Main Points :

- Bitcoin (BTC) spot markets show predominant selling pressure despite gold and equities rallying.

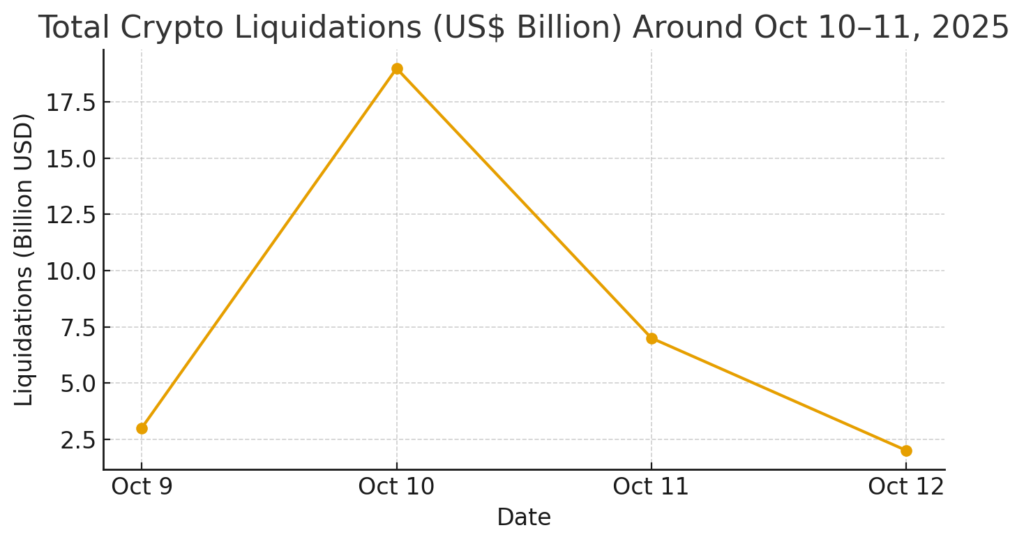

- A major liquidity shock on October 10-11 triggered the largest crypto liquidation in history (> US$19 billion).

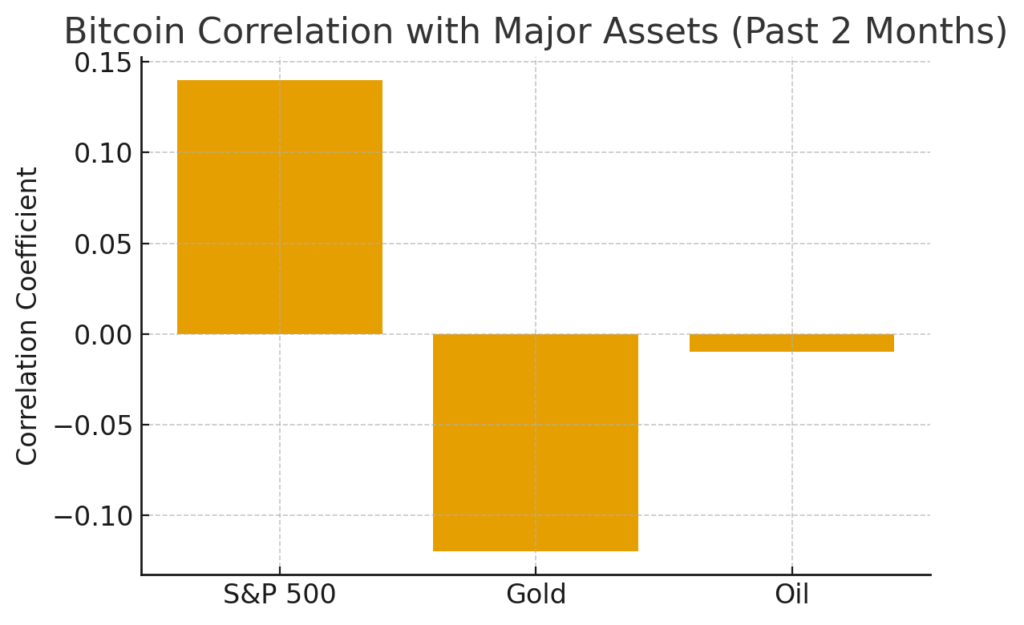

- BTC’s correlations with S&P 500 and gold are low, indicating independence from traditional risk assets.

- Structural vulnerabilities in crypto infrastructure (leverage, thin order books, centralised exchanges) were exposed.

- For blockchain practitioners and new-asset hunters: this period may offer both risk and opportunity in accumulation, infrastructure building, and altcoin evaluation.

Spot Market Selling Pressure within Broad Risk-On Environment

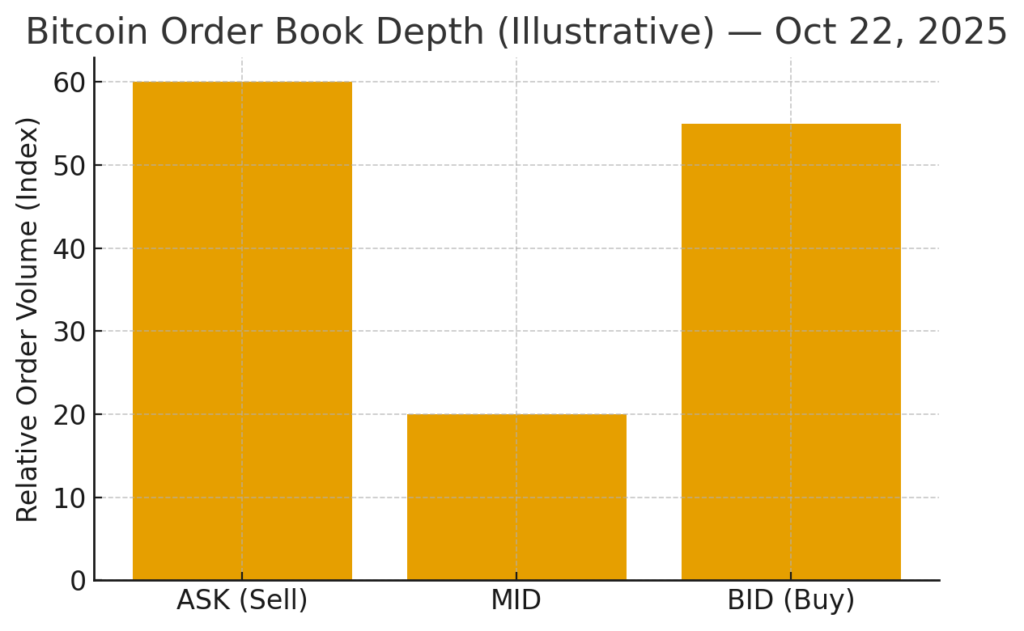

The recent market context shows that although gold and global equities are pushing higher, Bitcoin has remained relatively static. According to Japanese crypto analyst “仮想NISHI”, at the time of his report (10 AM on October 22, Tokyo), Bitcoin was “横ばい” (flat) while the Nikkei approached 50,000 yen and gold hovered near all-time highs. The key observation: large sell orders dominate the order book on the ask (sell) side, while thick bids sit around the US $100 000 region, indicating latent support but also the potential for sharp moves either direction.

On the spot side, the prevalence of sell orders — especially in physical/spot markets, rather than just derivatives — is underscored as one of the principal causes of the recent draw-down. The fact that major assets (gold, stocks) are advancing while BTC lags suggests that capital is behaving differently in crypto than in traditional safe-haven or growth assets in this cycle.

For an investor looking for new crypto revenue sources or building on blockchain, this indicates a possible strategic pause in the “digital gold” narrative for Bitcoin, and opens questions about whether altcoins or blockchain infrastructure projects may offer differentiated opportunities.

October 10-11, 2025: Historic Liquidation Shock and Market Microstructure Test

On October 10–11, a dramatic event unfolded: the crypto markets underwent an unprecedented liquidation cascade. Data suggest over US$19 billion of leveraged positions were forcibly closed within ~24 hours, making it arguably the largest single-day liquidation ever in this asset class.

More specific data:

- Spot BTC plunged from around US$122 000 to lows circa US$104 700 in the 10–11 Oct window.

- Perpetual futures open interest fell ~43% (from roughly US$217 billion to US$123 billion) across major exchanges.

- Some altcoins and smaller tokens collapsed by 60–90% in minutes, revealing acute structural fragility.

The immediate trigger appears to have been a geopolitical shock: an announcement from Donald Trump threatening 100 % tariffs on Chinese imports (and related export controls) ignited a risk-off reflex across markets, including crypto.

However, deeper analyses point to internal “micro-structure” weakness: highly leveraged long positions, thin order books, concentrated liquidity among a few exchanges and market-makers, and perhaps even manipulative behaviour (e.g., oracle/peg-crack events).

From the perspective of blockchain infrastructure builders, this event offers a set of red flags: reliance on centralised exchanges, vulnerability of synthetic-peg tokens and borrowed collateral, and a fragile plumbing structure even for large-cap assets. Any project or protocol that seeks to be durable must factor in these systemic risks.

Bitcoin’s Independence: Low Correlation with Stocks, Gold and Commodities

The report by NISHI draws an interesting correlation matrix: over the past two months, BTC had correlation +0.14 with the S&P 500, –0.12 with gold, and –0.01 with oil. In short, Bitcoin has been moving almost independently of these major asset-classes.

For investors hunting new revenue sources in crypto, this is a double-edged sword: on the one hand, the lack of strong coupling to equities and commodities may make Bitcoin (and crypto) a potential diversification play; on the other hand, the absence of correlation also means crypto can decouple negatively and behave idiosyncratically (i.e., risk is not cushioned by traditional safe-asset flows).

Given this independence, selection of blockchain projects or crypto assets cannot assume they will ride macro-trends universally — each token and protocol may experience its own micro-cycle, independent of equity/commodity sentiment.

Technical & Structural Analysis: Boards, Order-Books and Future Risk

On the technical side, the report highlights: the order books show heavy sell walls above current prices (ASK side), and strong bid walls around US$100 000. The adage “the board flows to the thick side” (板は厚い方に流れる) suggests that price movement may test these thick areas soon — either breaking higher through resistance or being repelled downward.

Furthermore, low yields on US Treasury bonds are reducing the interest-arbitrage benefit of issuing stablecoins. As the yield incentive declines, the issuance of stablecoins slows, and that may sub-optimally reduce liquidity inflows into crypto.

Together, this suggests: (a) potential for heightened volatility if one of the thick walls is breached; (b) structural headwinds due to declining yield arbitrage; (c) the maturity of the crypto market is still incomplete — especially in infrastructure, liquidity-depth and resilience.

For blockchain practitioners, one takeaway is to design for liquidity stress. Protocols and markets should assume that during shocks, order-book depth may vanish, or exchange APIs may malfunction — on-chain and off-chain resilience matters.

Recent Trends & What This Means for Crypto Revenue Builders

Beyond the referenced article, recent commentary and data shed further light:

- Analysts suggest that this October event may act as a “leverage reset” — clearing overextended positions and potentially setting the stage for future accumulation.

- Exchange-Traded Funds (ETFs) tracking Bitcoin have seen outflows (approximately US$1.2 billion) during this period, which points to institutional caution or temporary flight from the space.

- OTC (over-the-counter) desks are playing a critical role as “shock absorbers” in the ecosystem — when spot exchanges struggle, large trades and redemptions are shifting to OTC rooms.

- Some tokens and derivatives still show signs of structural vulnerability (e.g., synthetic dollar de-pegs, token wrap discounts) even though Bitcoin itself held up relatively well.

For someone seeking a new crypto asset or next revenue source, what are the implications?

- Accumulation mindset: The reset may offer an entry window, especially if one expects a medium-term bullish cycle post-2025. But risk must be managed.

- Protocol selection: Focus on projects with strong governance, liquidity structure, decentralisation of access (not over-reliant on one exchange), and that solve real use-cases rather than purely speculative token models.

- Infrastructure bets: Given the revealed fragility of exchange rails and synthetic-token systems, infrastructure solutions (e.g., better decentralized order books, cross-chain settlement, oracle resilience) may offer differentiated opportunity.

- Risk-aware leverage: The crash shows how quickly leverage can turn from friend to foe. If you plan to deploy capital (in yield farming, staking, derivatives), structural shock scenarios must be modelled.

- Alternative income streams: Consider blockchain-based business models that are less dependent on spot price appreciation — e.g., token-economy services, data infrastructure, layer-2 protocols, cross-chain bridging — while maintaining awareness that liquidity events can cascade.

Summary

In summary, the recent period has revealed a complex picture: although Bitcoin remains a major flagship of the crypto ecosystem, it is currently under spot market selling pressure, even as other risk and safe assets rally. The historic liquidity shock of October 10–11 exposed deep structural vulnerabilities — from concentrated centralised exchange risk to thin order books and leverage cascades — forcing a reset across the derivative and spot landscape.

For blockchain practitioners and investors seeking new assets or revenue streams, this juncture offers both caution and seedbed. The independence of crypto from traditional assets means opportunity for diversification, but also demands that each project be evaluated on its internal merits (governance, liquidity resilience, network utility). Infrastructure plays, real-use-case protocols and less-leveraged participation models are likely to stand out.

At this moment, with Bitcoin’s correlations weak and its order-book showing latent walls, market dynamics remain on a knife-edge — if either the upper thick bid or the lower heavy ask gives way, volatility may spike quickly. For those actively building or selecting new crypto assets, the lesson is clear: prepare for structural shocks, avoid over-reliance on price narratives alone, and favour projects engineered for resilience in a microstructure-challenged ecosystem.