Main Points :

- JP Morgan sees the U.S. stablecoin market possibly becoming a zero-sum game, i.e. one issuer’s gain likely means another’s loss, rather than expansion of the overall pie.

- Key drivers: regulatory changes (e.g. the GENIUS Act), rising compliance demands, and new entrants like Tether’s USAT, Hyperliquid’s USDH, plus fintechs developing their own stablecoins.

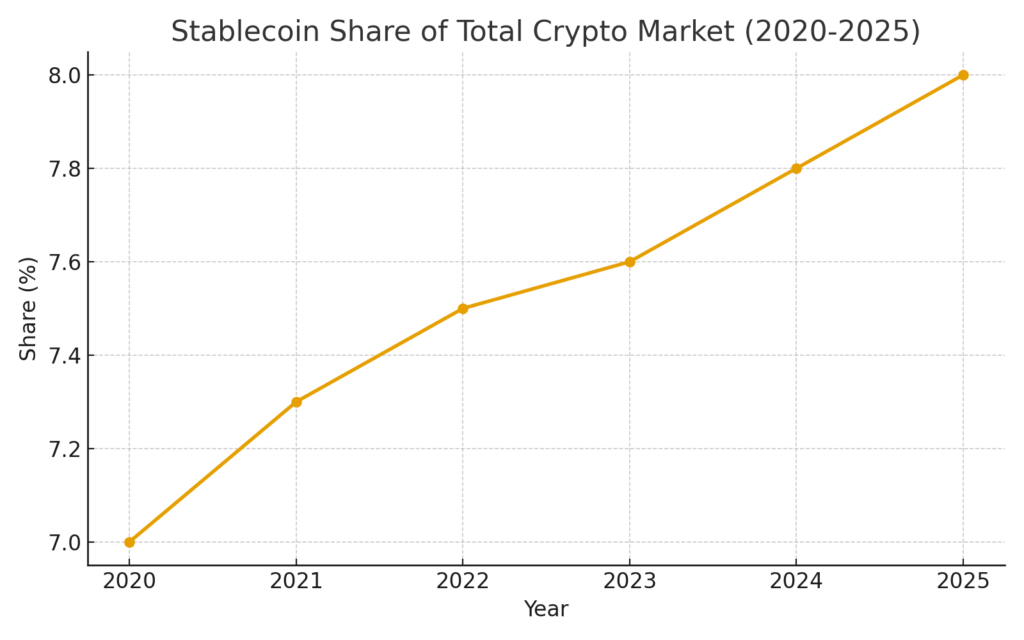

- The stablecoin market value is ~$270-$290 billion as of mid-2025, yet its share of the overall crypto market remains around 7-8% since 2020. Expansion of use cases—payments, cross-border transactions, institutional usage—is still limited.

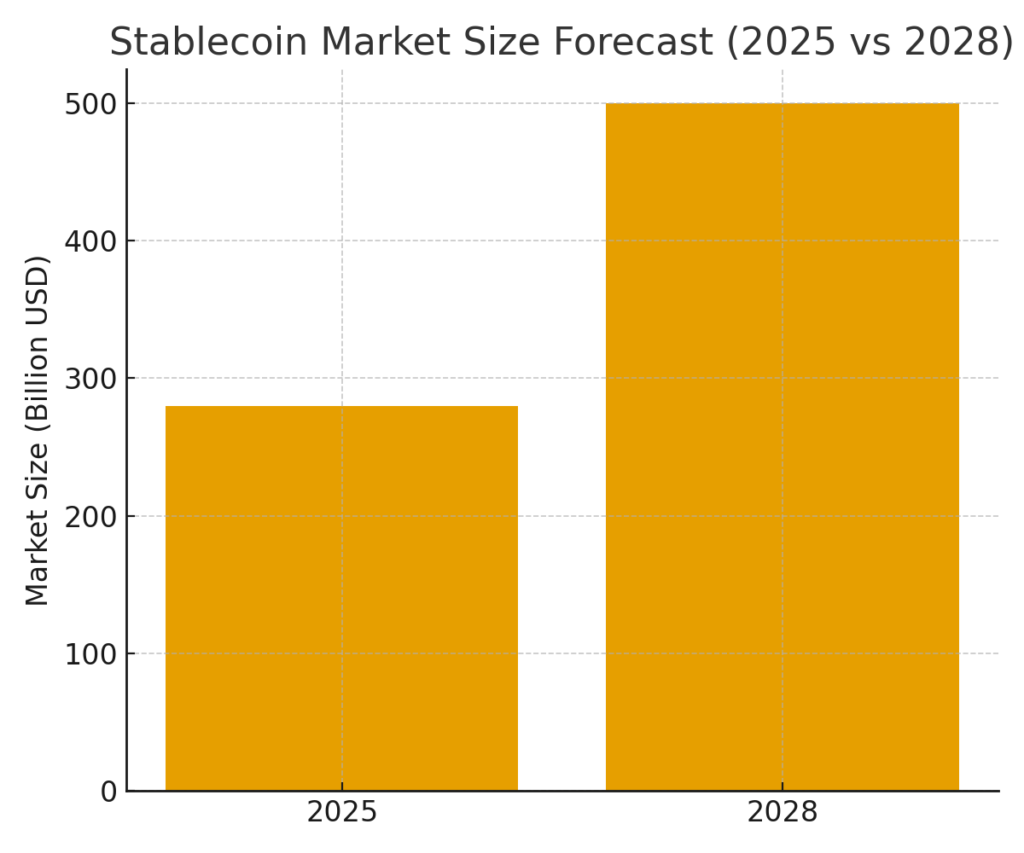

- Growth forecasts are being tempered: JP Morgan now predicts ~$500 billion by 2028, revising down from more optimistic earlier projections of $1-2+ trillion.

- Risks include fragmented liquidity, higher compliance/operational costs, regulatory uncertainty, and intensifying competition, possibly squeezing margins for new or smaller issuers.

- Opportunities lie in institutional demand, improved regulation (which can build trust), dedicated infrastructures (e.g., blockchains like “Arc” for USDC), and stablecoins tied to programmable finance/real-world assets.

1. What JP Morgan Is Saying: A Zero-Sum Stablecoin Market

JP Morgan analysts have warned that the U.S. stablecoin market may be entering a phase where competitive dynamics force issuers to simply reallocate market share among themselves, rather than generate net growth. In their study, the sector is valued at around $270-$290 billion in 2025. Although that is substantial, its proportion of the broader crypto market has remained stuck at roughly 7-8% since 2020.

They highlight that if the total size of the cryptocurrency market does not grow substantially, new stablecoin issuers will compete over existing demand rather than accessing new demand. Under such dynamics, one coin’s gain tends to come at another’s loss—a classic zero-sum game scenario.

2. Regulatory Shifts: The GENIUS Act and Its Effects

A major factor pushing toward this zero-sum scenario is regulatory change. In the U.S., the GENIUS Act—recently passed—establishes stricter standards for stablecoin issuers, including full backing by low-risk assets (cash, U.S. Treasury bills), stronger audit/reporting requirements, and superior oversight.

New entrants such as Tether are responding: USAT, Tether’s proposed fully compliant stablecoin, will hold reserves with Anchorage Digital (a federally chartered trust bank) to meet regulatory expectations. This contrasts with existing instruments (e.g. USDT) whose compliance is partial.

Meanwhile, regulation in other jurisdictions like the EU (MiCA) and Asia also increasingly demands transparency, reserves, and oversight, reinforcing standards that make issuance costlier and more demanding.

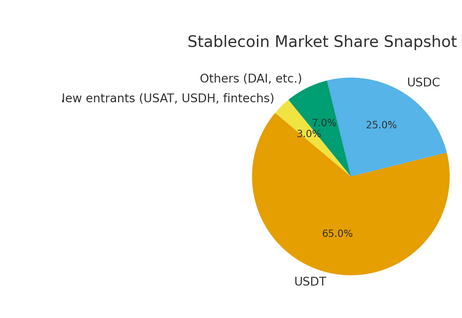

3. Key Players and New Entrants: Who’s Battling Whom

- Circle / USDC: Currently one of the biggest U.S. stablecoin issuers. It is trying to maintain its leadership via both regulatory compliance and infrastructure innovation (e.g. Arc, a dedicated blockchain for USDC).

- Tether / USAT: Tether plans to issue USAT, fully compliant with the GENIUS Act, to appeal to institutional trust and to reduce risks and costs tied to partial compliance. USAT is expected to compete directly with USDC.

- Hyperliquid / USDH: Another player, Hyperliquid, is launching USDH. The exchange already uses USDC heavily; by introducing USDH, it could shift usage and market share.

- Fintechs: Companies like Robinhood, Revolut, PayPal are reportedly developing stablecoins. Their large existing user bases and financial infrastructure could give them competitive advantages, especially in consumer payments or retail.

4. Growth Projections: Tempered Optimism

Early optimism in the stablecoin field forecast totals between $1-2 trillion (or more) in circulation within a few years. But JP Morgan has scaled back those expectations. Now, their projection is for the market to reach around $500 billion by 2028. This revision reflects recognition that:

- Payments and real-world adoption remain limited (roughly 6% of demand is from payments, per JP Morgan).

- Regulatory, technical, and competitive barriers slow the rate of adoption beyond trading, DeFi, or intra-crypto uses.

These growth estimates mean that unless new use cases or regulatory clarity unlock broader adoption, growth may be incremental rather than explosive.

5. Risks & Challenges

- Regulatory cost & compliance risk: New rules mean issuers must maintain high-quality reserve assets, strong audit trails, reporting, possibly even banking licenses or partnerships, which raise barrier to entry and ongoing operational costs.

- Fragmented liquidity: As more stablecoins compete, liquidity (users, capital, integrations) may be spread thin. Smaller coins may struggle to maintain pegging, trust, or market depth.

- Margin pressure: As competition intensifies, issuers may need to invest more in trust-building (reserves, compliance, transparency), technology, and partnership to differentiate, squeezing profit margins.

- Reliance on crypto market growth: If the broader cryptocurrency market slows or shrinks, stablecoins may suffer collateral damage. Most stablecoin demand today is still tied to crypto-native use cases (trading, DeFi).

6. Opportunities & Strategic Responses

- Institutional adoption & financial infrastructure: Stablecoins that satisfy regulatory and auditing standards may attract institutional clients (banks, asset managers, cross-border payments). Also, stablecoins may be used in settlement, tokenization of real-world assets, programmable finance.

- Regulation as differentiator: Issuers that proactively meet or exceed regulatory expectations (e.g. fully backed reserves, transparency, reliable audit) can use that as a competitive edge.

- Infrastructure innovation: Dedicated blockchains (like Arc for USDC), faster compliance, interoperability between blockchains, integration with existing financial rails can improve utility.

- Global & cross-jurisdictional stablecoins: There may be room for stablecoins that serve international payments, cross-border remittances, or regulatory-friendly jurisdictions which lower friction.

Recent Trends & Updates (beyond the JP Morgan report)

- Amundi & concerns about global payments/monetary sovereignty: The asset manager Amundi has warned that the GENIUS Act could lead to global “dollarization,” displacement of domestic monetary control in some countries, and other systemic risks.

- Treasury market impact: Because many stablecoins must hold reserves in short-term U.S. Treasury bills, rising stablecoin supply could materially increase demand for Treasurys, affecting yields and bond market dynamics. For example, Tether holds tens of billions in T-bills.

- EU stablecoins & regulatory environment: Europe’s Markets in Crypto-Assets Regulation (MiCA) is now fully in force for certain stablecoin classes, adding pressure globally for stablecoin issuers to adhere to similar standards.

- Emerging tokenization & real-world asset (RWA) use cases: Academic and industry research is focusing on how stablecoins can serve as programmable money, for example in tokenizing real-world assets, as a medium of settlement, or in hybrid systems combining public fiat / central bank money with private stablecoins.

What This Means for Practitioners / Investors

If you are looking for new crypto assets, or seeking stablecoins as a revenue source, or considering blockchain applications in real-world business, here are implications:

- Due diligence is more essential than ever: Don’t just look at price or yield; examine reserve backing, audit practices, regulatory compliance, issuer credibility.

- Focus on stablecoins with institutional trust: If a coin is positioning itself to serve institutional clients (banks, settlement, large scale payments), it may offer more durability in a competitive environment.

- Diversify among stablecoins: Since market share shifts may cause losses for some, holding exposure to multiple stablecoins may mitigate risk (regulation risk, pegging risk, issuer risk).

- Watch regulation carefully: Laws like the GENIUS Act in the U.S., MiCA in EU, and others in Asia will shape which coins survive, which thrive. Being early in compliance can be an advantage.

- Seek utility beyond DeFi/trading: Use cases in payments, remittances, programmable finance, tokenization, cross-border settlements may drive the next wave of growth. Projects or coins enabling real business usage may outperform those purely speculative.

Conclusion

The U.S. stablecoin market is entering a pivotal moment. JP Morgan’s forecast of a zero-sum future cautions that unless the overall cryptocurrency market expands significantly, new entrants and existing players will mostly compete over fixed demand, slicing existing market share rather than creating large new demand. Regulatory change—especially via the GENIUS Act—is pushing higher standards, raising costs, but also raising trust. This creates both risk and opportunity: risk for smaller or non-complying issuers, and opportunity for those who build credibility, institutional linkages, infrastructural advantages, and useful use-cases.

For those hunting new crypto assets or revenue sources, the wise strategy is one that emphasizes regulatory alignment, functional utility, diversification, and partnering with emerging finance or real-world asset projects. The market may not explode to multiple trillions overnight as some earlier projections hoped, but there is still strong potential for stablecoins to play a central role in crypto’s integration with traditional finance—and for certain players to win much of the share of that future pie.