Main Points :

- SEC and CFTC staff jointly state that existing law does not prohibit regulated exchanges from listing spot crypto products—including leveraged or margined retail commodities.

- This move formalizes and builds upon the President’s Working Group (PWG) recommendation to promote U.S. blockchain innovation via regulatory clarity.

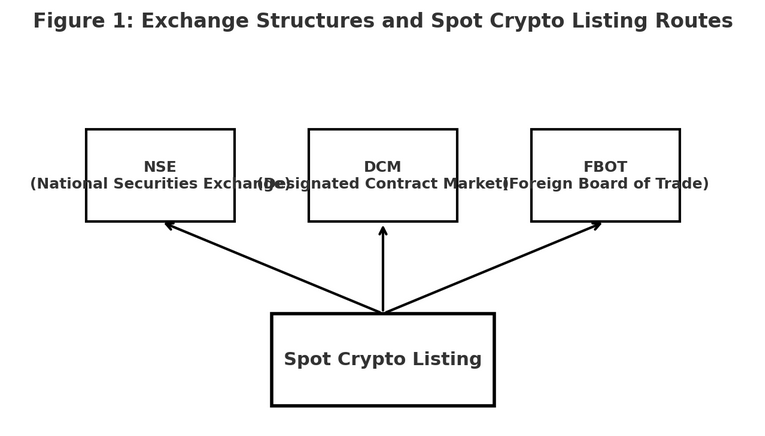

- Key exchanges including NSEs (e.g., Nasdaq, NYSE), DCMs (e.g., CME), and FBOTs may now list spot crypto products; regulators invite filings and engagement.

- Guidance covers custody, clearing, surveillance, trade data transparency, and fair and orderly market principles.

- This marks a shift away from enforcement-heavy posture toward innovation-friendly regulation under the current U.S. administration.

- Recent context: CFTC had already opened spot crypto trading on registered futures exchanges; this joint statement reinforces and expands on that groundwork.

1. Regulatory Clarification: Law Does Not Preclude Spot Crypto Trading

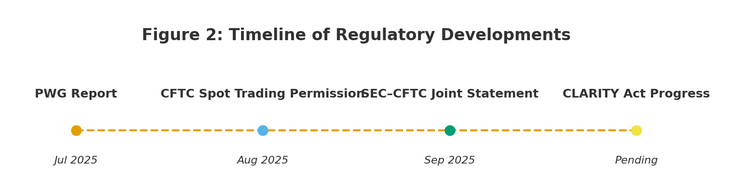

In a landmark joint staff statement issued on September 2, 2025, the U.S. Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) clarified that current U.S. law does not prohibit certain regulated exchanges from facilitating trading in spot crypto asset products—even those with leverage, margin, or financing features—so long as those exchanges are registered as National Securities Exchanges (NSEs under the SEC), Designated Contract Markets (DCMs), or Foreign Boards of Trade (FBOTs) under the CFTC.

This statement endorses the view that innovation in spot crypto markets can proceed under existing legal frameworks, without awaiting comprehensive new legislation—although new proposals such as the CLARITY Act are still making their way through Congress.

2. President’s Working Group: Steering Regulatory Alignment

The joint statement reflects key recommendations from the President’s Working Group (PWG) on Digital Asset Markets, particularly the call to preserve innovation within the U.S. by offering clear regulatory pathways. The PWG report urged use of existing authority to define conditions for listing leveraged or margined spot crypto products.

In effect, the SEC’s Project Crypto and the CFTC’s Crypto Sprint initiatives represent concrete steps in aligning regulatory tools with the PWG’s vision.

3. Opening the Doors: Who Can List, and What’s Next

Under the current guidance, major regulated venues—such as the Nasdaq, NYSE, CME Group, Cboe Global Markets (as NSEs or DCMs), and compliant FBOTs—may list spot crypto products. They are encouraged to engage with SEC or CFTC staff for guidance or to initiate the review of proposals.

4. Essential Operational Considerations for Listing Exchanges

The guidance highlights several practical considerations for exchanges pursuing spot crypto operations:

- Margin, Clearing, and Settlement: Clearinghouses may partner with custodians for customer account maintenance. Both SEC’s Division of Trading and Markets and CFTC’s Division of Clearing and Risk stand ready to advise.

- Market Surveillance & Pricing: Sharing reference pricing venues among NSEs, DCMs, and FBOTs supports market monitoring.

- Transparency: Encouraged dissemination of trade data by exchanges enhances public awareness.

- Fair and Orderly Markets: Use of efficient execution and transparency mechanisms helps promote competition.

- Innovation with Protections: Regulators commit to working with participants to enable technological innovation while maintaining investor/customer protections.

5. Regulatory Climate Shift: From Enforcement to Facilitation

This represents a fundamental tone change in U.S. crypto policy. The SEC and CFTC have long been viewed as enforcement-heavy—particularly under the SEC, which historically pursued lawsuits against major crypto platforms. The new collaboration signals a pivot toward enabling innovation.

SEC Chair Paul Atkins stated that market participants should have the “freedom to choose where they trade spot crypto assets,” while CFTC Acting Chair Caroline Pham framed the move as closing a chapter of mixed signals and opening a new chapter supportive of innovation.

6. Recent Moves: The CFTC Already Laid Groundwork

Just weeks prior, the CFTC announced it would allow spot crypto asset contracts on registered futures exchanges—a move hailed as a major regulatory breakthrough. The CFTC emphasis was coordinated with the SEC under Project Crypto.

This enhances the credibility and continuity of the joint staff statement, showing sustained momentum rather than an isolated announcement.

7. What This Means for Stakeholders

For investors and blockchain innovators, the message is clear: U.S.-based platforms can now explore spot crypto offerings with greater legal certainty and institutional collaboration.

For traditional finance venues, this is a green light to consider entry into crypto trading via regulated channels—potentially broadening market depth and mainstream participation.

And for regulatory evolution, this collaboration may serve as a template for further harmonization in digital asset oversight.

Conclusion

The SEC and CFTC joint staff statement is a decisive step toward bringing spot crypto innovation into the regulated U.S. financial system. It clarifies legal boundaries, encourages dialogue with regulated trading platforms, and places transparency, surveillance, and investor protection at the core of future spot crypto markets. Set against the backdrop of transformative legislation and policy frameworks, this milestone signals that U.S. regulators are choosing to enable rather than hinder blockchain-based financial innovation.