Key Points :

- The Bank of Japan (BOJ) Deputy Governor publicly declared that stablecoins may become a core component of global cross-border payments, signalling a major shift in central bank thinking.

- Traditional international payment systems suffer from cost, speed, and transparency inefficiencies; stablecoins promise to mitigate those by leveraging blockchain rails.

- The BOJ emphasises that regulation and risk-management must accompany innovation: the goal is to combine financial stability with the promise of modern payments.

- Japan is positioning itself strategically to be a payment hub in Asia, using regulatory clarity and stablecoin technology to strengthen its global role.

- For investors and practitioners in blockchain and crypto-assets, stablecoins now warrant re-thinking as infrastructural plays rather than merely transactional tokens.

- The shift from short-term speculation to long-term infrastructure investment is emerging: careful project selection, regulatory compliance and staying ahead of the curve matter more than ever.

1. The BOJ Deputy Governor’s Declaration: Stablecoins as the “Future of Cross-Border Payments”

The BOJ’s Deputy Governor recently made headlines by asserting that stablecoins could serve as a new core component of the international payments architecture. According to reports, he suggested that stablecoins might even partially replace bank deposits in the global financial system.

This is remarkable: a major central banker openly acknowledges that a sub-category of crypto-assets could anchor global payment flows. It signals a turning point in how monetary-policy and infrastructure players view tokenised cash. For practitioners in blockchain and crypto, that marks a clear shift from speculation to recognition of stablecoins as part of the plumbing of global finance.

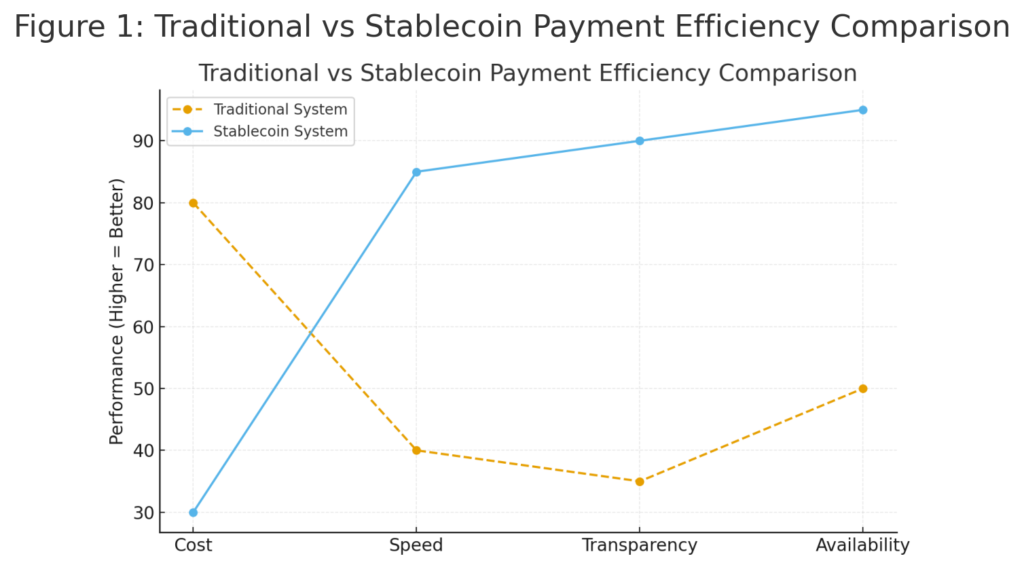

The BOJ’s reasoning is rooted in the inefficiencies of current systems: cross-border transfers are slow, costly, opaque and rely on multiple intermediaries. By contrast, stablecoins—when properly designed and regulated—offer faster settlement, 24/7 availability and transparency across borders.

In short: what was once a fringe topic for crypto-enthusiasts is now under serious consideration by central banks as a potential building block of future payment rails.

2. Addressing the Challenges of Traditional International Payments

One of the central reasons stablecoins are gaining institutional focus is the acute pain-points of legacy cross-border payment systems. Multiple correspondent banks, time-zones, FX costs, manual compliance steps — these mean high cost, slow speed and limited transparency.

By contrast, tokenised cash (stablecoins) on blockchain networks promise:

- Instant or near-instant settlement across borders

- Lower transaction fees due to fewer intermediaries

- Transparency of value movement and settlement status

- 24/7 global rails independent of banking hours

For example, a July 2025 report by consulting firm McKinsey & Company noted that stablecoins have doubled in circulation over the past 18 months and although their volume still represents less than 1 % of global money flows, they are rapidly evolving as a payment alternative.

What this means for blockchain practitioners is: when one considers building or investing in stablecoins or payment-rail projects, infrastructure readiness, cross-border capability and settlement finality become key differentiators.

3. Balancing Innovation with Risk: The Central Bank’s View

The BOJ’s remarks also emphasise that embracing stablecoins is not simply about innovation—it must go hand-in-hand with risk management. As stablecoins possibly edge into functions historically fulfilled by bank deposits, questions of financial stability, regulatory oversight and consumer protection become paramount.

From the central bank viewpoint, the following risks are top of mind:

- Payment-system stability: if stablecoins are widely used without proper reserves and redemption infrastructure, runs or peg breaks could occur.

- Regulatory arbitrage and fragmentation: differing national rules could lead to mismatches in oversight and expose systemic risk.

- Monetary sovereignty and deposit substitution: if stablecoins issued privately begin acting like bank deposits, this may erode traditional banking models and raise policy challenges.

Academic research supports these concerns: one recent study proposed a hybrid architecture in which private stablecoin issuers are backed by central-bank reserves and interoperable rails to reduce fragility in stress periods.

Therefore, for blockchain implementers and investors: it is no longer enough to build fast and cheap rails. The credibility of the stablecoin—what underlying assets back it, how redemption works, how compliant the governance is—is becoming critical.

4. Japan’s Strategic Intent: Asia’s Payment Hub and Regulatory Advantage

The BOJ’s interest is not just ideological—it is tethered to strategic national positioning. Japan appears to be signalling its ambition to become a regional payments hub, particularly within Asia, where cross-border payment inefficiencies remain most acute.

Japan’s approach seems two-pronged:

- Create a regulatory regime that gives clarity and trust to stablecoin issuers and operators.

- Drive collaboration among Japanese banks, fintech and cross-border corridors to launch yen-pegged or Asia-centric stablecoins.

By doing so, Japan can export its financial-system credibility, Japanese banks’ liquidity and a trusted regulatory framework into global payment corridors—especially in Asia where multi-currency and cross-border flows are heavy. This aligns with the BOJ’s comment about needing to adapt financial-regulation frameworks to new realities such as non-bank financial institutions and tokenised value.

For blockchain practitioners, this is a green-lighting signal: a jurisdiction is willing to support the role of stablecoins in global payments and is preparing the framework. That reduces execution risk and may increase first-mover advantage for projects aligned with these corridors.

5. Implications for Investors: Re-Evaluating Stablecoins as Infrastructure, Not Speculation

From an investment perspective, the BOJ’s stance offers important clues. Stablecoins should be reconsidered not merely as transactional assets, but as infrastructural plays in a broader modernization of payments. Two shifts are key:

5.1 From short-term speculation to infrastructure investment

Rather than treating stablecoin projects like high-volatility tokens for trading, the emerging mindset is: which stablecoin networks will underpin B2B cross-border flows, treasury operations, banking rails and enterprise-grade use-cases? A report by Fireblocks showed that 90 % of firms report taking action on stablecoins because of their payments potential; 48 % say speed is the top benefit.

Therefore, investors should ask: is the project built for scale? Is its infrastructure enterprise-grade (liquidity, compliance, settlement)? Does it aim for real-world use-cases?

5.2 Selection and long-term holding strategy

According to the source article, the critical questions for stablecoin-related investment are: Which stablecoins clear regulatory hurdles? Which enjoy public trust and central-bank or bank-grade backing? Projects that meet those will likely be winners in the long term.

For practitioners this means: don’t chase just the yield; evaluate governance, backing assets, redemption mechanics, compliance. And once a project meets those standards, a long-term “buy-and-hold” approach may make sense—as the infrastructure matures, growth may come from usage rather than token speculation.

6. Recent Trends & Data to Contextualise the Shift

To deepen the picture, let’s review recent data and trends:

- According to a McKinsey report, stablecoins are rapidly gaining traction: they are increasingly embedded into “multi-rail” payments (cards + A2A + stablecoin) in leading networks.

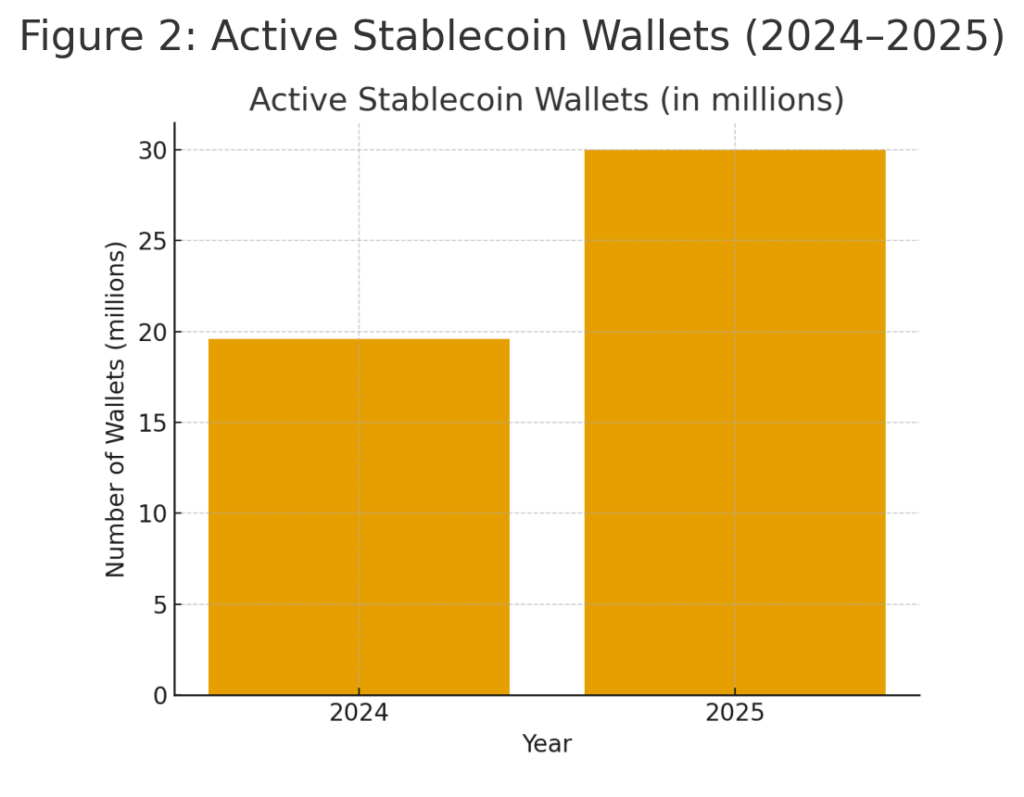

- A study shows that active stablecoin wallet addresses increased from 19.6 million (Feb 2024) to over 30 million (Feb 2025) — a +53 % year-on-year growth.

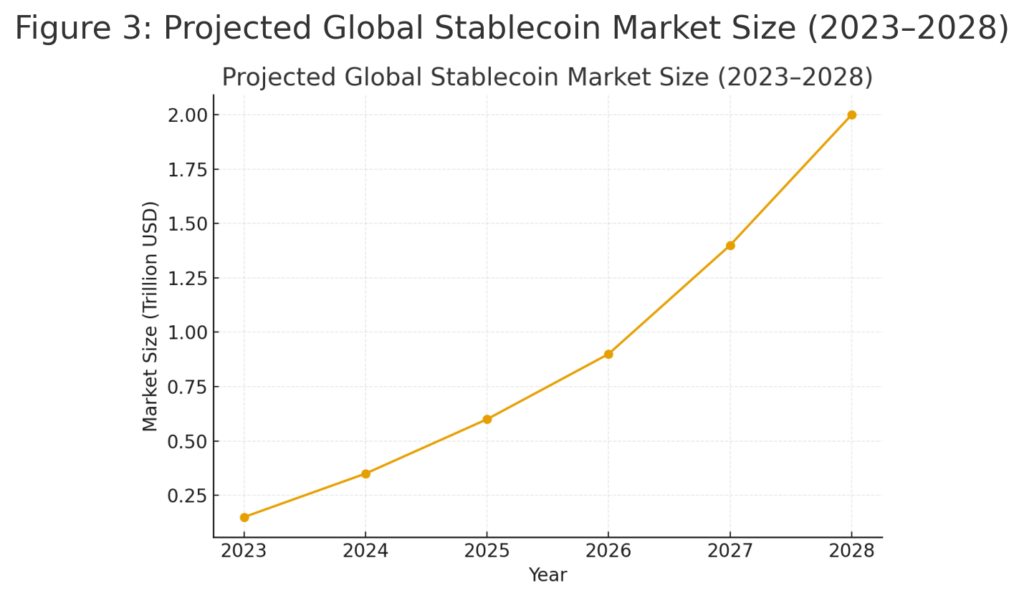

- Another report projects the stablecoin market could grow to US$2 trillion by end-2028.

- On the lending front, stablecoins are used as programmable money: August 2025 saw US$51.7 billion borrowed in stablecoins on-chain, with average loan size ~US$121,000.

These facts underscore that the trend is not hypothetical — stablecoins are scaling in usage, infrastructure and ambition.

7. What This Means for Blockchain Practitioners and New Crypto Projects

For people actively exploring new crypto-assets or blockchain use-cases, the following take-aways emerge:

- Design for real-world flows: If you’re building or examining a project, prioritise features such as liquidity management, redemption, regulatory compliance, treasury integration and cross-border settlement.

- Focus on corridor-specific value: Especially in Asia, Africa and Latin America, where traditional infrastructure is weak, stablecoin-based rails have outsized potential.

- Watch the regulatory architecture: With laws such as the GENIUS Act in the United States and regulations in the EU and Japan, projects aligned with compliant frameworks likely have lower execution risk.

- Invest for infrastructure value, not purely token appreciation: Projects that underpin payment flows, treasury solutions or enterprise corridors may deliver sustained value. Evaluate governance, backing, adoption strategy, network effect.

- Time-horizon matters: This is a longer-term megatrend, not a short-term trade. A stablecoin or payment-rail project that wins trust and usage today may deliver compounding benefits over years as the system grows.

Summary

The BOJ’s statement that stablecoins may become central to global payments marks a watershed moment. It reflects the evolving view of stablecoins—from crypto-niche assets to foundational components of global financial infrastructure. Traditional cross-border payment systems are burdened by cost, delay and opacity; blockchain-based stablecoins offer a compelling alternative. However, innovation must be balanced with risk oversight: central banks and regulators are signalling that stability, compliance and governance are non-negotiable.

Japan’s strategic positioning to become an Asia payment hub via regulatory clarity and stablecoin infrastructure presents opportunities for blockchain practitioners and investors alike. For those seeking the next crypto-asset or revenue stream, the message is clear: focus on underlying infrastructure, corridor-value and real-world adoption, and think long-term. Stablecoins are no longer just speculative tokens—they are potential building blocks for the next era of finance.