Key Points :

- Stablecoins are entering a phase of mass enterprise adoption, described as a “ChatGPT moment” by Brad Garlinghouse

- Fortune 500 and Fortune 2000 executives are actively exploring stablecoin strategies

- The global stablecoin market could reach $56.6 trillion annually by 2030

- Ripple is positioning itself aggressively with RLUSD and strategic acquisitions

- Regulatory clarity (e.g., US legislation) is a key catalyst for adoption

- Stablecoins are evolving from crypto tools into core financial infrastructure

1. The “ChatGPT Moment” of Finance

The analogy is deliberate and powerful. Just as generative AI exploded into mainstream consciousness with ChatGPT, stablecoins are now reaching a similar inflection point within finance.

According to Brad Garlinghouse, corporate leaders are no longer asking whether crypto has value, but rather how to implement it. This shift is subtle but critical. It signals a transition from speculative curiosity to operational necessity.

Boardrooms across major corporations—particularly within the Fortune 500 and Fortune 2000—are increasingly directing CFOs and treasury teams to evaluate stablecoins as part of their financial strategy. This is not driven by ideology or innovation hype, but by clear business advantages:

- Faster settlement times

- Lower cross-border transaction costs

- Reduced reliance on correspondent banking networks

- Improved liquidity management

Stablecoins, in this sense, represent not just a new asset class but a new financial primitive—a programmable, borderless unit of account that integrates seamlessly into digital systems.

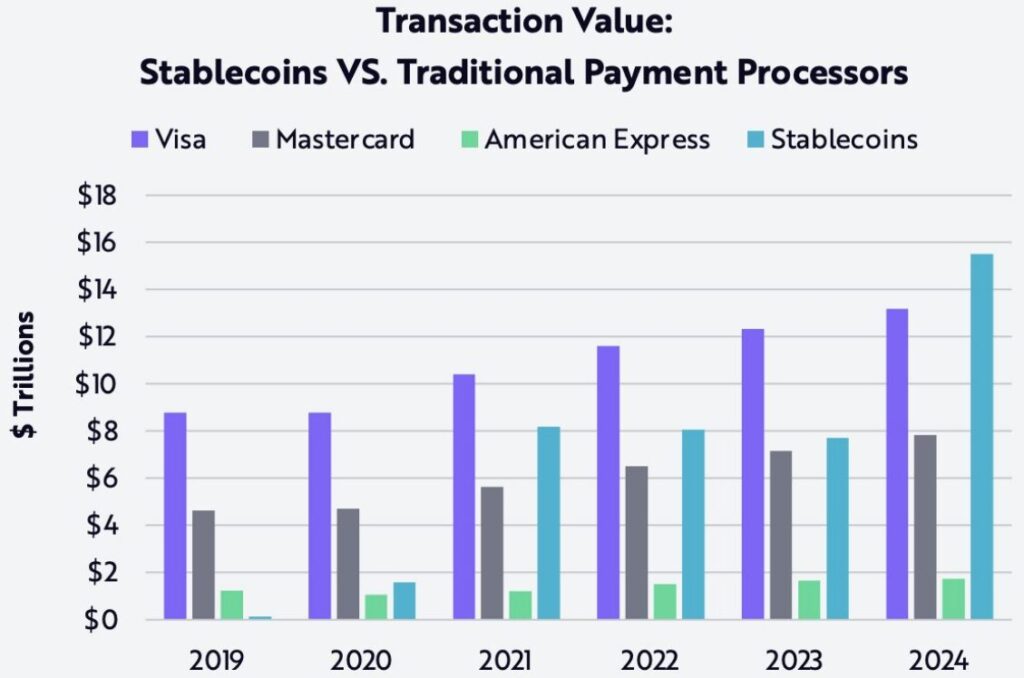

2. Market Explosion: From Billions to Trillions

The scale of the opportunity is staggering.

Bloomberg Intelligence estimates that stablecoin transaction flows could grow at an annual rate of 80%, reaching approximately $56.6 trillion by 2030. To put this into perspective, that would rival or exceed the transaction volumes of major global payment networks today.

Even today, the market is already massive. Annual stablecoin transaction volume has surpassed $33 trillion, with approximately 90% dominated by two players:

- Tether (USDT)

- USD Coin (USDC)

This dominance highlights both the maturity and concentration of the current ecosystem. However, it also opens the door for new entrants—particularly those targeting institutional use cases.

3. Ripple’s Strategic Positioning

Ripple is not approaching this trend passively—it is aggressively positioning itself as a foundational player in the next generation of financial infrastructure.

The launch of RLUSD, Ripple’s proprietary stablecoin introduced in December 2024, marks a significant milestone. With a market capitalization of approximately $1.4 billion, RLUSD has already become one of the top 10 stablecoins globally.

But the strategy goes far beyond issuing a stablecoin.

Ripple has executed two major acquisitions:

- Hidden Road (Prime brokerage platform): ~$1.25 billion

- GTreasury (Corporate treasury platform): ~$1.0 billion

These acquisitions signal a clear intent: to build an end-to-end institutional financial stack that integrates:

- Liquidity provisioning

- Treasury management

- Cross-border settlement

- Digital asset custody

In other words, Ripple is not just competing in crypto—it is attempting to redefine the infrastructure of global finance.

4. Why Enterprises Are Paying Attention

For enterprises, the appeal of stablecoins is not theoretical—it is operational.

4.1 Cross-Border Payments Efficiency

Traditional remittance and settlement systems rely heavily on intermediaries, leading to:

- Settlement delays (1–3 days or longer)

- High fees (often 3–7% in emerging markets)

- Limited transparency

Stablecoins can reduce settlement times to minutes or seconds, with significantly lower fees.

4.2 Treasury Optimization

Corporate treasury departments are increasingly exploring stablecoins for:

- Real-time liquidity management

- Automated reconciliation

- Multi-currency operations without FX friction

4.3 Programmability

Unlike traditional fiat, stablecoins can be embedded into smart contracts, enabling:

- Automated payments

- Conditional settlements

- Integrated compliance mechanisms

This programmability is particularly relevant for EMI and VASP operators, where compliance, auditability, and automation are critical.

5. Regulation as the Catalyst

Despite strong momentum, regulatory uncertainty remains the primary bottleneck.

Garlinghouse emphasized the importance of US legislation, particularly efforts such as the CLARITY Act, in accelerating adoption.

Key regulatory factors include:

- Clear classification of digital assets

- Licensing requirements for stablecoin issuers

- AML/CFT compliance frameworks

- Consumer protection mechanisms

For institutions, regulatory clarity is not a constraint—it is an enabler. It provides the confidence needed to deploy capital and integrate new technologies into core operations.

6. The Transition: From Crypto to Financial Infrastructure

The most important shift is conceptual.

Stablecoins are no longer merely “crypto assets.” They are becoming infrastructure.

This transition mirrors earlier technological shifts:

- The internet evolved from academic networks to global commerce infrastructure

- Cloud computing moved from optional tools to mission-critical systems

- AI transitioned from research to enterprise productivity

Stablecoins are following the same trajectory.

7. Implications for EMI, VASP, and Remittance Businesses

For organizations operating in regulated financial environments—such as EMI, VASP, and remittance providers—the implications are immediate and strategic.

7.1 Competitive Differentiation

Early adoption of stablecoin rails can:

- Reduce costs

- Improve user experience

- Enable new revenue models

7.2 Compliance Integration

Stablecoins can be integrated with:

- Travel Rule systems

- Real-time monitoring

- Automated AML checks

7.3 New Revenue Streams

Potential opportunities include:

- FX spreads via stablecoin corridors

- Treasury yield strategies

- API-based payment services

For a company like WIBS PHP INC, this aligns directly with the hybrid EMI + VASP model—bridging traditional finance with blockchain-based settlement.

8. Risks and Challenges

Despite the optimism, several risks remain:

- Regulatory fragmentation across jurisdictions

- Counterparty risks (issuer solvency)

- Liquidity concentration in major stablecoins

- Technology integration complexity

Enterprises must approach adoption strategically, balancing innovation with compliance and risk management.

Conclusion: The Beginning of a New Financial Era

Stablecoins are no longer an experiment—they are becoming a cornerstone of modern finance.

The “ChatGPT moment” described by Brad Garlinghouse reflects a broader transformation: a shift from curiosity to necessity, from niche to mainstream.

As regulatory frameworks mature and infrastructure continues to evolve, stablecoins are poised to redefine:

- How money moves

- How businesses operate

- How financial systems are structured

For forward-looking organizations, the question is no longer if stablecoins will matter—but how quickly they can be integrated into the core of their operations.