Main Points :

- October VIX futures command a historically high premium over September contracts, signaling elevated market uncertainty after the expected September Fed rate cut.

- The front-month (September) VIX futures trade only at a slight premium to the cash index, indicating that traders are discounting risk ahead of the Fed decision.

- Historically, large spreads in VIX futures precede increased volatility and equity drawdowns.

- Bitcoin’s volatility indices (BVIV, DVOL) now correlate strongly with the S&P 500 VIX, underlining crypto’s growing alignment with traditional markets.

- Institutional adoption is further integrating Bitcoin into traditional financial ecosystems, raising its systemic risk and diminishing its diversification value.

1. VIX Futures Premium: A Warning Bell for the Markets

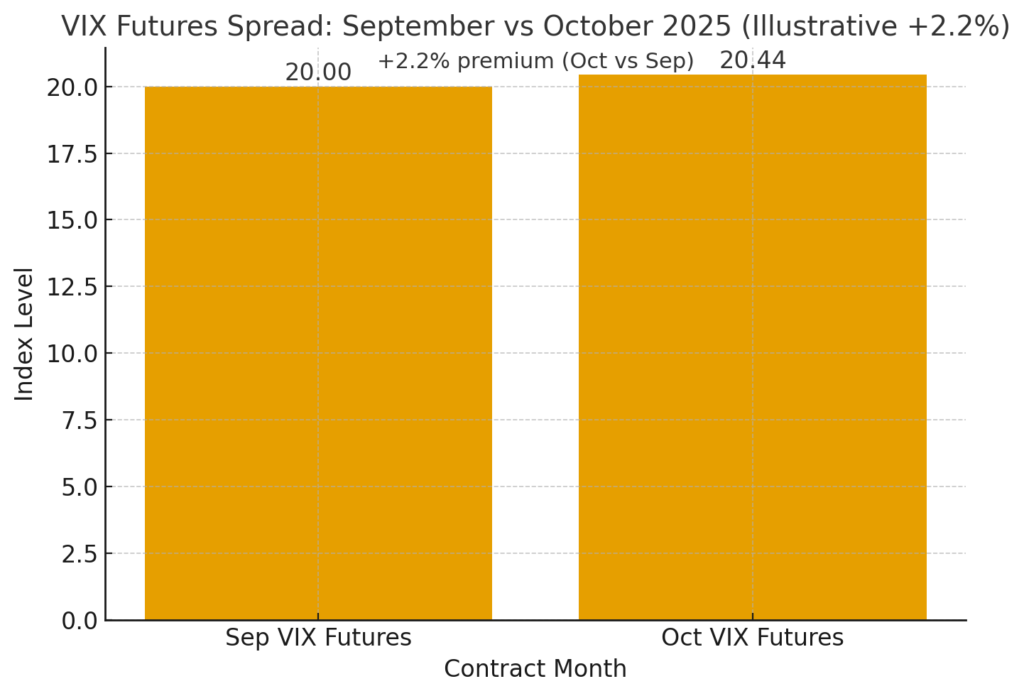

Investors keep a keen eye on VIX futures—a market’s “fear gauge”—to assess expected S&P 500 volatility. In early September 2025, the spread between October and September VIX futures widened to approximately 2.2%. Such a magnitude is historically extreme.

The separation in pricing serves as a red flag. While the September contract reflects low pre-Fed risk pricing, the much higher cost of October futures implies that traders anticipate spikes in volatility after the Fed’s meeting on September 17. The September contract, expiring the same day as the policy decision, carries only a modest premium over the cash (spot) VIX index, signaling that markets expect calm up to the announcement.

Amberdata’s Derivatives Director, Greg Magadini, interprets this dynamic clearly: “September VIX futures have priced away risk, whereas October could be ugly… a theme to remember for risk assets,” reinforcing the notion that market participants foresee turbulence after the policy decision.

2. Historical Context: Why VIX Spreads Matter

The VIX typically moves inversely to equity prices—when uncertainty rises, volatility spikes and stock prices tend to fall. A wide spread between near-term and next-month VIX futures often precedes turbulence in risk assets. In this case, the historical extremity of the 2.2% spread suggests traders expect meaningful volatility ahead, possibly with downward pressure on equity markets.

3. Crypto’s Reflection of Wall Street: Volatility Correlation

Bitcoin’s behavior is increasingly mirroring traditional financial markets. Recent data shows that the 90-day correlation coefficient between Bitcoin’s implied volatility indices (BVIV, DVOL) and the S&P 500 VIX reached an all-time high of 0.88.

Such a close alignment indicates that Bitcoin is becoming a “fear gauge” in its own right—its volatility rising during risk-off periods alongside equities. The shift is driven by growing institutional participation in crypto, particularly with strategies involving volatility selling (writing options), which link crypto volatility dynamics to broader market sentiment.

4. Institutional Adoption Strengthens Market Integration

Beyond volatility, Bitcoin is increasingly embedded in institutional frameworks. A recent academic study highlights that Bitcoin’s correlation with major equity indices like the Nasdaq 100 and S&P 500 surged in recent years—peaking around 0.87 in 2024—driven by factors such as crypto ETFs and corporate Bitcoin holdings.

This growing interconnection raises important implications: Bitcoin is transitioning from an alt-asset to a close cousin of traditional financial assets. It challenges its diversification benefit and elevates its transmission of systemic risk in periods of macroeconomic stress.

5. Synthesis: What Risk-Seeking Investors Should Take Away

For readers seeking new crypto assets, additional revenue sources, or practical blockchain applications, this evolving landscape offers both opportunity and caution:

- Volatility as opportunity: The elevated VIX futures spread signals potential price dislocations—both in equities and crypto—that active traders might exploit.

- Crypto’s fading safe-haven status: As Bitcoin’s volatility tracks Wall Street more closely, it may not offer the same hedging appeal it once did. Expect crypto drawdowns to mirror equity stress.

- Institutional behavior matters: Growing use of instruments like crypto ETFs and options means institutional sentiment can sway crypto volatility sharply. It’s no longer an isolated frontier.

- Timing and diversification shift: Markets may calm ahead of the Fed decision (as priced in), but investors should brace for turbulence afterward. Diversification strategies may need adjusting accordingly.

Conclusion

October’s VIX futures premium over September stands out as a stark warning: markets expect a wave of volatility after the Fed’s rate cut. Bitcoin, with its record-high volatility correlation to the VIX, underscores how tightly crypto markets now mirror traditional financial sentiment.

For practitioners, traders, and blockchain professionals—this convergence means that risk in one market is now mirrored in the other. Volatility becomes not just a feature but a systemic connector. As investors hunt new crypto opportunities or consider practical deployments of blockchain technology, understanding this synchronization is key.