Main Points :

- Current cross-border payments suffer from high fees, long settlement times (2–36 hours), and lack of transparency.

- Digital currency technologies—such as CBDCs, stablecoins, and tokenized deposits—offer efficient, low-cost, transparent alternatives.

- VISA, the Bank of Japan, and Ant International presented complementary, innovation-focused solutions rather than disruptive replacements.

- Pilot programs and collaborations are already underway—VISA’s stablecoin pilot for Visa Direct, BoJ’s participation in Project Agora, and Ant’s financial inclusion work in Bangladesh.

- Final vision: a real-time, interoperable global payments ecosystem where remittance is frictionless and simple.

- Broader context: SBI’s strategic push in Japan for stablecoins and tokenized real-world assets indicates growing momentum in regulated digital finance.

1. Facing the Pain Points in Cross-Border Payments

At the WebX Fintech EXPO powered by SBI Group held in Osaka on August 22, 2025, leading voices from VISA, the Bank of Japan, and Ant International discussed the persistent challenges hampering cross-border payments. They highlighted three main issues: high transaction fees, settlement delays of 2 to 36 hours, and insufficient transparency in payment status.

2. Digital Currency Approaches: CBDCs, Stablecoins, and Tokenized Deposits

Panelists presented digital currency technologies as realistic, complementary solutions—not disruptive threats—to the existing financial infrastructure. Technologies such as central bank digital currencies (CBDCs), stablecoins, and tokenized deposits offer the potential for 24/7 real-time settlement on blockchain, with dramatically reduced costs and increased visibility.

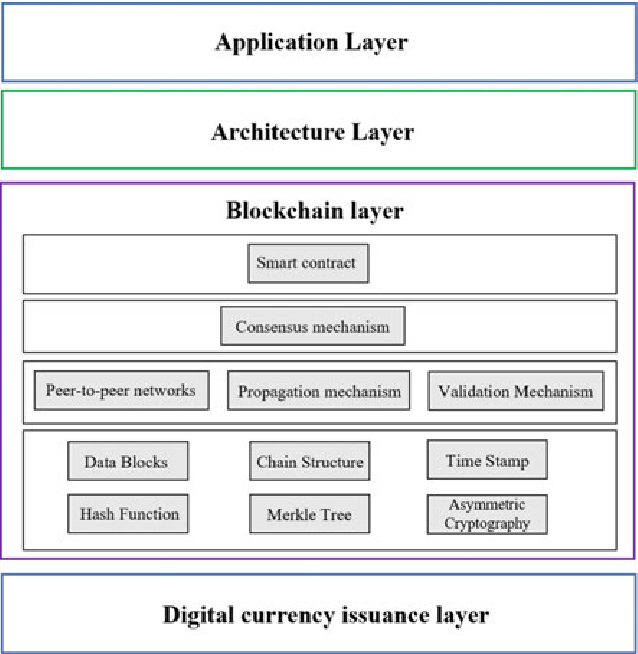

Graphic Insertion (Here):

A clear architecture diagram showing how blockchain-based digital currencies improve cross-border settlements (e.g., as represented in the image above). Mocht this be useful to illustrate the four-layered model—application, architecture, blockchain, and digital issuance—it strengthens the explanation.

3. VISA’s Pilot of Stablecoin Integration

VISA’s Head of Digital Currencies for Asia Pacific, Nischint Sanghavi, revealed that the company is piloting stablecoin payments and exploring integration with Visa Direct for global remittance solutions. He emphasized that these innovations are meant to complement, not replace, traditional systems.

4. Bank of Japan’s Project Agora and Wholesale CBDC Exploration

Masaki Bessho, Director of the Bank of Japan’s Kobe branch, shared that the bank joined the BIS’s “Project Agora,” collaborating with seven central banks and around 40 private-sector banks to explore blockchain use. A wholesale CBDC is seen as a promising instrument for improving cross-border transfers.

5. Ant International’s Financial Inclusion via bKash and AI Scoring

Yinfan Zhang from Ant International described a real-world use case in Bangladesh, where Ant partnered with the e-wallet provider bKash. Using AI-driven alternative data scoring, they enabled 30% of active users to access financial services while maintaining low default rates. This demonstrates how digital payments platforms, when combined with AI, can foster financial inclusion.

6. The Vision: Real-Time, Interoperable Global Payments

Sanghavi wrapped up with a forward-looking vision: a global payments ecosystem that is real-time and interoperable—one where users don’t need to understand the underlying technology and can transfer funds simply and instantly.

7. Broader Japanese Momentum: SBI’s Stablecoin and Tokenization Strategies

Beyond the Expo, developments in Japan underscore accelerating real-world applications. SBI Holdings is leading a three-pronged strategy for stablecoin deployment, involving Circle’s USDC, Ripple’s USD-backed RLUSD, and a JPY-backed stablecoin with SMBC. They are also launching “Project Trinity,” a consortium to bring tokenized real-world assets to the Japanese market.

Conclusion

Innovations in digital currency are poised to transform cross-border payments by solving the traditional threefold challenge: cost, speed, and transparency. The collaborative and forward-looking approach displayed by VISA, the Bank of Japan, and Ant International reflects real-world momentum—combining pilot implementations, central bank initiatives, and inclusive financial services.

For technology practitioners and crypto-savvy innovators, the opportunities are manifold. Stablecoins, CBDCs, and tokenized assets are not speculative offshoots—they’re being integrated by major institutions and local regulators. Whether you’re exploring blockchain-based remittance services, institutional fintech integration, or AI-enhanced inclusion platforms, now is the time to engage with this evolving ecosystem.