Main points :

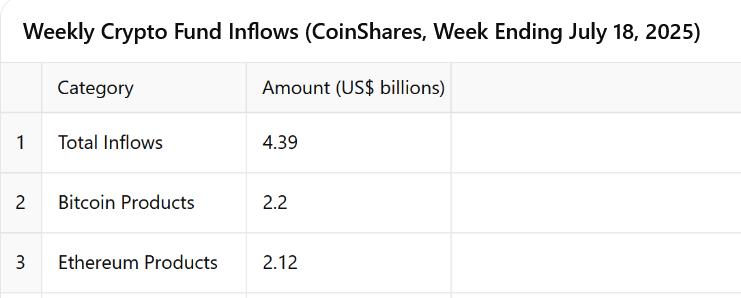

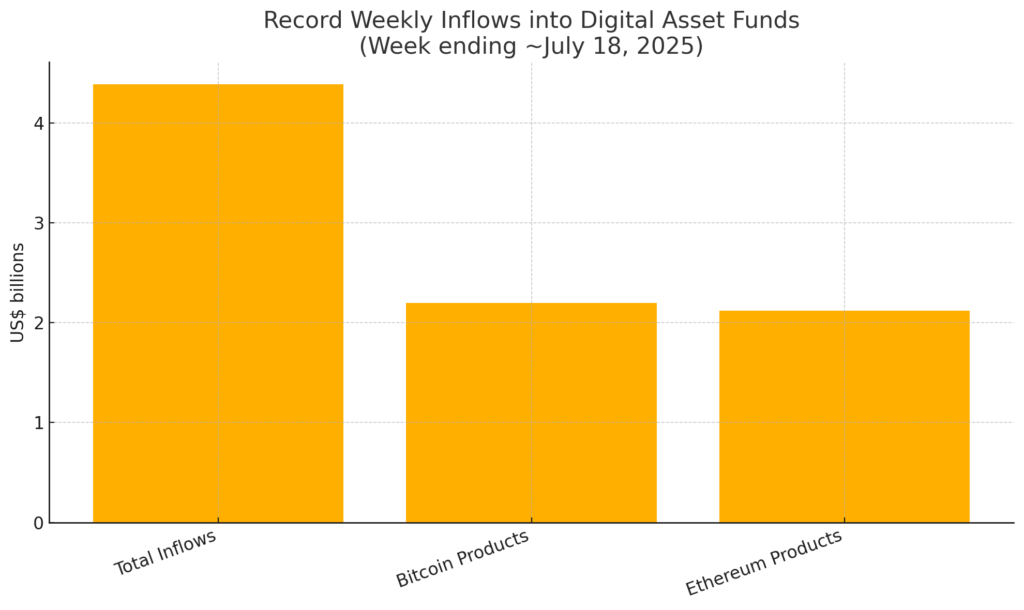

- Digital asset funds logged an all-time high $4.39B weekly inflow, topping the previous $4.27B record from December 2024.

- 14 straight weeks of inflows show persistent institutional and retail demand; total AuM hit roughly $220B.

- Ethereum products drew ~$2.12B, nearly matching Bitcoin’s ~$2.2B, as ETH rallied ~25% last week.

- Bitcoin recently set a new ATH above $120K; the broader crypto market briefly surpassed $4T in value.

- U.S. policy momentum (stablecoin bill, broader digital asset framework) and prior SEC approval of spot ETH ETFs continue to legitimize the asset class.

- For builders and yield-seekers: flows are concentrating in BTC/ETH ETPs, but second-order opportunities are opening in altcoins, staking, L2 infrastructure, RWA tokenization, and compliance tooling.

1. A Historic Inflow Week—and What It Really Means

CoinShares’ latest weekly report shows digital asset investment products attracted $4.39 billion last week—the largest weekly haul since tracking began—beating the $4.27B set in December 2024, right after the U.S. election. This marks 14 consecutive weeks of net inflows, pushing assets under management to roughly $220B.

Why care? Sustained inflows over a quarter suggest crypto allocations are no longer a “trade” but part of ongoing portfolio construction. Even if retail still dominates ETF ownership, the headline numbers create a feedback loop: higher AuM begets more coverage, which attracts more allocators.

[Insert Figure 1 here – Bar chart of weekly inflows: Total vs. BTC vs. ETH]

(The chart is displayed above. You can download it here: Download the image)

2. Ethereum Nearly Parity With Bitcoin: A Narrative Shift

Ethereum products absorbed ~$2.12B, almost tying Bitcoin’s ~$2.2B.CoinShares notes ETH’s weekly inflow was nearly double its previous record (~$1.2B), and 2025 inflows have already exceeded all of 2024 ($6.2B+). ETH’s price surged roughly 25% over the week, catalyzing a broader altcoin bounce.

Drivers include:

- The spot Ether ETF approval/launch in the U.S. (mid-2024) that normalized ETH as an investable “commodity-like” asset.

- Anticipation of fee-burning supply dynamics and staking yield as quasi “crypto-dividends.”

- A rotation from overextended BTC to ETH and high-beta altcoins after BTC’s ATH pause.

3. Macro & Policy Tailwinds: From Stablecoin Bills to the “Genius Act”

The crypto market briefly surpassed $4T in capitalization as U.S. lawmakers advanced stablecoin rules and a broader digital asset framework—while also moving to block a U.S. CBDC. The so-called “Genius Act” aims to clarify token classifications and could be a catalyst for deeper institutional participation.

For builders, legislation is opportunity: compliance-ready stablecoin rails, Travel Rule integrations, and KYC/AML modules can be productized for global launches. For investors, regulatory clarity tends to compress risk premiums, favoring mid-cap tokens with real cash flows or staking yields.

4. Bitcoin Still King—But Acting More Like Digital Gold

Bitcoin breached $120K this week before a modest pullback, and forecasts call for $200K by year-end. While such targets are speculative, BTC’s behavior resembles a macro hedge: corporates are adding it to treasuries, and ETFs have funneled tens of billions since launch.

If BTC is “digital gold,” ETH is positioning as “digital yield + programmable collateral.” That dichotomy matters for portfolio design: risk-on builders might harvest ETH staking plus L2 yields; conservative allocators might ladder BTC exposures through covered-call ETFs.

5. Reading the Flows: Where the Next Dollar Might Go

Flows show concentration in BTC and ETH, but second-order effects are playing out:

- Layer-2s & Rollups: If ETH demand grows, gas markets and L2 throughput spike. Revenue-sharing or fee-rebate tokens could benefit.

- Restaking & “DeFi Treasuries”: Institutions hunting yield may back tokenized T-bills, real-world assets (RWA), and restaking protocols offering “secured services” for ETH.

- Altcoin Beta: XRP, SOL, and AI-linked tokens (e.g., OZAK-AI cited in community press) are surfacing in trader narratives.

- Compliance & Infrastructure Plays: Travel Rule, AML, KYT providers see rising demand as regulated inflows scale.

6. Strategy for Builders & Investors Seeking the “Next Revenue Stream”

For token issuers/DeFi founders:

- Align with regulated rails—integrate stablecoin compliance hooks and custodial-grade reporting.

- Offer transparent, on-chain yield sources (staking, RWAs, MEV smoothing) rather than opaque tokenomics.

- Build liquidity with programmatic market-making and ETF/ETP partnerships—flows prove institutions prefer wrappers they understand.

For investors/traders:

- Use BTC/ETH ETP flows as a sentiment barometer; chase beta only when breadth expands beyond those two.

- Watch regulatory calendars (e.g., Senate votes on digital asset bills) as catalysts.

- Allocate a sleeve to infrastructure tokens (or equity in infra firms) that monetize compliance, custody, or scaling.

7. Risks That Could Break the Streak

- Price Shock: A sharp BTC correction can drain confidence and halt inflows.

- Regulatory Whiplash: A Senate rewrite or enforcement action could stall U.S. momentum.

- Liquidity Crunch: Overreliance on a few market makers/ETPs increases systemic risk.

- ETF Saturation: As ETF menus explode, retail may chase risky leveraged products, adding volatility.

8. Conclusion: From Narrative to Cash Flow

We’re witnessing the maturation of crypto as an investable category: record inflows, policy frameworks taking shape, and a clear two-asset core (BTC & ETH) around which everything else orbits. For those hunting new assets and revenue, the alpha is moving into infrastructure, yield primitives, and compliant on/off-ramps—the picks-and-shovels for the next $4T.