Main points :

- Global stablecoin supply sits around the high-$260B to $270B range as of August 2025, with momentum accelerating since the U.S. GENIUS Act became law in June. USDT (

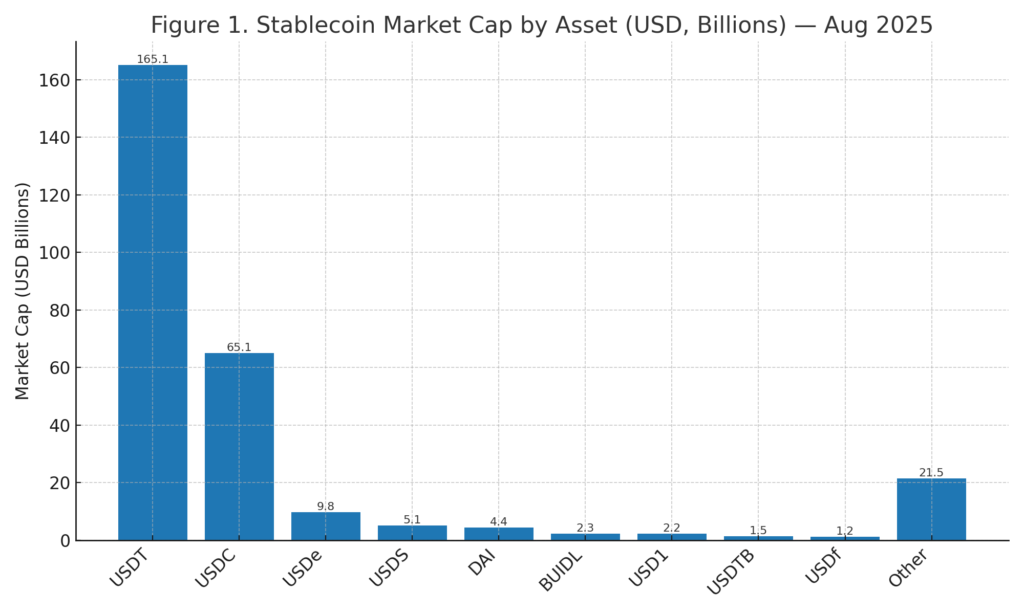

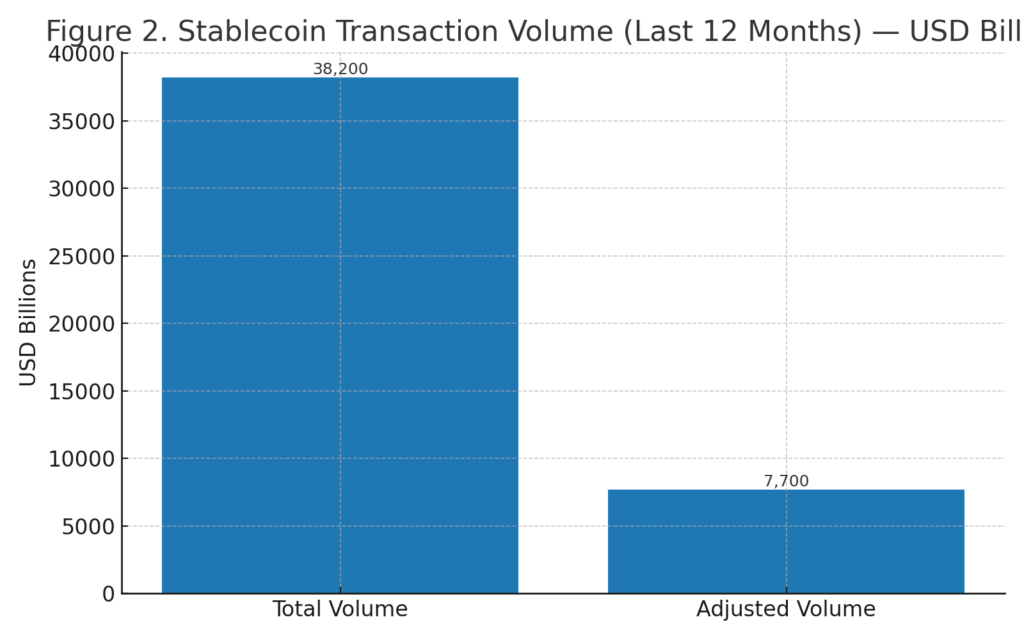

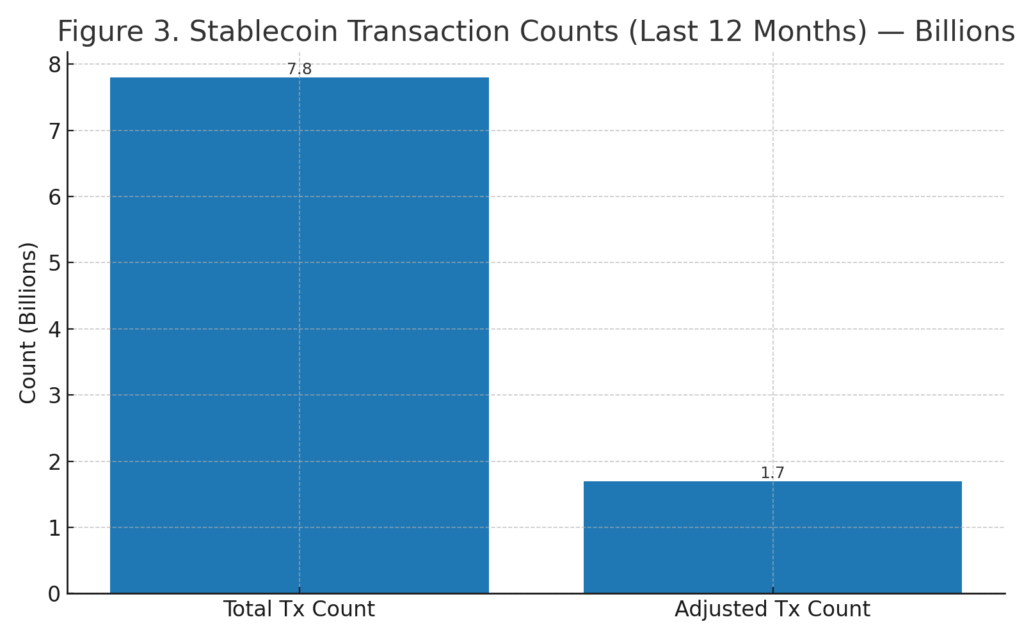

$165B) and USDC ($65B) still dominate; Ethena’s USDe has surged to ~$9–10B to become the #3 stablecoin. - On-chain activity is enormous: $38.2T total stablecoin transfer volume over the past 12 months (adjusted: $7.7T), with 7.8B total transactions (adjusted: 1.7B). Retail-sized payments account for the majority of transaction count, signaling day-to-day usage.

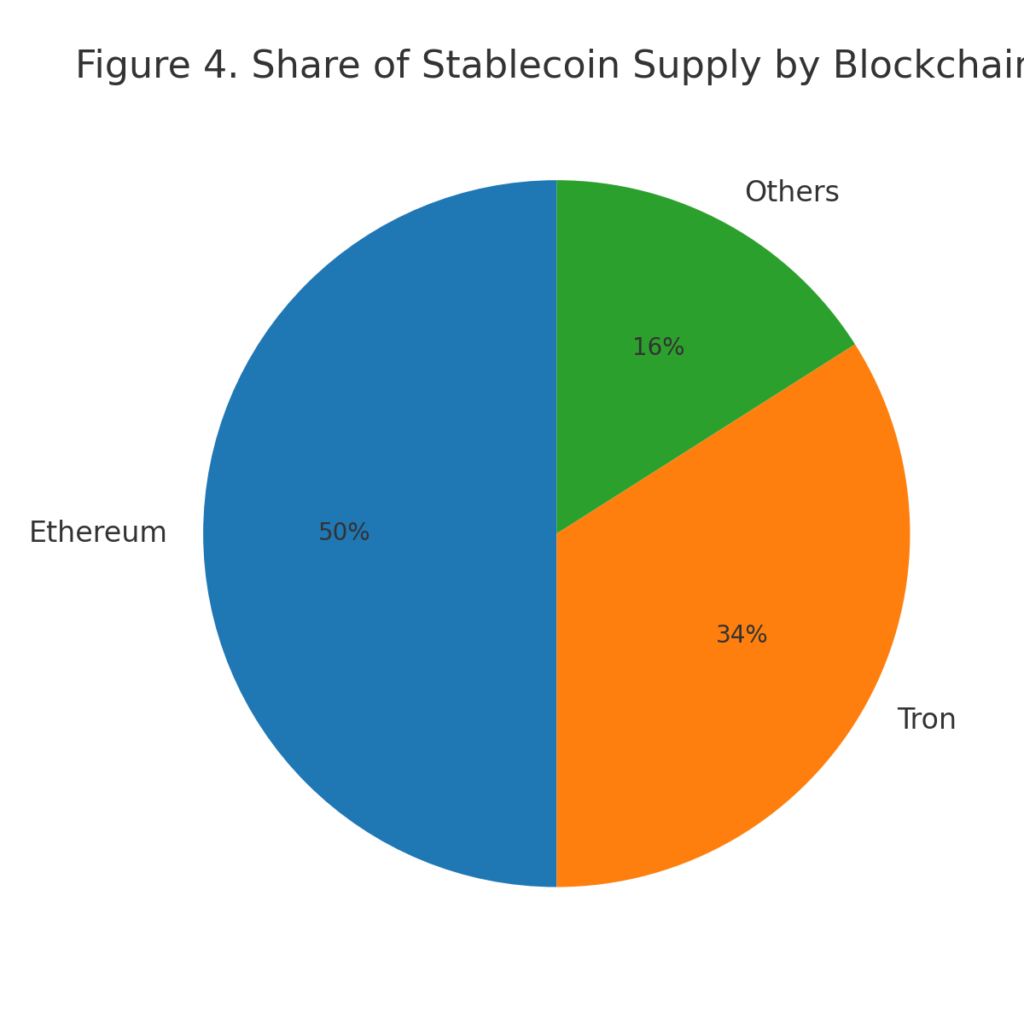

- Ethereum and Tron host ~84% of stablecoin supply; Ethereum ~50%, Tron ~35%, with Tron’s low fees supporting USDT’s emerging-market ubiquity.

- Regulation is finally clarifying: the U.S. GENIUS Act (now law) sets a federal framework for payment stablecoins; the CLARITY Act advances CFTC/SEC delineation; the EU’s MiCA stablecoin rules entered into force in mid-2024; Japan treats fiat-redeemable stablecoins as “electronic payment instruments.”

- New entrants and use cases: Ripple’s RLUSD (NYDFS-approved) is integrated into Ripple Payments; PayPal’s PYUSD expands and is preparing a Stellar rollout; tokenized money-market funds such as BlackRock’s BUIDL have scaled to multi-billion AUM, bridging TradFi and DeFi liquidity.

[Insert Figure 1 here: “Stablecoin Market Cap by Asset (USD, Billions) — Aug 2025”]

1) Market snapshot: who holds the float?

As of early August 2025, stablecoin market cap data sits just under the $270B mark, up sharply in recent weeks. USDT remains the anchor at roughly $165B, with USDC ~ $65B. USDe has sprinted into third place at ~$9–10B, reflecting the rise of yield-mechanism stablecoins that aim to satisfy institutional demand under clearer rules. The long tail includes USDS (Sky), DAI, PYUSD, and tokenized cash products (BUIDL) now used as collateral and liquidity sources.

Why that matters: float size drives network effects (market-maker inventory, FX rails, redemption depth). For builders, liquidity routing and treasury operations increasingly assume multiple stablecoin types (fiat-backed, crypto-collateralized, and tokenized fund shares) coexisting.

2) How the dollars move on-chain

Stablecoins processed $38.2T in total transfer volume over the past 12 months; Visa’s adjusted methodology (which filters internal/self transfers) still shows a hefty $7.7T. Transaction counts tell a similar story: 7.8B gross and 1.7B adjusted. In short, this is a payments rail at global scale—already.

The article you provided also notes retail-sized payments account for a majority of transactions by count (over half), though still a small share by volume—consistent with micropayments, P2P transfers, and merchant acceptance where low fees and instant settlement matter most.

[Insert Figure 2 here: “Stablecoin Transaction Volume (Last 12 Months) — USD Billions”]

[Insert Figure 3 here: “Stablecoin Transaction Counts (Last 12 Months) — Billions”]

Implication for product teams: If you build consumer flows (wallets, POS, remittances), focus on fail-safe on/off-ramps, human-readable identifiers, dispute-minimizing UX, and transparent fees. If you serve institutions, settlement finality, reconciliation tooling, and compliance attestations will be competitive moats.

3) The chains that matter (for now)

Ethereum remains the primary settlement layer for fiat-backed coins and tokenized funds (compliance toolkits, custody, and composability). Tron keeps a massive USDT footprint thanks to very low fees and wide exchange support, especially across emerging-market corridors. Together, the two chains account for ~84% of circulating stablecoins (Ethereum ~50%, Tron ~35%).

[Insert Figure 4 here: “Share of Stablecoin Supply by Blockchain”]

This duopoly will be tested as Solana, Base, and L2s keep improving throughput/fee economics and as custodians facilitate multi-chain issuance with consistent attestation standards.

4) Issuers & tokens to watch

Tether (USDT)

USDT’s ~$165B lead underpins exchange liquidity, OTC settlement, and cross-border transfers. On Tron it has become the defacto remittance rail in parts of LATAM, Africa, and Asia—helped by sub-cent fees and ubiquitous wallet support. Notably, several TRON-based tokens (including USDT) were granted authorized digital currency status in Dominica in 2022, enabling use for payments and taxes—an early example of a nation formalizing public-sector acceptance.

USD Coin (USDC)

With ~ $65B supply, USDC remains the preferred option for institutions requiring clearer reserve disclosures and U.S. banking rails. Expect continued growth where MiCA-compliant issuance in the EU and new U.S. rules favor audited, redeemable fiat-backed models.

Ethena (USDe)

USDe’s explosive climb (now around $9–10B) shows demand for “internet native” dollar exposure with programmatic yield—especially post-GENIUS Act, where large custodians and on-chain venues enabled safer integrations. Risk management (hedging mechanics, custodial resilience) remains the focus, but scale is already material.

Sky (USDS) & DAI

MakerDAO’s ecosystem pivot to Sky/USDS—alongside the legacy DAI—has broadened collateral and governance. USDS printing crossed key milestones quickly in 2025, with integrations (including purchases by other protocols) hinting at deeper DeFi-to-DeFi linkage.

PayPal (PYUSD)

PYUSD is becoming more “payments-native”: rollout plans include Stellar support (pending NYDFS approval), and Xoom/Yellow Card integrations push remittances into real corridors at lower cost. PYUSD’s market cap has topped ~$1B as of August 2025, small versus USDT/USDC but strategically placed in merchant and consumer flows.

Ripple (RLUSD)

RLUSD received NYDFS approval in late 2024 and is now integrated in Ripple Payments for cross-border settlement, with Ripple continuing M&A (e.g., acquiring stablecoin platform Rail) to extend issuer and corridor coverage. Time-to-fiat and compliance traceability are the design center here.

Tokenized cash & MMFs (BUIDL)

BlackRock’s BUIDL—a tokenized USD liquidity fund—has grown to ~$2–3B+ and is now accepted as collateral at certain venues, showcasing how tokenized treasuries bridge TradFi yield with on-chain collateral needs. Expect more “fund-as-coin” assets to sit alongside USDT/USDC in institutional wallets.

5) Regulation: from uncertainty to playbooks

United States. The GENIUS Act of 2025 is now law, establishing a federal regime for payment stablecoins (BSA/AML applicability, reserve, issuance, and supervision standards). The CLARITY Act (advancing through Congress) would assign the CFTC a lead role over digital commodity spot markets and define new registrant classes, easing the longstanding SEC/CFTC ambiguity. These moves have coincided with higher issuance and more aggressive product roadmaps.

European Union. The MiCA stablecoin regime (for ARTs & EMTs) has applied since June 30, 2024, with full MiCA applicability from Dec 30, 2024. ESMA/EBA guidance continues to tighten around listing non-compliant tokens and investor protections (notably, redemption rights), pushing EU-facing issuance toward fully supervised models.

Japan. Since 2023, fiat-redeemable stablecoins are treated as “electronic payment instruments” under the Payment Services Act; issuance by banks, trust companies, and registered funds transfer providers is permitted, triggering a wave of pilots by financial institutions and fintechs.

Strategic takeaway: global corridors will fragment by rule set (U.S. GENIUS/CLARITY vs. EU MiCA vs. JP PSA), but interoperable attestation (audits, segregation, disclosures) is becoming a de-facto standard. Issuers and gateways that can present consistent, machine-readable proofs will win enterprise and public-sector deals.

6) Where builders and investors can find the next $ opportunities

A. Remittances & merchant acquiring. Target corridors with fee-sensitive flows and weak FX infrastructure; package stablecoin rails with compliant on/off-ramps, clear refunds/dispute policies, and automated tax/VAT reporting.

B. Treasury & yield. Tokenized treasuries (e.g., BUIDL) as treasury buffers; stablecoin-denominated cash management with automated sweeps between fiat, on-chain dollars, and fund tokens depending on liquidity needs and compliance constraints.

C. DeFi liquidity & prime brokerage. Institutional perps/spot desks increasingly accept tokenized fund collateral and prefer stablecoin settlement; this is a revenue lane for custody, collateral utilities, and risk engines.

D. Compliance rails. Post-GENIUS/MiCA, productize reserve transparency, chain-forensics-assisted KYC/KYB, Travel Rule messaging, and sanctions-screened payout networks. In Japan, partner with licensed EPIs to issue/accept JPY-linked tokens under PSA.

E. Programmable commerce. Embed “dollars with rules” (payment conditions, revenue splits, time locks) into B2B SaaS, marketplaces, and IoT contexts. The narrative is moving from speculation to receivables and settlement automation.

7) Risks to track

- Regulatory divergence: fungible tokens issued across jurisdictions (EU vs. non-EU) may pose redemption and supervisory headaches; follow ESMA/EBA statements closely.

- Custody/attestation quality: proof of reserves, segregation of assets, and bank partner risk remain core.

- Mechanism risk: for yield-bearing and delta-hedged designs (e.g., USDe), stress-scenario behavior must be continuously audited.

- Concentration: chain and issuer concentration could become a policy target if systemic footprints expand.

Conclusion

Stablecoins are no longer a crypto side show—they are the on-chain money rail. The last 12 months delivered $38.2T of notional value transfer, a multi-billion rise in tokenized cash products, and the first credible federal rulebook in the U.S. Builders should assume a multi-asset, multi-chain future and design for attestation, settlement finality, and regulated liquidity. For investors hunting yield and growth, the action is where compliance, utility, and distribution intersect.