Main Points :

- Retail cryptocurrency trading volumes fell sharply in 2025, with major exchanges reporting declines of up to 38%.

- Despite relatively resilient Bitcoin price action, individual investor participation has cooled significantly.

- Capital is rotating from crypto into options and equities among retail traders.

- Institutional trading activity is rising, reshaping exchange revenue structures.

- Exchanges are diversifying into subscriptions, stablecoins, and services to reduce reliance on trading fees.

- The structural evolution of crypto markets presents new opportunities in infrastructure, stablecoins, and institutional-facing products.

1. Retail Activity Contracts Despite Resilient Crypto Prices

The fourth-quarter 2025 earnings reports of Robinhood and Coinbase reveal a striking divergence between cryptocurrency prices and retail trading participation. While Bitcoin and other major digital assets have maintained relatively elevated price levels compared to prior cycle lows, individual investor activity has cooled significantly.

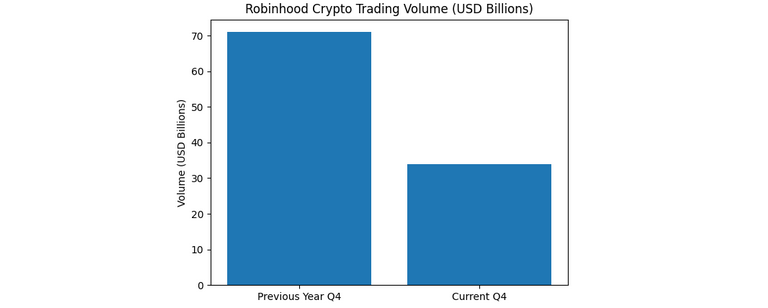

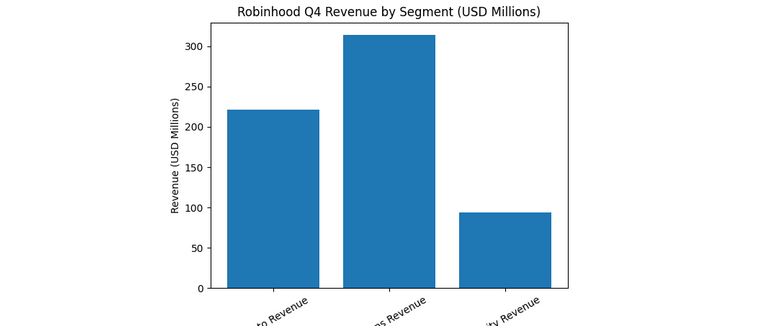

Robinhood reported total Q4 net revenue of $1.28 billion, up 27% year-over-year. However, cryptocurrency revenue fell 38% year-over-year to $221 million. Even more telling, crypto trading volume within the app dropped 52% compared to the same period last year, totaling $34 billion.

This decline occurred despite Bitcoin maintaining trading levels well above previous bear market lows. The data suggests that price resilience alone is no longer sufficient to sustain retail enthusiasm. Instead, market structure and participant composition appear to be evolving.

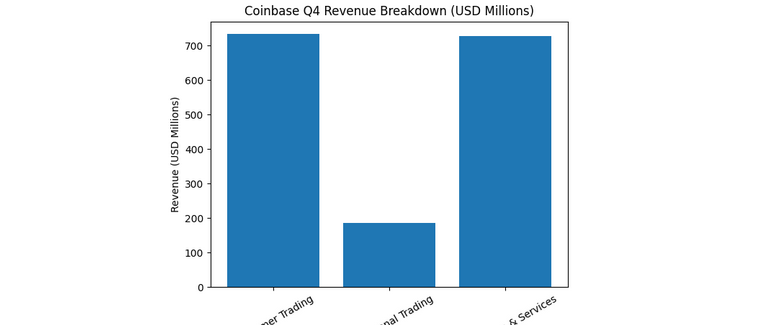

Coinbase’s Q4 performance reinforces this trend. Total revenue reached $1.781 billion, but the company posted a net loss of $667 million. Consumer trading revenue declined from $843.5 million in the prior quarter to $733.9 million. In contrast, institutional trading revenue rose to $185 million.

These figures signal a meaningful shift: retail investors are retreating while institutions gradually expand their presence.

2. Capital Rotation: From Crypto to Options and Equities

Robinhood’s internal revenue mix provides additional insight. While crypto revenue declined sharply, options trading revenue increased 41% year-over-year to $314 million. Equity trading revenue jumped 54% to $94 million.

This suggests retail traders are not exiting markets entirely; they are reallocating capital.

Several factors may explain this shift:

- Perceived risk-adjusted returns in equities and derivatives.

- Increasing macro uncertainty affecting speculative appetite.

- Reduced volatility in major cryptocurrencies compared to prior cycles.

- Growing availability of leveraged equity products.

The retail cohort that fueled explosive crypto rallies in 2020–2021 appears more selective in 2025. Instead of chasing parabolic digital asset moves, traders are diversifying into products offering structured risk or shorter-term volatility opportunities.

3. Structural Shift Toward Institutional Participation

While retail participation cools, institutional engagement is strengthening.

Coinbase’s institutional trading revenue increase to $185 million highlights growing activity from hedge funds, asset managers, and corporate treasury desks. The introduction of regulated Bitcoin ETFs and custody solutions has further legitimized digital assets in traditional finance.

Institutional participants behave differently from retail traders:

- Larger average trade sizes.

- Lower fee sensitivity.

- Preference for derivatives and structured products.

- Emphasis on compliance, custody, and liquidity depth.

This shift alters exchange economics. Retail flows are high-margin but volatile. Institutional flows are lower margin but more stable and scalable.

For crypto entrepreneurs and investors seeking new revenue streams, this suggests a pivot toward infrastructure, custody, compliance tooling, and institutional-grade liquidity services.

4. The Rise of Subscription and Stablecoin Revenue

To mitigate dependence on transaction fees, exchanges are expanding subscription and service-based revenue models.

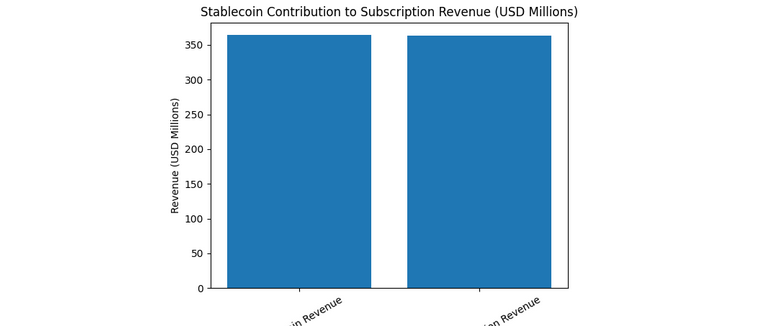

Coinbase’s subscription and services segment generated $727.4 million in Q4. Notably, stablecoin-related revenue accounted for $364.1 million—nearly half of that segment.

Stablecoins are becoming a foundational layer of crypto finance:

- Used for cross-border settlements.

- Integral to decentralized finance (DeFi).

- Core to exchange liquidity pools.

- Increasingly embedded in corporate treasury operations.

Unlike trading revenue, stablecoin revenue can be recurring and tied to reserve yields or transaction flows rather than speculative cycles.

For investors seeking practical blockchain applications, stablecoins represent one of the clearest monetization paths in the ecosystem today.

5. Market Structure: Maturation or Fatigue?

Is the decline in retail trading a temporary pause or a sign of structural maturation?

Several indicators suggest structural evolution rather than collapse:

- Institutional inflows remain steady.

- Stablecoin supply remains elevated relative to prior bear markets.

- On-chain activity is increasingly utility-driven rather than purely speculative.

- Exchanges are diversifying revenue models beyond spot trading.

Retail participation historically surges during euphoric phases. Its contraction may indicate a mid-cycle consolidation rather than long-term decline.

However, it also reflects changing retail psychology. The easy gains narrative of early crypto cycles has faded. Participants now demand clearer value propositions, regulatory clarity, and sustainable tokenomics.

6. Opportunities Emerging from the Shift

For readers seeking new crypto assets or revenue opportunities, the evolving structure suggests several strategic areas:

A. Infrastructure Tokens

Projects enabling institutional custody, cross-chain settlement, compliance tooling, or liquidity aggregation may benefit from structural demand.

B. Stablecoin Ecosystems

Stablecoin issuance, yield-bearing stable assets, and payment-layer integrations are increasingly attractive.

C. Real-World Asset (RWA) Tokenization

As institutions enter the market, tokenization of treasury bills, real estate, and private credit is gaining traction.

D. Exchange-Adjacent Services

Risk management software, market-making infrastructure, and treasury automation platforms align with institutional needs.

Retail speculation may be cooling, but institutional infrastructure spending is expanding.

7. Macro Context and Risk Considerations

Macroeconomic conditions continue influencing digital asset volatility. Higher interest rates, tighter liquidity, and shifting global risk appetite affect speculative flows.

If rates decline and liquidity expands, retail enthusiasm could reaccelerate. Conversely, prolonged macro tightening may further consolidate activity among institutional players.

The market is no longer driven solely by social media momentum. It is increasingly shaped by capital efficiency, yield strategies, and balance sheet management.

8. Conclusion: A Market Growing Up

The 38% decline in retail crypto trading, as reflected in major exchange earnings, does not signal the end of digital assets. Rather, it marks a structural transformation.

The crypto market is transitioning:

- From retail-dominated speculation to institutional integration.

- From fee-dependent exchanges to diversified financial platforms.

- From hype-driven cycles to infrastructure-led development.

For sophisticated participants, this phase offers clarity. The next wave of opportunity may not lie in viral tokens, but in foundational services powering the next decade of blockchain finance.

The retail frenzy of prior cycles built awareness. The institutional era may build permanence.