Main Points :

- Regulatory ambiguity around stablecoins may harm traditional banks more than crypto companies.

- Major banks have already invested heavily in blockchain payment infrastructure, but unclear classification prevents deployment.

- Yield differences between stablecoins and bank deposits could gradually trigger deposit migration.

- Attempts to regulate stablecoin yields may push capital toward offshore or synthetic structures.

- New crypto-native financial products such as synthetic dollar tokens could reshape the competitive landscape.

Introduction: A New Phase of Competition Between Banks and Crypto

For much of the past decade, the narrative surrounding cryptocurrency regulation has been dominated by the assumption that tighter rules would primarily hurt crypto companies. However, a growing number of financial experts now argue that the opposite may be true—at least in the short to medium term.

According to Colin Butler, Executive Vice President for Capital Markets at Mega Matrix, regulatory uncertainty surrounding stablecoins may create a strategic disadvantage not for crypto firms, but for traditional banks. His argument reflects a broader structural shift underway in global finance: banks are investing billions of dollars in digital asset infrastructure, yet the regulatory framework required to activate these systems remains incomplete.

As a result, financial institutions find themselves in an unusual position. They have built the technological rails for digital finance, but regulatory ambiguity prevents them from fully using them.

Meanwhile, crypto-native companies—long accustomed to operating in regulatory gray zones—continue innovating and capturing market share.

The implications of this imbalance extend far beyond the crypto industry itself. If stablecoins become widely adopted as a form of digital cash, the competitive dynamics between banks, fintech platforms, and decentralized finance could fundamentally reshape the global financial system.

Banks Have Already Built the Infrastructure

Despite the perception that traditional banks are slow to adopt new technologies, many of the world’s largest financial institutions have already built significant digital asset infrastructure.

Examples include:

- JPMorgan’s Onyx blockchain payment network

- BNY Mellon’s digital asset custody platform

- Citigroup’s pilot programs for tokenized deposits

These initiatives represent billions of dollars in investment and years of technological development. Banks have created internal blockchain networks, custody systems, tokenization frameworks, and digital settlement mechanisms.

Yet the full deployment of these systems has stalled.

The core issue is not technological capability—it is regulatory classification.

Financial institutions must determine how stablecoins will be categorized before launching services at scale. Will they be treated as:

- Bank deposits?

- Securities?

- Payment instruments?

- Or a new regulatory category entirely?

Without clarity, bank legal teams cannot justify large-scale capital deployment.

As Butler explains, corporate legal advisors are increasingly telling bank boards that further investment cannot be approved until regulators clearly define the status of stablecoins.

This hesitation reflects a structural difference between banks and crypto companies.

Banks operate within strict compliance frameworks and cannot experiment freely in regulatory gray areas. Crypto companies, however, have built their entire business models around navigating those gray zones.

As a result, regulatory uncertainty ironically favors crypto-native players.

The Yield Gap: A Hidden Driver of Financial Migration

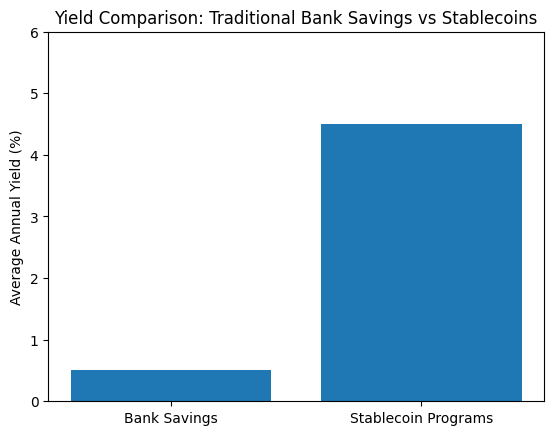

Another critical factor reshaping the competitive landscape is the widening yield gap between stablecoins and traditional bank deposits.

Crypto exchanges frequently offer returns of 4–5% annually on stablecoin balances through lending programs or staking mechanisms.

In contrast, the average interest rate for a U.S. savings account remains below 0.5% annually.

When expressed in dollar terms:

| Asset Type | Typical Annual Yield |

|---|---|

| Traditional bank savings | ~$0.50 per $100 |

| Stablecoin programs | ~$4–$5 per $100 |

This difference may appear modest, but historically even small yield gaps have triggered massive capital movements.

During the 1970s, the emergence of money market funds (MMFs) led to a major shift of deposits away from traditional bank accounts. Investors moved funds to higher-yielding instruments once regulatory ceilings on bank interest rates became restrictive.

Today, the technological barriers to moving money are dramatically lower.

Transfers between bank accounts and crypto platforms can occur within minutes, and global crypto exchanges allow instant conversion between fiat currency and stablecoins.

According to Butler, this dynamic could accelerate deposit migration in the future.

However, Fabian Dori, Chief Investment Officer at digital asset bank Sygnum, believes the situation is not yet critical.

Institutional investors still prioritize:

- regulatory certainty

- operational resilience

- financial stability

These factors continue to favor banks.

Nevertheless, Dori warns that gradual capital migration could emerge among:

- fintech users

- global businesses

- technologically sophisticated investors

These groups are already comfortable moving liquidity across multiple platforms.

Once stablecoins are widely perceived not merely as trading tools but as productive digital cash, competitive pressure on banks could intensify significantly.

Yield Restrictions Could Push Innovation Offshore

Regulators are also grappling with another challenge: whether stablecoin issuers should be allowed to pay interest to token holders.

Under current U.S. law, stablecoin issuers generally cannot directly pay yield to users.

However, crypto platforms have developed numerous workarounds.

Examples include:

- lending programs

- staking rewards

- promotional campaigns

- liquidity incentives

These mechanisms allow platforms to offer returns without technically classifying them as interest payments.

If regulators attempt to ban such yield mechanisms more broadly, capital may migrate toward alternative financial structures.

One emerging example is the synthetic dollar token.

Unlike traditional stablecoins backed by reserves such as U.S. Treasury bills, synthetic tokens generate yield through derivatives strategies.

A prominent example is USDe, developed by the protocol Ethena.

Instead of holding physical reserves, USDe uses derivatives markets to create a synthetic dollar exposure while simultaneously generating yield.

These mechanisms allow synthetic tokens to continue providing returns even if regulated stablecoins cannot.

Butler warns that excessive regulation could unintentionally accelerate this trend.

If investors are unable to earn returns from regulated stablecoins, they may move capital into:

- synthetic stablecoins

- offshore lending platforms

- decentralized finance protocols

Ironically, such migration could reduce consumer protection and financial transparency—the opposite of what regulators intend.

As Butler notes:

“Capital will always seek yield.”

The Strategic Future of Stablecoins

The long-term importance of stablecoins extends far beyond speculative trading.

In many ways, stablecoins represent the first large-scale experiment in programmable digital cash.

They allow instantaneous global transfers, programmable financial logic, and integration with decentralized applications.

Stablecoins are already widely used in several areas:

- crypto trading settlement

- cross-border payments

- remittances

- decentralized finance

- collateral for derivatives markets

Their market capitalization has grown to over $150 billion globally, making them one of the largest segments of the crypto ecosystem.

If regulatory clarity emerges, banks may accelerate their participation in this market.

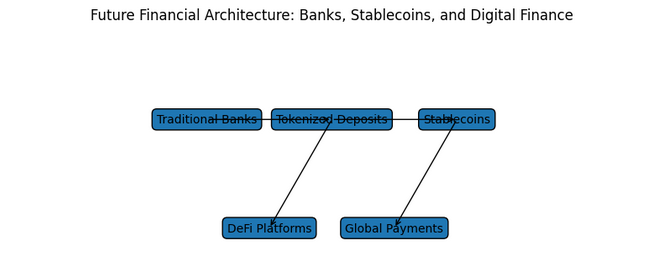

Several potential scenarios are emerging:

1. Bank-issued stablecoins

Major financial institutions could launch their own stablecoins backed by deposits.

2. Tokenized bank deposits

Banks may tokenize existing deposits on blockchain networks rather than issuing new coins.

3. Hybrid public-private payment systems

Governments and banks could collaborate on regulated digital payment networks.

Each of these models would integrate blockchain infrastructure into the traditional financial system.

However, regulatory clarity will determine how quickly such systems develop.

Implications for Crypto Investors and Builders

For crypto investors and entrepreneurs, the regulatory landscape around stablecoins represents both risk and opportunity.

Key trends to watch include:

Growth of synthetic yield-bearing assets

Products like USDe suggest that algorithmic financial engineering may play a larger role in crypto markets.

Institutional blockchain infrastructure

Banks have already built much of the underlying infrastructure needed for digital finance.

Once regulatory barriers are removed, institutional adoption could accelerate rapidly.

Cross-border financial competition

Stablecoins could reshape global capital flows by enabling faster and cheaper international payments.

The emergence of digital dollar ecosystems

Stablecoins are increasingly functioning as a global digital dollar system operating outside traditional banking rails.

These developments suggest that stablecoins may become one of the most strategically important components of the digital asset economy.

Conclusion: A Regulatory Crossroads for Global Finance

The debate surrounding stablecoin regulation highlights a broader tension in modern financial policy.

On one hand, regulators aim to protect consumers and maintain financial stability. On the other hand, excessive restrictions could unintentionally push innovation—and capital—into less transparent environments.

Ironically, the institutions most constrained by regulatory ambiguity may be the very banks regulators are trying to protect.

Crypto companies, having spent years navigating uncertain regulatory environments, may continue operating with relative agility.

As a result, the next phase of financial innovation may depend less on technology and more on regulatory clarity.

If governments establish clear frameworks for stablecoins, banks and fintech firms could integrate blockchain technology into the global financial system at unprecedented speed.

If not, the center of innovation may shift further toward decentralized and offshore ecosystems.

Either way, stablecoins have already begun reshaping the architecture of money.

The only remaining question is who will ultimately control that future.