Key Points :

- Ripple joins Singapore’s central bank initiative led by Monetary Authority of Singapore

- Project BLOOM focuses on tokenized deposits and regulated stablecoins for global trade

- Integration of XRP Ledger and RLUSD enables programmable trade finance

- Smart contracts reduce inefficiencies and improve SME access to capital

- Major institutions like JPMorgan Chase and Stripe signal institutional convergence

1. A New Phase in Global Trade Infrastructure

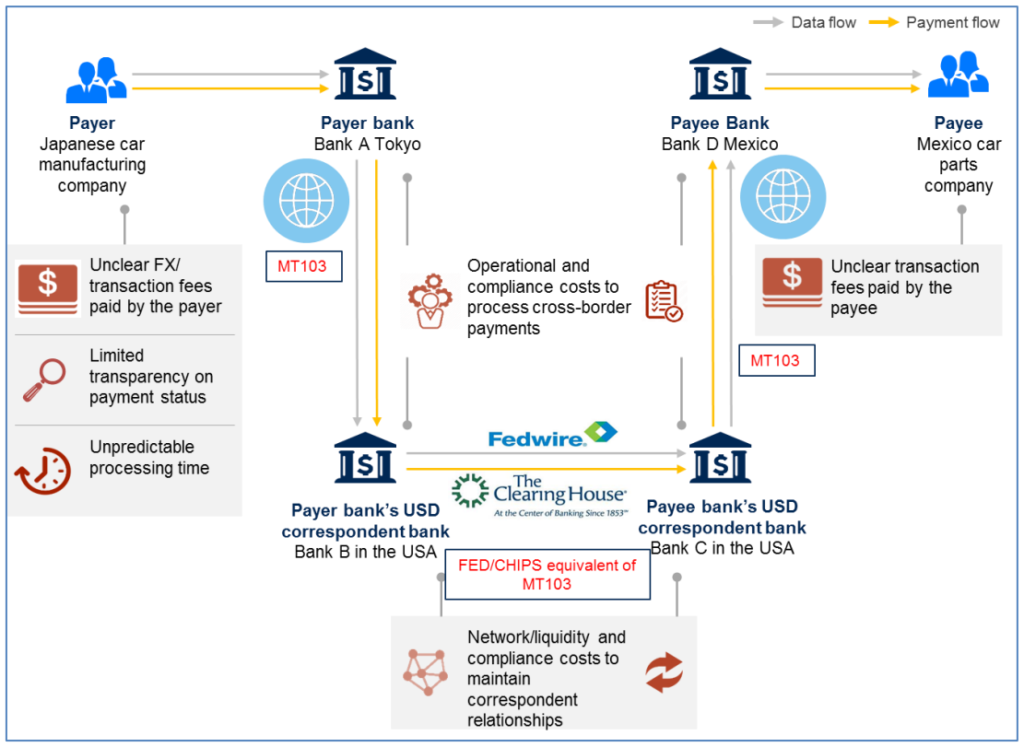

The global trade finance system—long dominated by paper-based processes, fragmented banking relationships, and slow settlement cycles—is undergoing a profound transformation. At the center of this shift is the collaboration between Ripple and the Monetary Authority of Singapore (MAS) under Project BLOOM.

Announced in March 2026, this initiative is not merely a pilot program—it represents a strategic attempt to redefine how cross-border trade payments function in a digitally interconnected world. By leveraging blockchain infrastructure, tokenized financial instruments, and programmable money, BLOOM aims to create a system that is borderless, liquid, open, online, and multi-currency.

Singapore’s role is particularly significant. As one of the most forward-thinking regulatory jurisdictions globally, MAS has consistently positioned itself as a hub for fintech innovation. Its regulatory clarity around digital assets has attracted both traditional financial institutions and crypto-native firms, creating a rare environment where experimentation can occur within a compliant framework.

2. What is Project BLOOM? A Structural Redesign

Project BLOOM is an acronym representing:

- Borderless

- Liquid

- Open

- Online

- Multi-currency

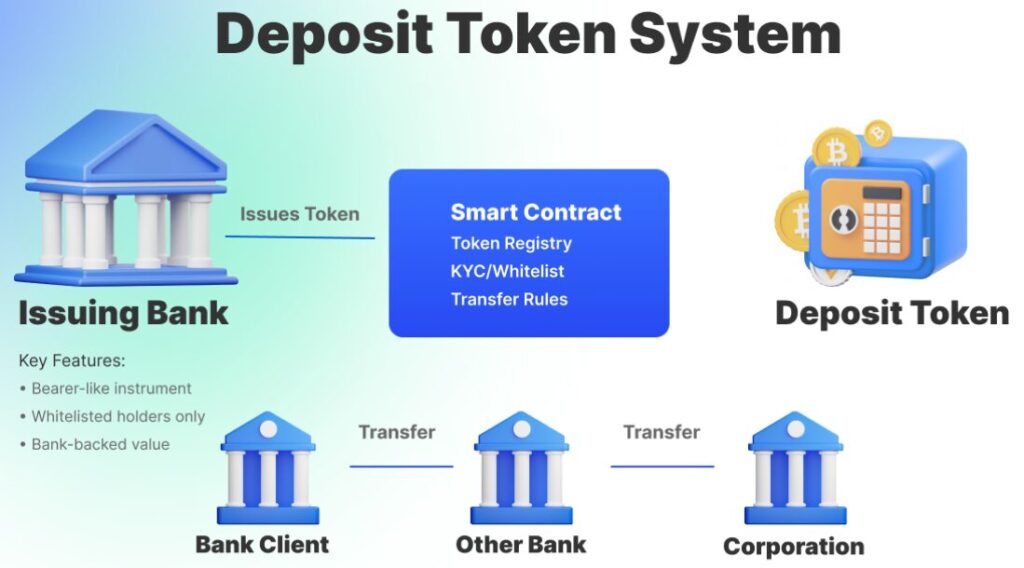

These five pillars encapsulate a vision for a next-generation financial infrastructure where tokenized bank liabilities (such as deposits) and regulated stablecoins coexist and interact seamlessly.

Unlike earlier blockchain experiments that focused primarily on cryptocurrencies, BLOOM emphasizes regulated financial instruments. This includes tokenized deposits issued by banks and stablecoins that comply with regulatory frameworks. The goal is not to replace the traditional system but to upgrade it from within.

Participants in the initiative include major global players such as JPMorgan Chase, Standard Chartered, Coinbase, Circle, and Stripe. Their involvement signals a broader convergence between traditional finance (TradFi) and decentralized finance (DeFi).

3. Ripple’s Role: XRPL and RLUSD in Trade Finance

Ripple’s contribution to BLOOM centers on the integration of the XRP Ledger (XRPL) and its stablecoin RLUSD.

XRPL is known for its high throughput, low transaction costs, and built-in decentralized exchange functionality. These features make it particularly suitable for cross-border payments, where speed and cost efficiency are critical.

The introduction of RLUSD adds another layer of utility. As a regulated stablecoin pegged to the US dollar (displayed here as $), RLUSD provides price stability while retaining the programmability of blockchain-based assets.

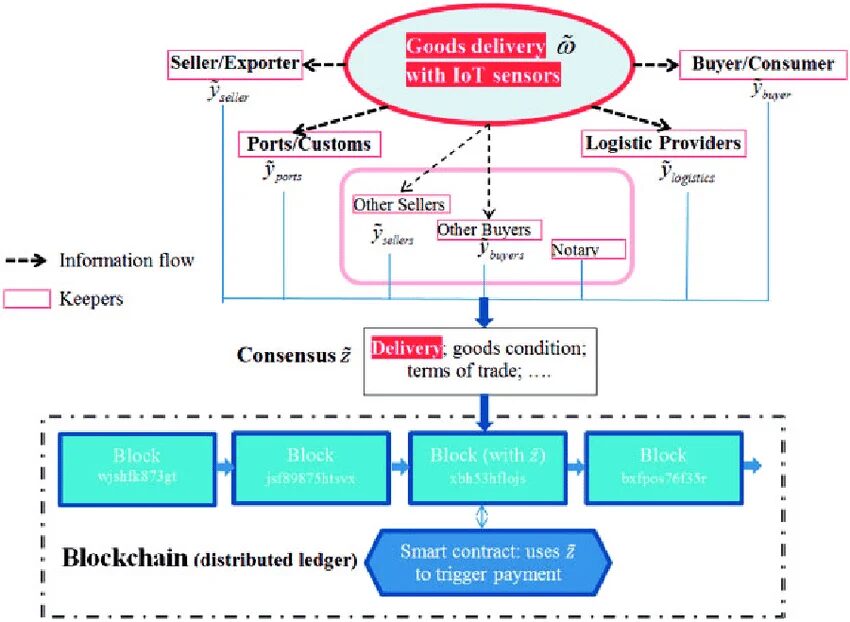

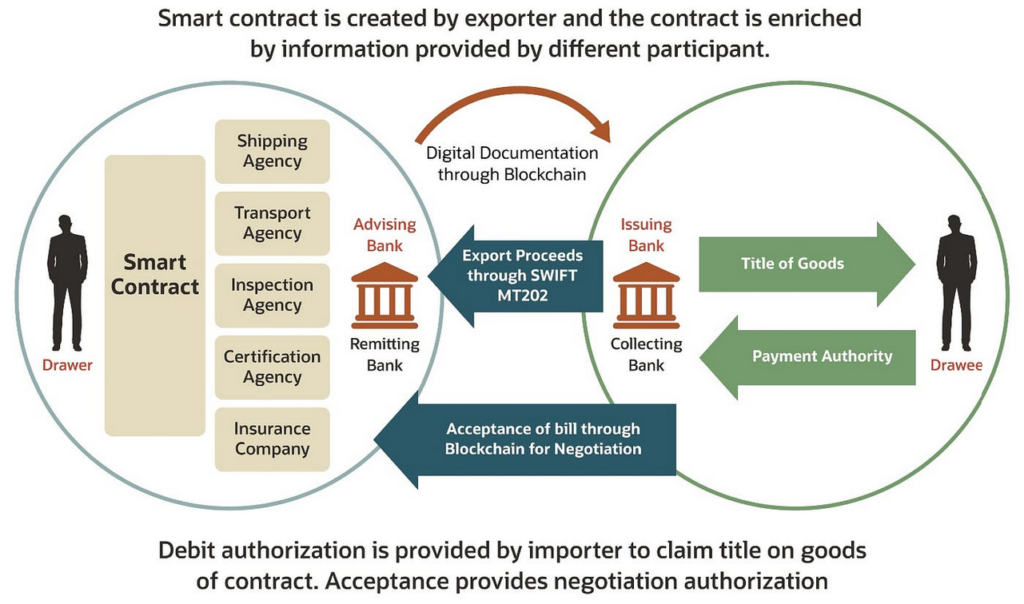

In collaboration with fintech firm Unloq, Ripple is deploying a trade finance infrastructure that uses smart contracts to automate payment execution. Payments are only released when predefined conditions—such as delivery confirmation or document verification—are met.

This model addresses one of the most persistent challenges in trade finance: counterparty risk. By embedding trust directly into the transaction logic, the need for intermediaries is reduced, and transparency is significantly enhanced.

4. Solving Structural Inefficiencies in Trade Finance

Traditional trade finance is plagued by inefficiencies:

- Manual document processing

- Long settlement times (often several days)

- High costs due to multiple intermediaries

- Limited access for small and medium enterprises (SMEs)

By contrast, blockchain-enabled systems like those being developed in BLOOM offer:

- Real-time settlement

- Programmable compliance

- Reduced operational costs

- Improved transparency

For SMEs, this transformation is particularly গুরুত্বপূর্ণ. Access to trade finance has historically been constrained by risk assessments and lack of collateral. With smart contracts and transparent transaction histories, lenders can better evaluate risk, potentially unlocking billions of dollars in previously inaccessible capital.

5. The Rise of Regulated Stablecoins in Global Payments

The inclusion of stablecoins like RLUSD reflects a broader industry trend: the rapid rise of regulated digital dollars in global finance.

Stablecoins have evolved from niche crypto tools into critical infrastructure for payments, remittances, and decentralized finance. Companies like Circle (issuer of USDC) have demonstrated how regulated stablecoins can achieve widespread adoption while maintaining compliance.

Recent developments suggest that stablecoins may soon rival traditional payment networks in certain use cases:

- Cross-border remittances

- Treasury management for global corporations

- On-chain settlement for financial institutions

In this context, BLOOM can be seen as part of a larger movement toward programmable money, where financial transactions are not only digital but also conditional and automated.

6. Institutional Convergence: TradFi Meets Blockchain

One of the most significant aspects of Project BLOOM is the participation of both traditional financial institutions and crypto-native companies.

For example, JPMorgan Chase has already developed its own blockchain-based payment network (Onyx), while Stripe has re-entered the crypto space with stablecoin integrations.

This convergence suggests that the future of finance will not be dominated by a single paradigm. Instead, it will be a hybrid system where:

- Banks issue tokenized deposits

- Stablecoins facilitate liquidity

- Blockchains provide settlement infrastructure

Such a system aligns closely with emerging regulatory frameworks, particularly in jurisdictions like Singapore, where innovation is encouraged within clearly defined boundaries.

7. Strategic Implications for Investors and Builders

For readers seeking new crypto assets, revenue opportunities, and practical blockchain applications, the implications of BLOOM are substantial.

Investment Perspective:

Projects that enable interoperability between traditional finance and blockchain—such as XRPL—are likely to gain strategic importance. Stablecoin ecosystems, in particular, represent a rapidly expanding market with significant upside potential.

Builder Perspective:

Developers and startups can explore opportunities in:

- Trade finance platforms

- Cross-border payment solutions

- Compliance and identity verification tools

- Smart contract infrastructure

The key trend is clear: real-world utility is becoming the primary driver of value in the crypto space.

Conclusion: Toward a Programmable Global Economy

The collaboration between Ripple and the Monetary Authority of Singapore under Project BLOOM represents more than a technological upgrade—it is a blueprint for the future of global finance.

By integrating blockchain infrastructure, regulated stablecoins, and programmable smart contracts, BLOOM addresses longstanding inefficiencies in trade finance while opening new avenues for innovation.

As institutional players continue to enter the space and regulatory frameworks mature, the vision of a borderless, programmable financial system is rapidly becoming a reality.

For investors, builders, and policymakers alike, the message is clear: the next phase of blockchain adoption will be defined not by speculation, but by real-world impact.