Key Points :

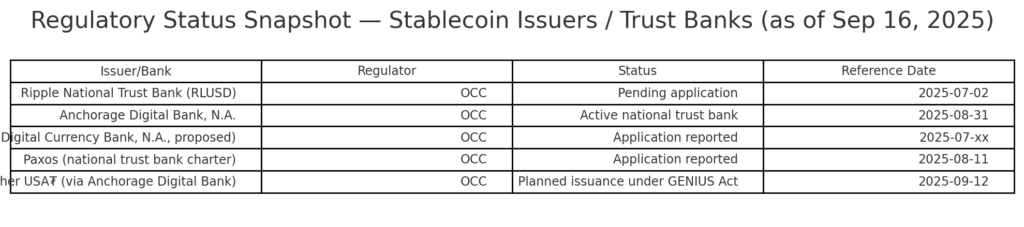

- Ripple has filed for a national trust bank charter with the U.S. OCC to operate “Ripple National Trust Bank” (RNTB), focused on issuing and managing its stablecoin RLUSD and related digital-asset infrastructure.

- The U.S. passed the GENIUS Act in July 2025, setting up a regulatory framework for stablecoins: full reserve backing, audits, licensing of issuers, reserve disclosures, etc.

- There is debate on whether RLUSD under this framework will supplant some of XRP’s roles (especially as bridge / liquidity asset), or whether RLUSD’s more regulated status will complement XRP by increasing on-ledger usage and demand for XRP in swaps, fees, AMMs, etc.

- Ripple is also seeking a Federal Reserve master account, and plans to keep RLUSD reserves with high-quality liquid assets, like U.S. Treasuries, to meet regulatory requirements.

- Critics (regulators, community groups, banks) have raised concerns about consumer protection, the bypassing of existing banking rules (e.g. deposit insurance, obligations under Community Reinvestment Act), and potential competitive or systemic risks.

Context: Ripple, RLUSD & the National Trust Bank Application

In July 2025, Ripple officially applied to the U.S. Office of the Comptroller of the Currency (OCC) for a national trust bank charter for a wholly-owned subsidiary to be known as Ripple National Trust Bank (RNTB). The plan is for RNTB to handle fiduciary services, necessary infrastructure, and management of the RLUSD stablecoin, especially its reserves. Importantly, this is not a full deposit/lending bank; Ripple explicitly describes it as a “limited-purpose” trust bank.

Separately, the U.S. Congress passed the GENIUS Act (“Guiding and Establishing National Innovation for U.S. Stablecoins”) on July 18, 2025, implementing a comprehensive stablecoin regulatory framework. Under the Act:

- Stablecoin issuers must maintain reserves in liquid, low-risk assets (U.S. dollars, short-term Treasuries, etc.).

- Monthly reserve disclosures and annual audits are required.

- Issuers must be licensed / recognized under federal regulation (and state oversight where applicable).

Thus, Ripple’s RLUSD project, plus the RNTB application, appear designed to align with the new law, potentially giving them first-mover advantage among regulated stablecoins.

Possible Outcomes: How RLUSD Might Affect XRP

There are several possible scenarios for how this regulatory change + institutional structuring might shift XRP’s role. Here are a few:

Scenario A: RLUSD replaces part of XRP’s bridge / settlement role

If RLUSD becomes very widely accepted, especially in cross-border payments, payment flows and liquidity operations, then some of the use-cases where XRP currently serves as a bridge or liquidity asset could be handled directly by RLUSD or stablecoin-based rails. That could reduce demand for XRP in those use-cases. For example, rather than using XRP to move value and then converting to a fiat or stablecoin, institutions might use RLUSD directly.

Scenario B: RLUSD and XRP act in tandem, enhancing XRP demand

Alternatively, RLUSD’s activity on the XRP Ledger (XRPL) could increase trading pairs with XRP, more usage in AMMs, more transaction volume on XRPL, more fees (which are paid in XRP), etc. In that case, XRP could benefit from RLUSD’s growth, as RLUSD might strengthen overall ecosystem liquidity. Also, if RLUSD issuers need liquidity bridges, XRP might still be part of the routing / liquidity provisioning.

Scenario C: Regulatory clarity boosts institutional confidence

One often-underappreciated effect is that the GENIUS Act and Ripple’s bank charter application reduce regulatory uncertainty—something that has weighed on XRP in the past (e.g. SEC litigation). For many institutions, clearer rules around stablecoins and digital assets mean lower legal risk, better compliance visibility, and more willingness to participate. This could raise demand for RLUSD, but also for XRP in utility roles (settlement, liquidity, cross-asset flows).

Challenges, Criticisms & Risks

While the developments are promising for Ripple / RLUSD / XRP, there are significant hurdles and risks to watch.

- Regulatory resistance / oversight: Groups such as the National Community Reinvestment Coalition (NCRC) and various community and banking groups have raised concerns about Ripple’s bank charter application, especially about lax consumer protections, how stablecoins could drain deposits from traditional banks, and how Ripple’s RNTB might avoid some obligations like those under the Community Reinvestment Act.

- Implementation risk: Even though the law is passed, many details (regulation compliance, audits, reserve management, enforcement) remain to be filled out. Ripple will need to demonstrate that RLUSD reserves, transparency, infrastructure etc. meet regulators’ expectations. Any misstep could damage reputation or lead to regulatory pushback.

- Competition: Other stablecoin issuers (e.g. Circle / USDC, Tether / others) are also racing to comply, secure trust bank charters, get Fed master accounts, etc. Ripple’s first mover status helps, but competitive pressure is real.

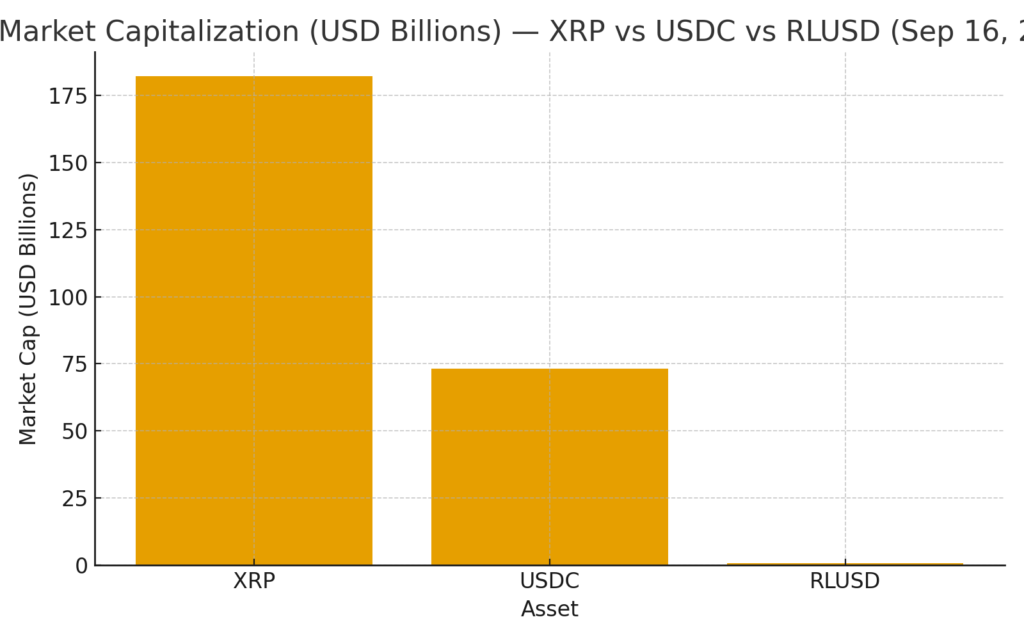

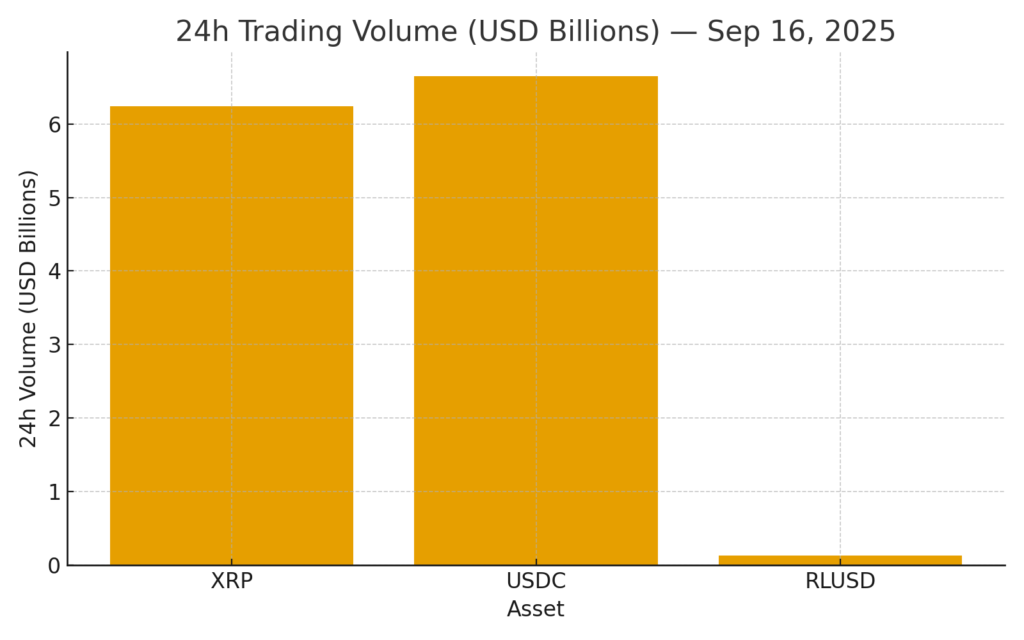

- Market dynamics & demand: Even with regulatory clarity, adoption of RLUSD must be achieved — usage by payment service providers, institutions, exchanges, cross-border flows etc. If RLUSD remains small or limited, its impact on XRP will be correspondingly modest. Currently RLUSD’s market cap is significantly smaller than USDC or USDT.

Recent Developments & Data

To give a sense of the momentum:

- On July 2, 2025, Ripple filed the national trust bank charter application with the OCC.

- The GENIUS Act became law on July 18, 2025.

- XRP rose by ~6% in mid-July when the House advanced the GENIUS Act, reflecting investor optimism around regulatory clarity.

- The float / market cap of RLUSD is on the order of US$400-500 million (or somewhat under US$500 million) at the time of the reports — much smaller than the major stablecoins like USDC/USDT, but growing.

What to Watch Next

To assess whether XRP benefits or is partially displaced, keep an eye on:

- Whether OCC approves Ripple’s national trust bank charter, and whether RNTB also acquires a Federal Reserve master account. These determinations will shape how RLUSD operates (e.g. access to payments systems, reserve custody, credibility).

- How detailed regulations / implementing rules under the GENIUS Act are enforced — especially rules about reserve backing, disclosures, audits. If RLUSD meets them solidly, trust increases.

- Market adoption: whether RLUSD is integrated into payments rails, used by financial institutions, exchanges, etc. Also whether RLUSD/XRP trading pairs on XRPL increase, more activity in XRP-based AMMs/liquidity‐routing.

- XRP’s legal status / regulatory risk (SEC oversight etc.). If XRP is seen more clearly as a utility / non-security (or at least its status is not threatened), that helps upside.

- Competitive moves: what Circle, Tether, etc. are doing in applying for similar charters, securing Fed master accounts, etc. The stablecoin space is getting more regulated and competitive.

Summary

Ripple is making a major structural move to position RLUSD (its USD-pegged stablecoin) under U.S. federal regulatory oversight via a national trust bank charter (RNTB) and aligning with the recent GENIUS Act. These steps are intended to give RLUSD compliance credentials, reserve-backing transparency, and regulatory legitimacy. For XRP, this could go one of two ways: RLUSD might replace some of XRP’s bridge/utility roles, or RLUSD’s growth could reinforce XRP’s relevance, increasing on-ledger transaction volume, demand for XRP in liquidity and swaps, and fee burn (though fee burn remains relatively small per transaction). Regulatory clarity, institutional adoption, and execution will be the deciding factors. For readers interested in finding new crypto assets or revenue sources, RLUSD + XRP together might present interesting arbitrage / utility opportunity if RLUSD adoption increases and the ecosystem (XRPL) picks up traffic. XRP’s fate will depend not just on Ripple’s strategy, but on regulatory enforcement, market acceptance, and competing stablecoin projects.