Main Points :

- AMINA Bank, a FINMA-regulated Swiss digital asset bank, has become the first European bank to adopt Ripple Payments, Ripple’s licensed end-to-end payment solution.

- The partnership enables near-instant cross-border payments, bridging fiat currencies and blockchain-based settlement without reliance on legacy correspondent banking.

- Ripple’s stablecoin RLUSD and other stable assets play a central role in liquidity efficiency and settlement transparency.

- This move signals a broader institutional shift toward blockchain-native payment rails in Europe.

- Ripple’s global payment network now covers over 90% of global FX corridors, with cumulative processing volume exceeding $95 billion.

- The collaboration expands an existing relationship, as AMINA already became the world’s first bank to provide custody and trading for RLUSD earlier in 2025.

1. Introduction: A Turning Point for Blockchain Payments in European Banking

The announcement that Ripple has partnered with Switzerland-based AMINA Bank marks a defining moment for blockchain adoption within Europe’s regulated banking sector. While blockchain-based payments have long promised faster, cheaper, and more transparent cross-border transactions, institutional adoption—particularly among fully licensed banks—has remained cautious.

AMINA Bank, regulated by the Swiss Financial Market Supervisory Authority (FINMA), has now become the first European bank to deploy Ripple’s licensed end-to-end payment infrastructure, known as Ripple Payments. This decision places AMINA at the forefront of a structural shift in how banks perceive blockchain—not as an experimental add-on, but as a core settlement layer.

This partnership demonstrates how blockchain technology is transitioning from fintech experimentation into regulated financial infrastructure, reshaping the future of global payments.

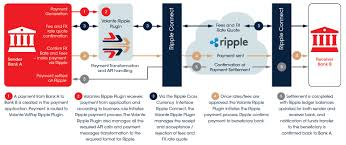

2. What Is Ripple Payments? Licensed Blockchain Settlement at Bank Grade

Ripple Payments is Ripple’s enterprise-grade payment solution designed specifically for regulated financial institutions. Unlike early blockchain payment systems that required banks to operate outside traditional compliance frameworks, Ripple Payments is fully licensed and designed to integrate seamlessly with existing banking operations.

Key characteristics include:

- Near-real-time settlement across borders

- Integrated compliance and reporting

- Multi-currency support, including stablecoins

- Elimination of pre-funded nostro/vostro accounts

- Full transparency and traceability of transactions

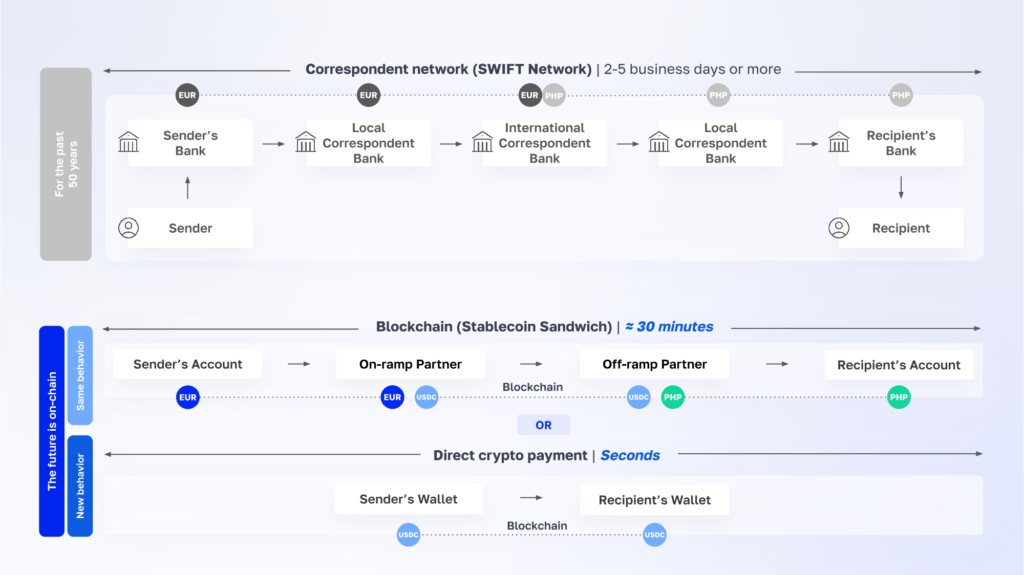

By adopting Ripple Payments, AMINA Bank enables its clients to move funds internationally without relying on slow correspondent banking networks such as SWIFT-based chains, which often require multiple intermediaries and delayed reconciliation.

Comparison of Traditional Correspondent Banking vs Ripple Payments Settlement Flow

3. AMINA Bank: A Regulated Digital Asset Pioneer in Switzerland

AMINA Bank is not a newcomer to digital assets. Formerly known as SEBA Bank, AMINA has positioned itself as a fully regulated bridge between traditional finance and blockchain ecosystems. Operating under FINMA supervision, AMINA offers:

- Digital asset custody

- Crypto trading and brokerage

- Tokenization services

- Fiat and crypto banking under one license

Earlier in 2025, AMINA became the first bank globally to provide custody and trading services for Ripple’s U.S. dollar stablecoin, RLUSD. That initial step laid the foundation for deeper operational integration.

With the adoption of Ripple Payments, the partnership now extends beyond asset custody into core payment infrastructure, representing a strategic escalation in scope.

4. Stablecoins at the Core: The Strategic Role of RLUSD

A critical component of this partnership is the role of stablecoins, particularly Ripple USD (RLUSD). Stablecoins solve a persistent problem in cross-border finance: liquidity fragmentation.

Traditional cross-border payments often require banks to maintain idle capital across multiple currencies and jurisdictions. Stablecoins allow:

- On-demand liquidity

- Atomic settlement

- Reduced FX risk exposure

- 24/7 availability, unlike traditional banking rails

By leveraging RLUSD and other compliant stablecoins, AMINA clients gain access to efficient settlement while maintaining regulatory clarity—an essential requirement for institutional adoption.

Stablecoin-Based Liquidity Flow in Cross-Border Payments

5. Regulatory Alignment: Why Switzerland Matters

Switzerland’s regulatory environment has played a decisive role in enabling this development. FINMA has long provided clear guidance for digital asset custody, trading, and blockchain-based financial services.

This regulatory clarity allows institutions like AMINA to adopt blockchain infrastructure without legal ambiguity. Ripple’s emphasis on licensed and compliant deployment aligns closely with European regulators’ expectations, distinguishing it from unregulated payment experiments.

For other European banks observing this move, the message is clear: blockchain adoption is now compatible with regulatory compliance—if done correctly.

6. Ripple’s Global Expansion Strategy Comes into Focus

Ripple’s collaboration with AMINA is not an isolated event. It reflects a broader global strategy focused on regulatory-first expansion.

Ripple Payments is currently available in:

- Switzerland

- United States

- Singapore

- Australia

- Brazil

- Mexico

- Dubai

According to Ripple, its payment network now covers over 90% of global foreign exchange corridors, with cumulative processed volume exceeding $95 billion.

This scale is critical. Payment networks derive value not merely from technology, but from network effects. Each new regulated bank strengthens the system’s institutional credibility.

Global Coverage of Ripple’s Payment Network

7. Strategic Implications for Banks and Fintechs

For banks, this partnership illustrates a viable blueprint for blockchain adoption:

- Start with custody and asset services

- Expand into settlement and payments

- Maintain full regulatory alignment

- Integrate stablecoins as liquidity instruments

For fintech firms, it signals that bank-grade blockchain infrastructure is becoming the competitive standard. Speed alone is no longer enough; compliance, transparency, and scalability are decisive.

8. What This Means for Crypto Investors and Builders

For readers seeking new digital assets, revenue models, or blockchain use cases, this development carries several implications:

- Institutional adoption increases demand for compliant blockchain infrastructure

- Stablecoins are becoming operational tools, not speculative instruments

- Payment-focused blockchain networks may see renewed institutional relevance

- Banking integration reduces long-term adoption risk

Ripple’s strategy contrasts with purely decentralized models by emphasizing institutional trust and regulatory cooperation—a path that may define the next phase of blockchain finance.

9. Conclusion: From Experiment to Infrastructure

The partnership between Ripple and AMINA Bank represents more than a product deployment—it marks a transition. Blockchain payments in Europe are moving from proof-of-concept toward regulated infrastructure.

By combining Ripple’s licensed payment technology with AMINA’s regulatory credibility, this collaboration demonstrates how blockchain can function as a core financial rail, not merely an auxiliary system.

For banks, fintechs, investors, and builders alike, the message is unmistakable:

Blockchain-based payments have entered the institutional era.