Main Points :

- Ruya Bank becomes the world’s first Islamic bank to offer Sharia-compliant Bitcoin trading directly inside its mobile app.

- Bitcoin is officially approved as part of the bank’s long-term wealth management tools after review by its Sharia Governance Committee.

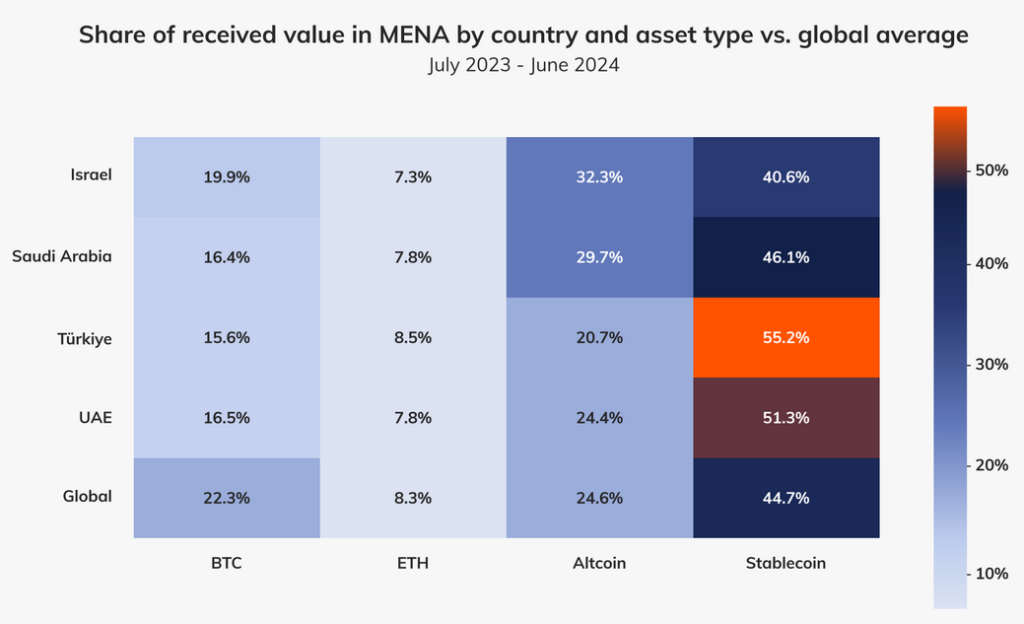

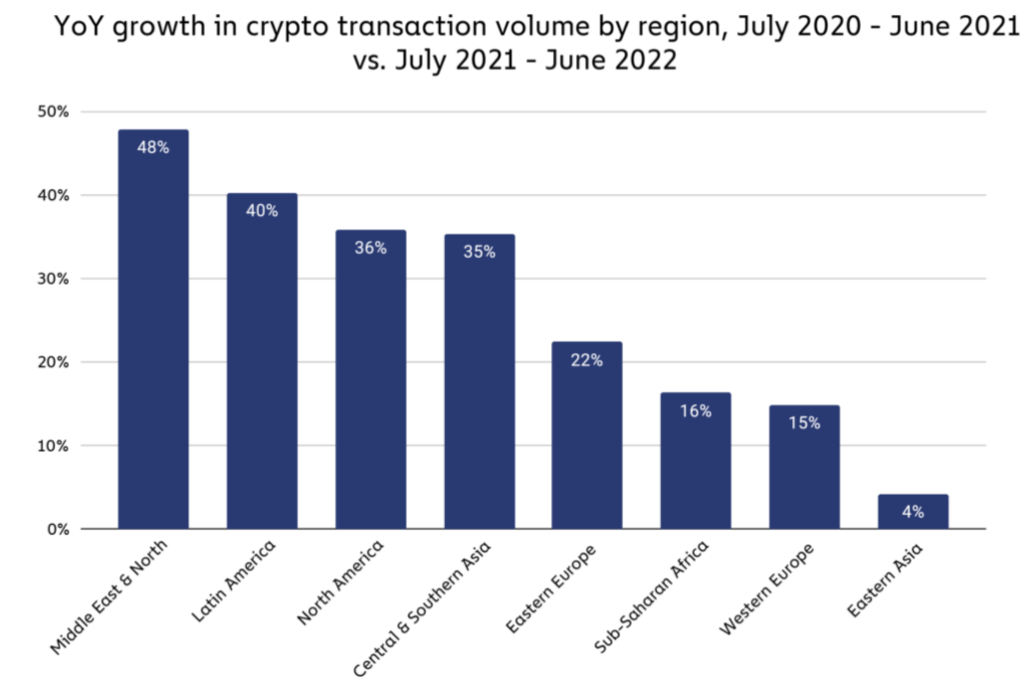

- UAE crypto inflows exceeded $30 billion between July 2023 and June 2024, up 42% year-over-year, according to Chainalysis.

- Partnership with Fuze ensures licensed digital asset infrastructure, AML compliance, and secure custody.

- This move strengthens the UAE’s ambition to be a global crypto hub, while opening a compliant gateway for Muslim investors worldwide.

- Sharia-aligned crypto access is expected to create new revenue streams and legitimize digital assets within Islamic finance.

1. Introduction: A Landmark Moment for Islamic Finance

The intersection of Islamic banking and modern digital assets has long been a topic of careful regulatory, ethical, and scholarly evaluation. While the global Islamic finance market exceeds $4 trillion, access to cryptocurrencies has largely been limited due to concerns around volatility, uncertainty (gharar), speculation (maysir), and compliance with ethical investment frameworks.

Against this backdrop, Ruya Bank, a UAE-based digital-first Islamic institution, has accomplished what no other Sharia-compliant bank has done before: enabling customers to buy and sell Bitcoin directly within a regulated banking application.

With the approval of its Sharia Governance Committee and through strategic collaboration with the licensed digital asset provider Fuze, Ruya Bank is emerging as a pioneer in compliant crypto access, bridging Islamic ethical finance and cutting-edge blockchain technology.

2. UAE’s Expanding Crypto Market and Why Ruya’s Move Matters

The UAE has rapidly grown into one of the world’s most forward-looking crypto jurisdictions. Between July 2023 and June 2024, the country recorded over $30 billion in digital asset inflows, placing it far above regional averages. Dubai’s VARA regulatory framework and Abu Dhabi Global Market’s progressive digital asset rules play a central role in enabling safe institutional adoption.

But despite strong demand, Muslim investors have lacked fully Sharia-compliant access points. Many avoided global exchanges due to concerns over custody, regulatory clarity, and adherence to Islamic principles.

Ruya Bank directly addresses these barriers by offering:

- Regulated in-app Bitcoin access

- Full AML/KYC alignment

- Transparent pricing and compliant custody

- Sharia-certified oversight ensuring ethical use

This initiative is expected to encourage more conservative or ethically focused investors to participate in the crypto economy without compromising religious standards.

3. Sharia Compliance and Why Bitcoin Passed Review

Islamic scholars evaluating crypto often analyze issues such as:

• Intrinsic Value

Bitcoin is increasingly recognized as a scarce digital commodity with utility as a store of value.

• Avoidance of Interest (Riba)

Bitcoin transactions, when handled properly, do not involve interest-based mechanisms.

• Transparency and Fraud Prevention

Blockchain’s immutable ledger aligns with Islamic values of fairness and accountability.

• Ownership and Custody

Digital assets must be held in a way that ensures real, provable ownership—supported by Fuze’s custodial infrastructure.

Ruya Bank’s Sharia Governance Committee determined that Bitcoin, when offered within a controlled custodial framework with appropriate auditability, meets the criteria for permissible (halal) investment. This makes Ruya Bank a reference point for future Islamic finance digital asset frameworks.

4. How Ruya Bank and Fuze Deliver Secure, Ethical Access

4.1 Licensed Digital Asset Infrastructure

Fuze provides:

- Institutional-grade custody

- Compliant transaction monitoring

- Full financial reporting traceability

- Audit-friendly ledger integration

Each transaction is recorded according to standard reporting procedures, ensuring transparency for regulators and auditors.

4.2 Full AML/KYC Compliance

By integrating crypto flows into existing risk management systems, the bank ensures that:

- Transactions comply with UAE and international AML rules

- Customer identity data is verified and retained properly

- Suspicious activity monitoring is unified across fiat and crypto channels

This creates one of the safest pathways for crypto participation within the Middle East.

5. Graphs & Visuals

“UAE Crypto Inflows Over Time”

This chart visually illustrates the rapid expansion of the UAE’s digital asset inflows, contextualizing the environment in which Ruya Bank made its strategic move.

“Adoption of Bitcoin in Islamic Finance”

This visual represents a conceptual trend of increasing institutional Islamic engagement with Bitcoin.

6. Global Context: Rising Interest in Sharia-Compliant Crypto Products

Across Southeast Asia, the Middle East, and Africa, there is accelerating momentum behind Muslim-friendly financial technologies.

Examples include:

- Indonesia’s growing halal-compliant digital gold and crypto education initiatives

- Malaysia’s Islamic fintech sandbox exploring blockchain for sukuk issuance

- Saudi Arabia’s government-backed blockchain pilots

- Pakistan and Nigeria, where young populations show increasing crypto adoption

However, none of these countries have yet provided Sharia-compliant banking access to Bitcoin on the level Ruya Bank has introduced.

This positions the UAE as the global leader in regulated Islamic crypto finance.

7. New Revenue Streams and Strategic Advantages for Ruya Bank

By offering Bitcoin access directly inside the app, Ruya Bank taps into multiple revenue opportunities:

- Trading spreads and fees

- Custody-related service income

- Long-term wealth management packages

- Cross-selling digital financial products

More importantly, Ruya Bank becomes the primary gateway for millions of potential Muslim crypto investors who previously lacked compliant options.

For customers, the advantages include:

- Safe, regulated, trusted environment

- No need to transfer funds to offshore exchanges

- Ethical approval and peace of mind

- Consolidated wealth management inside one ecosystem

This integrated structure may quickly become the new standard for Islamic digital finance.

8. How This Shapes the Future of Islamic Banking

Ruya Bank’s launch signals a broader shift:

• Islamic banks must modernize and innovate

Customers expect digital-first experiences.

• Crypto is no longer an experimental asset

Institutional adoption is accelerating across Europe, Asia, and the Middle East.

• Sharia compliance can coexist with blockchain systems

Transparent, auditable ledgers fit naturally with ethical financing standards.

• New financial products will emerge

Potential future developments include:

- Sharia-compliant crypto funds

- Tokenized sukuk on blockchain

- Halal digital commodity baskets

- Cross-border remittance platforms using stablecoins

Ruya Bank’s move is not just a new feature—it is the beginning of a structural transformation in how Islamic finance interacts with digital assets.

9. Conclusion

Ruya Bank’s integration of Sharia-compliant Bitcoin trading marks a historic leap forward for Islamic finance and digital asset accessibility. By providing a secure, regulated, and ethically governed platform, the bank opens doors for millions of investors who previously lacked a compliant way to participate in Bitcoin markets.

This development enhances the UAE’s position as a global crypto hub, encourages responsible adoption, and lays the foundation for new Islamic fintech innovations. As demand for digital assets continues to rise worldwide, Ruya Bank’s pioneering initiative will likely serve as the blueprint for Islamic financial institutions across the Middle East, Southeast Asia, and beyond.