Main Points :

- Yield-bearing stablecoins are becoming a central topic in U.S. financial policy debates.

- Some banks fear stablecoins will drain deposits, while crypto advocates argue the opposite.

- The White House digital asset advisory council suggests stablecoins may increase global demand for U.S. dollars.

- Regulatory proposals such as the GENIUS Act and CLARITY Act are shaping how stablecoins will interact with the banking system.

- For crypto investors and builders, stablecoin yield mechanisms could become a major revenue opportunity and infrastructure layer for global finance.

1. The Rising Debate Around Stablecoin Yields

The global cryptocurrency market has entered a new phase in which stablecoins are no longer seen merely as trading instruments. Instead, they are increasingly viewed as the infrastructure of the next digital financial system. A recent debate in Washington illustrates how central these digital dollars have become.

Patrick Witt, Executive Director of the White House’s Digital Asset Advisory Council, recently argued that yield-bearing stablecoins may actually increase capital flows into the U.S. banking system, rather than drain them. His comments came amid ongoing discussions about U.S. legislation that aims to establish a clearer regulatory framework for cryptocurrencies and stablecoins.

The debate reflects a larger structural question: Will stablecoins disrupt banks, or will they ultimately reinforce the U.S. financial system?

This question is particularly important because stablecoins have already become one of the most widely used crypto instruments in the world. Their combined market capitalization has grown rapidly in recent years, and they play a central role in global trading, remittances, decentralized finance (DeFi), and increasingly real-world payments.

For investors searching for the next wave of blockchain applications and yield opportunities, the outcome of this debate could reshape the financial landscape.

2. The White House Perspective: Stablecoins Can Attract Global Capital

Patrick Witt’s central argument is straightforward: the world’s demand for U.S. dollars remains enormous.

According to his statements on X (formerly Twitter), international investors may convert their local currencies into stablecoins issued by U.S. companies. Because most regulated stablecoins are backed by reserves such as U.S. dollars and U.S. Treasury securities, the funds ultimately flow into the American financial system.

In practice, the process works like this:

- A user in another country buys a U.S. dollar stablecoin.

- The stablecoin issuer receives the fiat currency equivalent.

- The issuer deposits the funds in banks or purchases U.S. Treasuries.

- The capital ultimately strengthens U.S. financial markets.

In other words, stablecoins may function as global digital demand channels for U.S. dollar assets.

This mechanism mirrors how the eurodollar market historically expanded the global reach of the dollar. However, stablecoins do so through blockchain infrastructure rather than traditional banking networks.

3. The Bankers’ Concern: Deposits Could Leave the Banking System

Despite this optimistic view from the White House, many banks remain cautious.

A recent research note from Standard Chartered estimated that the expansion of stablecoins could potentially reduce U.S. bank deposits by an amount equivalent to one-third of the stablecoin market capitalization.

The concern is based on a simple behavioral assumption.

If users can earn yield directly from stablecoins—particularly through tokenized treasury products or DeFi lending—they may prefer to hold their savings in digital dollars instead of traditional bank accounts.

For example, if a stablecoin platform offers a yield of $4–$5 per $100 annually, while a traditional savings account offers significantly less, capital could migrate toward blockchain-based alternatives.

This dynamic has already appeared in decentralized finance ecosystems, where stablecoins such as USDC and USDT have been widely used in lending platforms and liquidity pools.

Banks worry that this trend could gradually reduce the deposit base that supports their lending activities.

4. The Role of New U.S. Legislation: GENIUS and CLARITY Acts

The policy debate around stablecoins is unfolding alongside major regulatory proposals in the United States.

Two legislative initiatives are particularly important:

GENIUS Act

The proposed GENIUS Act focuses on creating a regulatory framework for stablecoin issuance and reserve requirements. It aims to ensure that stablecoins are fully backed by high-quality assets such as cash or U.S. Treasuries.

If implemented, the law could effectively integrate stablecoin issuers into the regulated financial system.

CLARITY Act

The CLARITY Act seeks to define regulatory responsibilities between agencies such as the SEC and the CFTC, while also addressing the treatment of digital assets including stablecoins.

Supporters argue that these frameworks will reduce regulatory uncertainty and accelerate institutional adoption.

Critics, however, fear that allowing stablecoins to provide yield could create competition with traditional banking products.

5. Regional Banks Push Back

Opposition to yield-bearing stablecoins has been particularly strong among regional banks.

Christopher Williston, president of the Independent Bankers Association of Texas, warned that concessions in the CLARITY Act negotiations could undermine community lending and local economic activity.

He argued that liquidity leaving regional banks could weaken the financial foundation that supports small businesses and local development.

From the perspective of community banks, deposits are not just funding sources—they are also the basis for loans that support regional economies.

If a significant share of deposits migrates into digital assets, the traditional lending ecosystem could face disruption.

6. Crypto Industry Response: Cooperation Is Possible

The cryptocurrency industry has responded to these concerns by suggesting that banks and blockchain companies should collaborate rather than compete.

Austin Campbell, founder of Zero Knowledge Consulting, argued that if regional banks and the crypto sector fail to cooperate, large global banks will ultimately dominate both markets.

In this scenario, major financial institutions could leverage their resources to control stablecoin infrastructure, leaving smaller players behind.

This argument reflects a broader trend: many large banks are already experimenting with tokenized deposits, blockchain settlement systems, and stablecoin-like instruments.

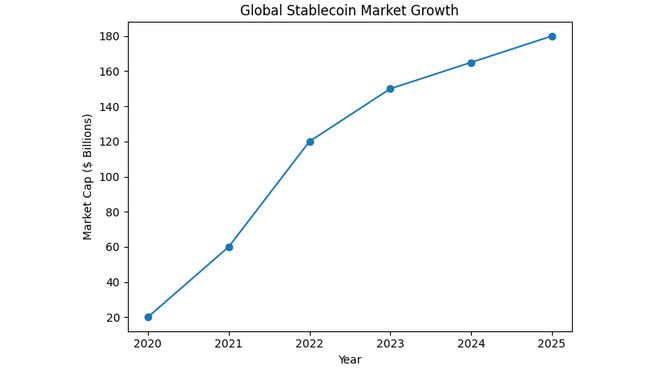

7. Global Stablecoin Growth and Market Trends

The policy debate in the United States is occurring at a time when stablecoin adoption is accelerating worldwide.

Several trends illustrate this growth:

Rapid Expansion of Market Capitalization

The total stablecoin market has grown dramatically over the past few years, surpassing $150 billion at times. This expansion reflects increasing demand for blockchain-based dollars in global markets.

Integration With Traditional Finance

Financial institutions are beginning to explore stablecoins as tools for payments, settlement, and liquidity management.

Some banks are experimenting with tokenized deposits, which function similarly to stablecoins but remain within regulated banking frameworks.

DeFi Yield Opportunities

Stablecoins have become one of the primary sources of yield generation in decentralized finance.

Users can lend stablecoins, provide liquidity, or participate in automated market makers to earn returns.

These opportunities have attracted both retail investors and institutional participants.

Global Stablecoin Market Growth

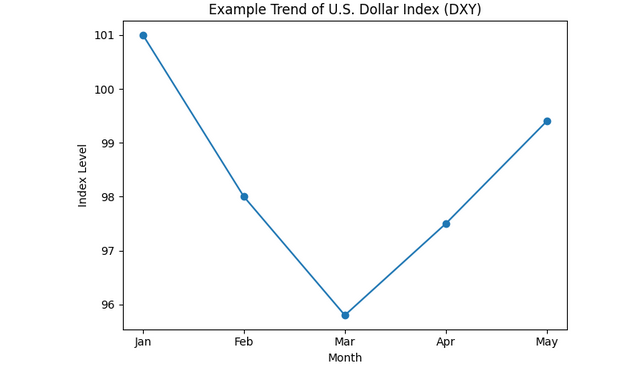

8. The U.S. Dollar’s Role in the Digital Economy

The debate around stablecoins also reflects broader geopolitical dynamics.

Despite periodic fluctuations, the U.S. dollar remains the dominant global reserve currency.

The U.S. Dollar Index (DXY) recently reached a multi-year low before rebounding, highlighting ongoing volatility in currency markets.

Stablecoins may reinforce the dollar’s global role by allowing people in emerging markets to hold digital dollars without requiring access to U.S. banks.

For individuals in countries experiencing inflation or capital controls, stablecoins can function as a digital safe haven.

Dollar Index (DXY) Trend Example

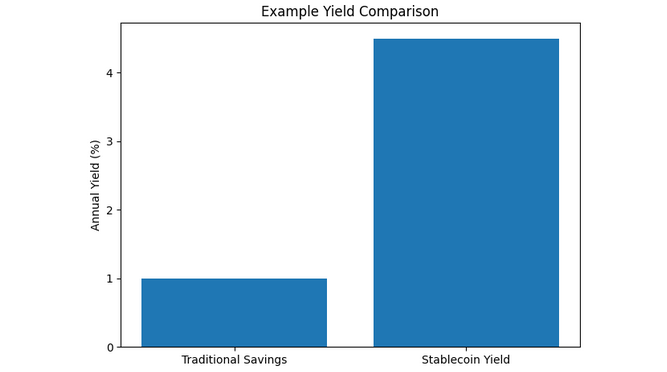

9. Stablecoin Yield as a New Financial Layer

Yield-bearing stablecoins represent one of the most interesting developments in the crypto ecosystem.

Rather than simply holding a token pegged to $1, users can earn returns generated from:

- Treasury-backed reserves

- DeFi lending markets

- Tokenized real-world assets

- Liquidity provisioning

This structure effectively creates blockchain-native money market funds.

For investors seeking new income streams, stablecoin yield strategies could become an important component of digital asset portfolios.

Stablecoin Yield vs Traditional Savings

10. Implications for Crypto Investors and Builders

For readers searching for new crypto assets and revenue opportunities, the stablecoin sector offers several key insights.

First, infrastructure projects supporting stablecoin issuance, settlement, and compliance may experience strong demand as regulation becomes clearer.

Second, decentralized finance platforms that generate sustainable stablecoin yields could attract both retail and institutional capital.

Third, the intersection between stablecoins and traditional finance may create hybrid systems where banks, fintech companies, and blockchain protocols operate together.

These developments suggest that stablecoins may become the financial rails of the digital economy.

Conclusion

The debate over stablecoin yields highlights a fundamental transformation taking place in global finance.

While some banks fear that digital dollars could drain deposits, policymakers such as Patrick Witt argue that stablecoins may actually strengthen the U.S. financial system by expanding global demand for dollar-denominated assets.

At the same time, regulatory frameworks like the GENIUS Act and CLARITY Act will determine how these digital instruments interact with traditional banking.

For investors and entrepreneurs in the crypto sector, the message is clear: stablecoins are no longer just trading tools—they are emerging as the backbone of the next generation of financial infrastructure.

As the regulatory environment evolves and institutional participation increases, the stablecoin ecosystem could become one of the most important drivers of growth in the blockchain economy.