Main Points :

- The American Bankers Association (ABA) is urging the Office of the Comptroller of the Currency (OCC) to enhance transparency and tighten review standards for crypto bank charters.

- The pending implementation of stablecoin legislation may reshape supervisory expectations across federal agencies.

- Failures such as FTX and Celsius highlight unresolved operational and custody risks.

- Regulatory overlap between banking and securities law could blur supervisory boundaries.

- For investors and blockchain operators, regulatory clarity may create both near-term friction and long-term opportunity.

I. Introduction: A Structural Debate Over the Future of Crypto Banking

The United States is entering a decisive phase in its treatment of crypto-native financial institutions. On February 11, the American Bankers Association (ABA) submitted a formal statement to the Office of the Comptroller of the Currency (OCC), calling for greater transparency and stricter evaluation criteria in the chartering process for crypto-focused banks.

The debate is not merely administrative. It reflects deeper structural questions about how digital asset institutions should integrate into the regulated banking system. Should crypto banks be evaluated under traditional prudential standards designed for deposit-taking institutions? Or should regulators craft new supervisory frameworks tailored to tokenized assets, stablecoins, and blockchain-based custody?

The ABA argues that recent OCC approval processes lack sufficient public disclosure, making it difficult to evaluate applicants’ business models, operational resilience, and systemic risk exposure. At stake is not only consumer protection but also confidence in the broader financial system.

II. The Regulatory Landscape: OCC, Federal Reserve, FDIC, and the Expanding Rulemaking Horizon

The ABA’s statement highlights the incomplete regulatory environment surrounding stablecoins and crypto banking. Proposed federal stablecoin legislation—often described as a comprehensive framework—will likely require coordinated rulemaking across the OCC, the U.S. Treasury, the Federal Reserve, the Federal Deposit Insurance Corporation (FDIC), and state regulators.

Such interagency coordination can take years. In the meantime, granting charters to crypto-focused banks may create regulatory asymmetry. If institutions operate under evolving or partially defined standards, supervisory clarity may lag behind operational expansion.

The ABA suggests that until this rulemaking process matures, the OCC should not rush charter approvals. The concern is that premature licensing may embed structural weaknesses into the regulated banking perimeter.

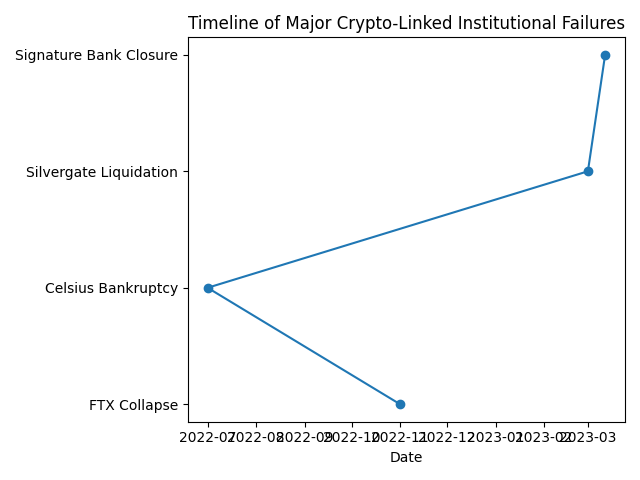

III. Operational Risk Lessons from Recent Crypto Failures

The collapses of FTX and Celsius demonstrated how weak internal controls, asset commingling, and inadequate risk segregation can produce multi-billion-dollar losses measured in U.S. dollar terms.

“Timeline of Major Crypto-Linked Institutional Failures”

These failures were not traditional bank runs. They were liquidity collapses amplified by opaque balance sheets, leverage exposure, and insufficient governance frameworks.

For regulated crypto banks, the primary risk categories include:

- Custody segregation failures

- Smart contract vulnerabilities

- Liquidity mismatches between on-chain and off-chain liabilities

- Counterparty exposure to exchanges and decentralized finance protocols

- Concentration risk in stablecoin reserves

The ABA contends that without transparent disclosure of how applicants manage these operational risks, granting charters could introduce systemic vulnerabilities into federally supervised institutions.

IV. Capital Requirements and the Question of Supervisory Consistency

One of the ABA’s central criticisms is the lack of clarity around how capital requirements are calculated for crypto bank applicants.

Traditional banks must maintain capital ratios based on risk-weighted assets. However, digital assets do not always fit neatly into existing risk buckets. For example:

- Is a fully reserved stablecoin custody asset equivalent to cash?

- Should Bitcoin ($BTC) held in custody be assigned a higher risk weight due to price volatility?

- How should tokenized securities be treated under Basel-style frameworks?

Without standardized methodologies, different institutions may face inconsistent supervisory expectations. This not only complicates compliance planning but may also create competitive distortions between traditional banks and crypto-native entities.

V. The SEC Boundary Problem: Banking Versus Securities Supervision

The ABA also raised concerns about overlap between banking regulation and securities oversight. Certain trust banks may rely on statutory exemptions under securities law. However, if a significant portion of their activities resembles brokerage, investment advisory, or fund management services, registration with the Securities and Exchange Commission (SEC) could be required.

This creates a boundary problem:

- If crypto banks expand into tokenized securities, staking-as-a-service, or yield-generating products, do they remain primarily banks?

- Or do they become hybrid institutions subject to dual oversight?

The ABA warns that expanding SEC supervisory reach over national banks could dilute the value of an OCC charter and create legal uncertainty.

VI. Deposit Insurance, Naming Rights, and Consumer Protection

Another area of contention involves institutions that receive national trust bank charters but do not participate in federal deposit insurance through the FDIC.

If such an institution were to fail, the OCC would appoint a receiver to oversee liquidation. However, existing resolution frameworks were not designed for blockchain-based balance sheets or tokenized customer liabilities.

The ABA has recommended regulatory amendments prohibiting non-FDIC-insured institutions from using the word “bank” in their name. The objective is to prevent consumer confusion and mitigate reputational risk across the banking sector.

For retail and institutional investors alike, naming conventions influence perceived safety. Clear labeling becomes essential in a market where digital asset custody and traditional deposits may coexist within similar branding structures.

VII. The Federal Reserve’s “Simplified Master Account” Proposal

In parallel, the Federal Reserve recently closed public comments on a proposal concerning simplified access to master accounts.

Crypto-native institutions, including Anchorage Digital Bank, have expressed support for streamlined access, arguing that direct settlement connectivity reduces counterparty risk and improves payment efficiency.

Conversely, regional banking associations in states such as Colorado and Illinois have raised safety concerns, arguing that insufficiently vetted crypto institutions could expose the Federal Reserve payment system to novel risks.

This policy crossroads reflects a broader tension: integrating blockchain-native institutions into core financial infrastructure while preserving systemic stability.

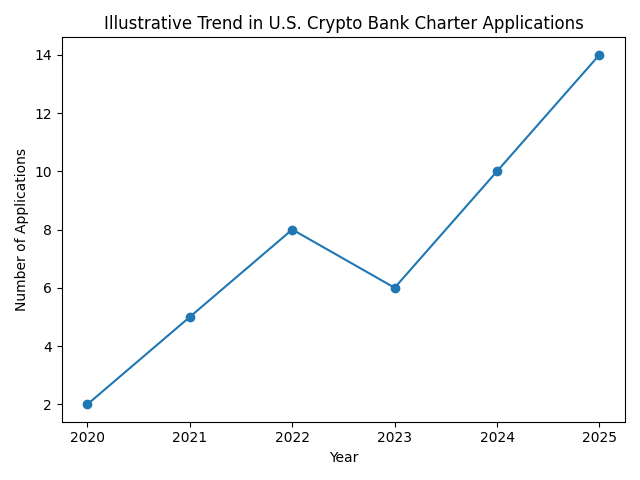

VIII. Market Implications: Friction Today, Infrastructure Tomorrow

For readers seeking new digital asset opportunities and revenue streams, regulatory tightening may initially appear negative. However, long-term clarity often supports sustainable growth.

“Illustrative Trend in U.S. Crypto Bank Charter Applications”

Although illustrative, the broader market trend suggests increasing institutional interest in regulated crypto banking structures. This trend aligns with:

- Stablecoin expansion measured in tens of billions of dollars

- Tokenized Treasury products growing in institutional portfolios

- Payment firms exploring blockchain-based settlement rails

- Traditional asset managers launching spot crypto exchange-traded funds

If charter approvals become more rigorous but transparent, well-capitalized operators may gain durable competitive advantages.

IX. Strategic Considerations for Blockchain Entrepreneurs

For builders and fintech operators, several strategic conclusions emerge:

- Regulatory architecture is becoming multi-layered. Success will require compliance integration across banking, securities, and payments law.

- Capital planning must anticipate volatility stress scenarios denominated in U.S. dollars.

- Governance transparency may become a competitive differentiator.

- Naming, branding, and deposit insurance status must be communicated clearly to avoid reputational spillover.

X. Conclusion: Transparency as Infrastructure

The ABA’s call for transparency is not merely defensive lobbying by traditional banks. It reflects a broader recognition that crypto banking has entered the systemic perimeter.

The question is no longer whether blockchain-based institutions will integrate into regulated finance. The question is how.

If regulators prioritize disclosure, capital adequacy, operational risk controls, and interagency coordination, the result may be a more resilient hybrid financial architecture.

Short-term delays in charter approvals may frustrate some applicants. However, for long-term investors, disciplined regulatory integration may ultimately support larger-scale capital flows, deeper liquidity, and broader mainstream adoption.

The U.S. crypto banking experiment is no longer peripheral. It is structural. And the debate over transparency may define its durability.