Key Points :

- The Council of Economic Advisers (CEA) challenges claims of massive bank deposit outflows from stablecoins

- Banking groups warned of up to $1.3 trillion in deposit migration and $850 billion in reduced lending

- CEA analysis shows yield bans would increase lending by only $2.1 billion (≈0.02%)

- Consumers would bear approximately $800 million in additional costs if yields are prohibited

- Around 88% of stablecoin reserves already remain within the traditional financial system

- Legislative uncertainty around the Clarity Act continues amid political and industry conflict

1. Introduction: A Narrative of Fear Meets Data

The debate over stablecoins has entered a critical phase in 2026, as policymakers, banks, and crypto innovators collide over one central question: Do stablecoins threaten the traditional banking system, or do they quietly reinforce it?

For months, major banking institutions and lobbying groups have warned of a looming crisis. Their argument is simple yet alarming: if stablecoins begin offering yield to users, deposits will rapidly leave the banking system, triggering a contraction in lending and potentially destabilizing financial markets.

However, a recent report from the Council of Economic Advisers has fundamentally challenged this narrative. Rather than relying on speculative projections, the CEA applied quantitative modeling to assess the real impact—and the results are striking.

The data suggests that the “deposit outflow crisis” may be largely overstated.

2. The Banking Industry’s Warning: A Trillion-Dollar Risk

The banking sector’s position has been consistent and forceful. Organizations such as the Independent Community Bankers of America (ICBA) have argued that allowing stablecoins to offer yield would create a powerful incentive for consumers to shift funds out of traditional bank deposits.

Their projections estimate:

- Up to $1.3 trillion in deposit outflows

- A corresponding $850 billion contraction in lending capacity

From a traditional finance perspective, this concern is understandable. Banks rely heavily on deposits as a primary funding source for loans. Any significant migration of funds could, in theory, reduce credit availability across the economy.

Yet these projections are based on a key assumption: that funds leaving banks for stablecoins exit the financial system entirely.

This assumption, as the CEA analysis reveals, is fundamentally flawed.

3. The CEA Model: A Minimal Impact on Lending

Comparison of Estimated Impact on Bank Lending (Bank Industry vs CEA Model)

The CEA’s model offers a more nuanced understanding of how stablecoins interact with the broader financial system.

Even in a scenario where stablecoin yields are fully banned, the increase in bank lending is estimated at just:

- $2.1 billion (approximately 0.02%)

This figure is negligible when compared to the scale of the U.S. financial system. In other words, prohibiting stablecoin yields would barely move the needle in terms of protecting bank lending.

At the same time, the policy would impose approximately $800 million in additional costs on consumers, effectively reducing financial efficiency and innovation.

This creates a striking asymmetry:

- Minimal benefit to banks

- Significant cost to users

For policymakers, this raises an important question: Is the trade-off justified?

4. The Hidden Mechanism: Why Funds Don’t Truly “Leave”

The most important insight from the CEA report lies in understanding where stablecoin funds actually go.

Contrary to popular belief, when users convert bank deposits into stablecoins, the money does not disappear into a parallel system. Instead, it is largely recycled back into the traditional financial infrastructure.

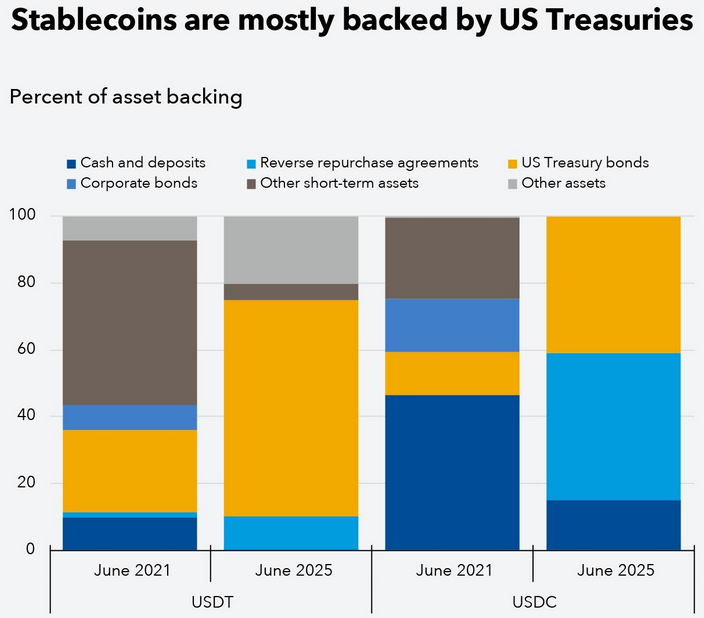

The report highlights that approximately:

- 88% of stablecoin reserves are held in U.S. Treasuries or bank deposits

This creates a circular flow:

- Users convert fiat into stablecoins

- Issuers allocate reserves into Treasuries and banks

- Funds remain within the financial system

This mechanism effectively neutralizes the feared “deposit drain.” Rather than competing with banks, stablecoins operate as a new interface layer on top of existing financial rails.

5. Legislative Battlefield: The Clarity Act and Political Gridlock

The implications of the CEA findings extend far beyond economics—they strike at the heart of U.S. crypto regulation.

The Clarity Act has become the focal point of this debate. One of its most contentious provisions is whether stablecoin issuers should be allowed to offer yield.

Key developments include:

- Strong opposition from crypto firms such as Coinbase

- Delays in Senate Banking Committee deliberations

- Proposed compromises limiting yield to specific reward programs

Despite these efforts, consensus remains elusive. Prediction markets such as Polymarket now estimate the probability of the bill passing in 2026 at around 60%, down sharply from over 90% earlier in the year.

With the U.S. midterm election cycle accelerating toward August 2026, the legislative window is rapidly closing.

6. Market Implications: A New Era of Yield Competition

Stablecoin Growth vs Traditional Deposits (Conceptual Trend Visualization)

For investors and builders, the implications are profound.

If stablecoin yields are permitted—even in a limited form—they could unlock:

- Programmable interest mechanisms

- DeFi-integrated savings products

- Cross-border yield optimization strategies

This would mark a shift from passive asset holding to active yield participation within blockchain ecosystems.

At the same time, traditional banks may be forced to respond by:

- Increasing deposit rates

- Launching tokenized deposit products

- Integrating blockchain-based settlement layers

The result is not displacement, but convergence.

7. Strategic Insight: Where Opportunity Emerges

For readers seeking new crypto assets, income streams, and practical blockchain applications, this transition phase presents several opportunities:

1. Yield Infrastructure Tokens

Protocols that facilitate stablecoin yield distribution—particularly those bridging CeFi and DeFi—stand to benefit significantly.

2. Tokenized Treasury Platforms

Given that stablecoin reserves are heavily invested in government bonds, platforms enabling direct access to tokenized Treasuries could see rapid growth.

3. Payment and Remittance Networks

Stablecoins continue to dominate cross-border payments, offering faster and cheaper alternatives to traditional systems.

4. Compliance-First Crypto Projects

As regulation tightens, projects that align with frameworks like the Clarity Act will gain institutional trust and adoption.

8. Conclusion: From Conflict to Integration

The stablecoin yield debate is no longer just a regulatory issue—it is a defining moment in the evolution of global finance.

The data from the Council of Economic Advisers forces a reconsideration of long-held assumptions. Rather than draining the banking system, stablecoins appear to recycle liquidity and enhance financial efficiency.

At the same time, political uncertainty remains high. The fate of the Clarity Act will shape the next phase of market development, determining whether innovation accelerates or stalls.

For investors, builders, and institutions, one conclusion is clear:

The future is not a battle between banks and blockchain—it is a convergence of both.