

The biggest value will not just be in tokens, but in:

- Payment gateways

- Wallet UX layers

- Compliance tooling (KYC, Travel Rule)

- Cross-chain settlement systems

2. Stablecoin-First Design

Future applications should assume:

- Stablecoins as the default unit of account

- Fiat abstraction happening in the background

3. Monetization Models

Revenue will increasingly come from:

- Transaction fees (low but high volume)

- FX spreads

- Financial services layered on top

4. Regulatory Alignment Is Critical

Especially in jurisdictions like the Philippines or Japan, compliance-first architecture will be a competitive advantage.

Conclusion: The Quiet Reinvention of Money

Stablecoins are not just another crypto trend—they represent a fundamental redesign of global financial infrastructure.

From $28 trillion in real economic usage today to potentially $1.5 quadrillion by 2035, the trajectory is clear. Driven by generational change, technological integration, and real-world utility, stablecoins are on track to become:

- The backbone of global payments

- A bridge between traditional finance and blockchain

- The default settlement layer for digital economies

The most important shift, however, may be psychological.

In the future, people will not say they are “using crypto.”

They will simply pay, send, and transact—without thinking about the system underneath.

That is when stablecoins win.