Key Points :

- Mastercard, Western Union, and Worldpay join as early adopters of Solana’s enterprise platform

- Over 20 infrastructure partners and 11 wallet providers integrated at launch

- Introduction of a modular API system: issuance, payments, and trading

- Growing institutional demand for stablecoins, tokenized deposits, and real-world assets (RWA)

- AI-native development compatibility signals a shift toward automated financial infrastructure

1. A Turning Point: Solana Moves Beyond Retail Crypto

The launch of the Solana Developer Platform (SDP) marks a decisive turning point not only for Solana but for the broader blockchain industry. Historically, Solana has been known for its high throughput and low transaction costs, attracting retail traders, NFT platforms, and crypto-native applications. However, this new initiative signals a strategic pivot: from a retail-focused ecosystem toward a full-scale enterprise-grade financial infrastructure.

This shift reflects a broader industry trend. Over the past two years, institutional players have increasingly entered the digital asset space—not through speculative trading, but through infrastructure, payments, and tokenization. Financial institutions are no longer asking whether blockchain is viable; instead, they are asking how quickly it can be integrated into existing systems.

The SDP is Solana’s answer to this demand. By offering a unified API-based environment, the platform reduces the complexity traditionally associated with blockchain development. Enterprises no longer need to build custom integrations for wallets, compliance tools, and liquidity providers. Instead, they can access a pre-integrated ecosystem designed specifically for financial applications.

This approach mirrors what cloud computing did for software development. Just as AWS abstracted away infrastructure management, SDP aims to abstract blockchain complexity—making it accessible to banks, payment processors, and fintech companies.

2. The Architecture of SDP: Modular Finance for the Digital Age

At the core of SDP are three modular APIs:

- Issuance Module

- Payment Module

- Trading Module (coming in 2026)

These modules are not just technical components—they represent the building blocks of a new financial system.

The issuance module enables the creation of tokenized deposits, stablecoins, and real-world assets (RWA). This is particularly important as banks explore tokenized versions of fiat currencies. For example, a tokenized deposit equivalent to $1 USD can move instantly across borders while maintaining regulatory compliance.

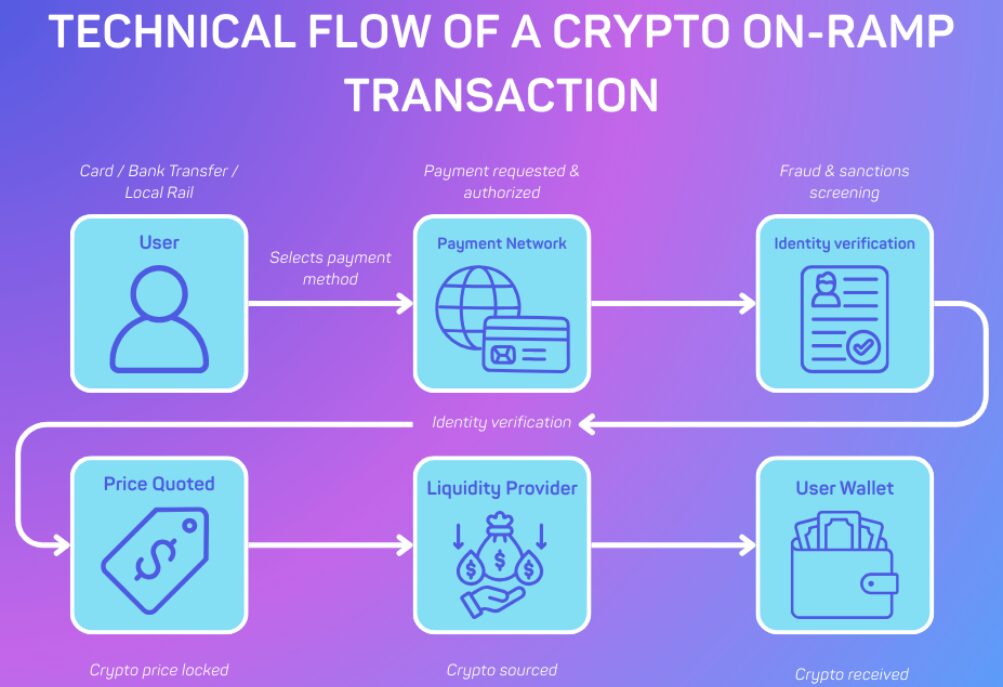

The payment module handles the flow of both fiat and stablecoins. It supports on-ramps, off-ramps, and transactions across B2B, B2C, and P2P contexts. This effectively bridges traditional finance and blockchain, allowing businesses to accept stablecoin payments while settling in fiat if needed.

The trading module, expected later in 2026, will enable liquidity and exchange functionalities directly within the platform. This could significantly reduce reliance on external exchanges, creating a more integrated financial environment.

Architecture of Solana Developer Platform (SDP)

3. Institutional Adoption: Why Mastercard and Western Union Matter

The involvement of Mastercard, Worldpay, and Western Union is not مجرد symbolic—it is foundational.

Mastercard’s participation signals a major step toward integrating stablecoin payments into global merchant networks. With billions of transactions processed annually, even a small percentage shift toward blockchain-based settlement could represent trillions of dollars in volume.

Western Union’s use case is equally significant. Cross-border remittances remain one of the most expensive segments in finance, often costing between $5 and $25 per transaction. By leveraging stablecoins and blockchain rails, these costs can be reduced dramatically, potentially to below $1 per transaction.

Worldpay, on the other hand, brings merchant acquisition and settlement capabilities. Its integration suggests that stablecoin acceptance could soon become as seamless as credit card payments.

Together, these companies form a bridge between traditional finance and blockchain infrastructure.

4. Compliance as a First-Class Feature

One of the biggest barriers to institutional adoption of blockchain has been regulatory compliance. SDP addresses this directly by integrating leading compliance providers such as Chainalysis, Elliptic, and TRM Labs.

These tools enable:

- KYC (Know Your Customer)

- KYB (Know Your Business)

- FATF Travel Rule compliance

This is crucial. Without compliance, blockchain cannot scale in regulated environments. By embedding compliance directly into the platform, Solana removes one of the largest friction points for enterprises.

In effect, SDP transforms blockchain from a “permissionless experiment” into a “regulated financial infrastructure.”

5. The Rise of Tokenized Assets and Stablecoins

The timing of SDP’s launch aligns with a major macro trend: the rise of tokenized assets.

Tokenized real-world assets (RWA) are projected to reach trillions of dollars in value over the next decade. These include:

- Tokenized bonds

- Tokenized real estate

- Tokenized deposits

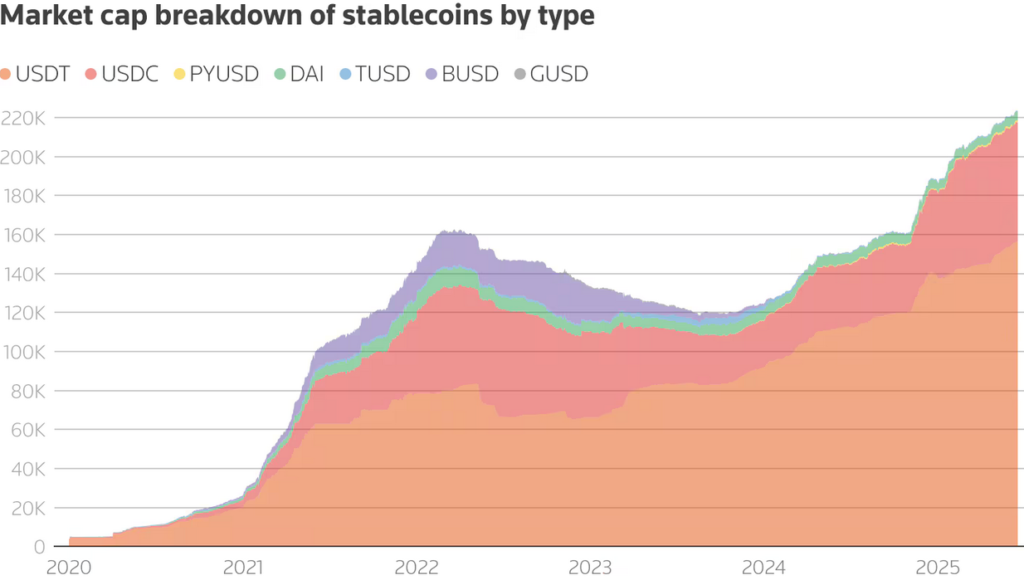

Stablecoins, already exceeding $150 billion in market capitalization globally, are becoming a core component of digital finance. Unlike volatile cryptocurrencies, stablecoins provide price stability, making them suitable for payments and settlements.

Growth of Stablecoins and Tokenized Assets (USD)

6. AI Meets Blockchain: The Next Development Paradigm

One of the most forward-looking aspects of SDP is its compatibility with AI coding platforms such as Claude Code and OpenAI Codex.

This is not a minor feature—it represents a fundamental shift in how financial systems will be built.

In the near future, developers may not manually write smart contracts. Instead, they will describe financial products in natural language, and AI systems will generate compliant, secure code using platforms like SDP.

This convergence of AI and blockchain could lead to:

- Rapid prototyping of financial products

- Automated compliance checks

- Reduced development costs

- Faster time-to-market

7. Strategic Implications: A New Financial Stack Emerges

The introduction of SDP suggests that blockchain is entering a new phase: the infrastructure phase.

In this phase:

- Blockchain becomes invisible to end users

- Financial services are API-driven

- Stablecoins act as settlement layers

- Compliance is embedded by design

This mirrors the evolution of the internet. Just as users do not think about TCP/IP when browsing websites, future users may not think about blockchain when making payments.

Evolution of Financial Infrastructure

Conclusion: From Crypto Experiment to Financial Backbone

The Solana Developer Platform represents more than just a technical upgrade—it is a strategic move toward making blockchain the backbone of modern finance.

By combining modular APIs, institutional partnerships, compliance integration, and AI compatibility, Solana is positioning itself at the center of the next financial revolution.

For investors and builders, the implications are clear:

- The opportunity is shifting from tokens to infrastructure

- Revenue models will increasingly come from services, not speculation

- The winners will be those who can bridge traditional finance and blockchain

In this new landscape, platforms like SDP are not just tools—they are the foundation upon which the next generation of financial systems will be built.