Main Points :

- Legendary investor Stanley Druckenmiller predicts stablecoins could dominate global payments within 10–15 years.

- Blockchain-based payment rails are expected to outperform traditional systems in speed, cost efficiency, and transparency.

- Major payment companies and financial institutions are already experimenting with stablecoin settlement infrastructure.

- Regulatory frameworks such as new digital asset laws are accelerating adoption by clarifying compliance rules.

- Despite optimism about blockchain payments, Druckenmiller remains skeptical about cryptocurrencies like Bitcoin as long-term stores of value.

- The debate between “payments utility” vs. “store of value” may define the next phase of the crypto industry.

1. The Stablecoin Payment Revolution

[Stablecoin Payments Network Diagram]

The global financial system may be approaching a structural transformation. According to legendary investor Stanley Druckenmiller, blockchain-based tokens—particularly stablecoins—could become the backbone of global payment systems within the next decade to decade and a half.

Druckenmiller made this observation during an interview recorded with Morgan Stanley. While the interview itself reflects a personal viewpoint, it aligns with broader trends unfolding across the financial sector.

Stablecoins—cryptocurrencies designed to maintain a stable value by being pegged to assets such as the U.S. dollar—have grown from experimental instruments in the crypto ecosystem into serious infrastructure candidates for international payments.

Druckenmiller emphasized that blockchain tokens could dramatically improve the productivity of payment networks. Traditional payment rails often require multiple intermediaries, settlement delays, and significant operational costs. Blockchain technology, by contrast, allows transactions to be processed directly between parties with near-instant settlement.

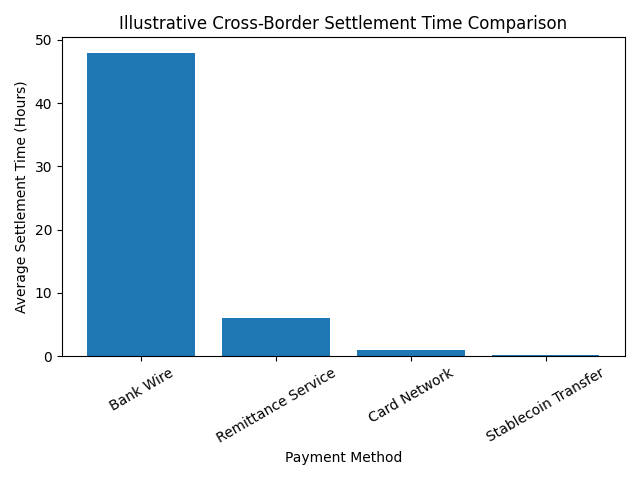

This efficiency is particularly evident in cross-border payments, which historically have been slow and expensive. Stablecoin transfers can settle within minutes or even seconds while significantly reducing transaction fees.

According to Druckenmiller, the benefits of blockchain settlement are so compelling that most payment systems could eventually migrate to stablecoin infrastructure within 10–15 years.

Such a transformation would represent one of the most significant changes to the financial system since the rise of digital banking.

2. Why Stablecoins Are Gaining Momentum

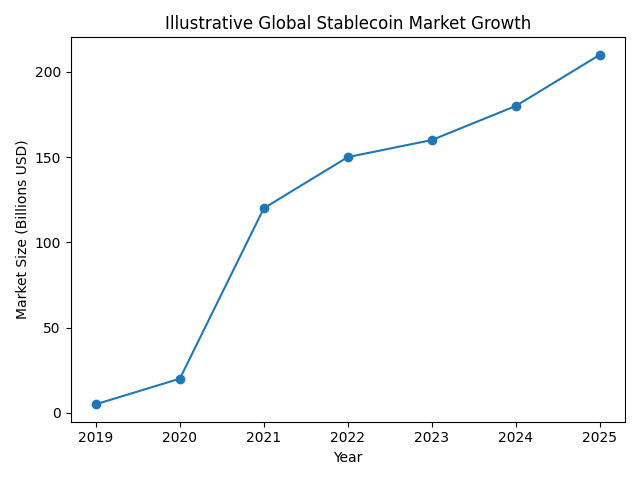

The increasing relevance of stablecoins is not merely theoretical. Over the past several years, the total market capitalization of stablecoins has surged dramatically.

[Global Stablecoin Market Growth Chart]

Several key factors are driving this expansion.

Speed and Settlement Efficiency

Traditional cross-border payments often rely on correspondent banking networks. Each intermediary introduces delays and fees. In contrast, blockchain-based transfers settle directly on distributed ledgers, eliminating many middlemen.

Lower Costs

Transaction costs on stablecoin networks are often far lower than those charged by international wire services or remittance providers. This makes stablecoins particularly attractive for remittance corridors and international commerce.

Programmability

Stablecoins are programmable assets. Smart contracts allow payments to be automated, conditional, or integrated directly into business processes.

For example:

- Supply chain payments can be triggered automatically when goods arrive.

- Escrow contracts can release funds when conditions are met.

- Decentralized finance platforms can use stablecoins as collateral or liquidity.

Global Accessibility

Unlike traditional banking systems that require extensive infrastructure, stablecoin networks can be accessed using only a smartphone and internet connection.

This makes them particularly relevant for financial inclusion, especially in emerging markets where banking penetration remains limited.

3. Traditional Finance Is Already Moving In

Druckenmiller’s prediction is not occurring in a vacuum. Traditional financial institutions have already begun integrating stablecoin infrastructure into their operations.

Major payment companies such as Western Union, MoneyGram, and digital payment platforms have announced plans to explore or deploy stablecoin-based payment solutions.

In many cases, these firms are experimenting with stablecoins for cross-border settlement. Instead of transferring funds through legacy systems, institutions can use stablecoins as settlement layers before converting back into local currencies.

Banks are also exploring stablecoin settlement systems for wholesale financial transactions.

Several developments have accelerated this shift:

- Clearer regulatory frameworks for digital assets

- Increased institutional participation in crypto markets

- Growing demand for faster international settlement

- Expansion of blockchain infrastructure

Regulatory clarity has been especially important. In the United States, for example, new legislation such as the GENIUS Act, passed in 2025, established a framework for payment companies to provide digital asset services.

Regulatory developments like these reduce uncertainty and allow financial institutions to experiment with blockchain technology while remaining compliant with financial laws.

4. The Productivity Argument

One of Druckenmiller’s strongest arguments concerns productivity gains.

Payments may appear simple on the surface, but they represent an enormous global industry involving banks, clearing houses, card networks, remittance providers, and settlement systems.

Each layer introduces operational costs.

Blockchain-based systems can collapse many of these layers into a single shared infrastructure.

For example:

Traditional payment flow:

- Sender bank

- Correspondent bank

- Clearing network

- Receiving bank

- Recipient

Blockchain payment flow:

- Sender wallet

- Blockchain settlement

- Recipient wallet

This structural simplification dramatically reduces costs and settlement times.

For global commerce, the economic impact could be significant.

Even small efficiency gains in payment systems can translate into billions of dollars in savings annually.

5. Skepticism About Crypto as a Store of Value

Despite his optimism about blockchain payments, Druckenmiller remains skeptical about cryptocurrencies as stores of value.

This view places him in contrast with many Bitcoin advocates who argue that Bitcoin functions as “digital gold.”

Druckenmiller described cryptocurrency as somewhat like “a solution looking for a problem.”

While he acknowledged the growing popularity of crypto assets, he suggested their value may depend largely on brand perception rather than intrinsic necessity.

Gold, in contrast, has served as a store of value for thousands of years.

Druckenmiller has previously stated that gold’s 5,000-year history gives it credibility that cryptocurrencies have yet to establish.

That said, he also acknowledged the possibility that Bitcoin could still function as a store of value for certain groups of investors.

In fact, he has indicated that although he currently does not hold Bitcoin, he might consider doing so.

This nuanced stance reflects the broader debate within the financial world.

6. The Emerging Two-Track Crypto Economy

The future of digital assets may ultimately evolve along two distinct tracks:

1. Blockchain as Financial Infrastructure

In this model, blockchain networks serve primarily as settlement layers for financial transactions.

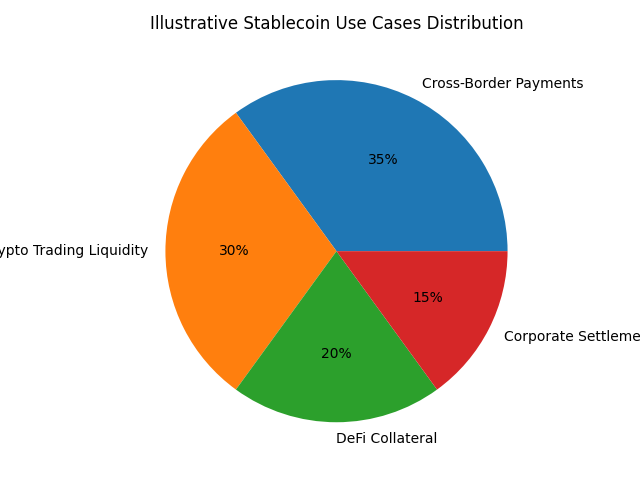

Stablecoins play a central role, enabling:

- Cross-border payments

- Global remittances

- Institutional settlement

- Corporate treasury transfers

- Digital commerce

2. Crypto as Digital Scarcity Assets

In parallel, certain cryptocurrencies—especially Bitcoin—may continue to function as speculative or alternative store-of-value assets.

These two roles are not mutually exclusive.

However, they represent fundamentally different economic narratives.

One focuses on utility and productivity, while the other emphasizes scarcity and monetary independence.

7. Institutional Adoption Is Accelerating

Recent developments suggest the institutionalization of stablecoins is accelerating.

Examples include:

- Asset managers launching stablecoin-based settlement networks

- Banks issuing tokenized deposits on blockchain platforms

- Governments exploring central bank digital currencies (CBDCs)

- Payment platforms integrating stablecoin rails

Large financial institutions such as JPMorgan, Visa, and PayPal have all conducted experiments with blockchain payments or stablecoin infrastructure.

These experiments are gradually transforming blockchain technology from a niche innovation into a mainstream financial tool.

8. Implications for Investors and Builders

For readers interested in discovering new crypto opportunities and practical blockchain applications, several implications emerge from these trends.

Stablecoin Infrastructure

Projects focused on payment rails, compliance tools, and liquidity networks may become increasingly important.

Tokenized Finance

Tokenized assets—such as tokenized treasury bills or deposits—could merge traditional finance with blockchain infrastructure.

Cross-Border Settlement Platforms

Businesses enabling faster international payments may see growing demand.

Regulatory-Compliant Blockchain Services

As regulation matures, compliant infrastructure providers will likely gain an advantage over purely experimental crypto projects.

Conclusion

Stanley Druckenmiller’s perspective highlights a critical shift underway in the digital asset industry.

While debates about cryptocurrency as a store of value continue, the practical utility of blockchain technology—especially stablecoins—has become increasingly difficult to ignore.

Over the next 10 to 15 years, stablecoins could transform the global payments landscape by offering faster settlement, lower costs, and programmable financial infrastructure.

At the same time, the role of cryptocurrencies like Bitcoin may continue to evolve as investors debate their long-term monetary significance.

For entrepreneurs, investors, and policymakers, the key insight is clear:

The future of blockchain may not be defined solely by speculative assets, but by the reinvention of the global payment system itself.