Main Points:

- Bitcoin’s divergence from gold and equities reflects growing awareness of asset-specific risks rather than a pure safe-haven logic.

- The rise of “treasury companies” holding crypto on corporate balance sheets carries inherent financial risks tied to volatility and valuation.

- The expansion of stablecoins, and their dependency on treasury assets, is both a driver of liquidity and a structural vulnerability.

- Recent regulatory, institutional, and macro shifts are reshaping how Bitcoin and stablecoins interact with traditional markets.

- For investors in Japan and globally, a nuanced strategy—emphasizing diversification, risk assessment, and trend awareness—is now essential.

Below is the English article version, followed immediately by a Japanese translation (without summarizing the translation).

1. Bitcoin’s Divergent Path Amid Gold and Stock Strength

In mid-2025, Bitcoin has exhibited behavior that sets it apart from traditional safe-haven assets and risk instruments alike. While U.S. equities hover near highs and gold has surged, Bitcoin has lagged or even declined—revealing that it no longer moves strictly in tandem with either markets or inflows into hard assets.

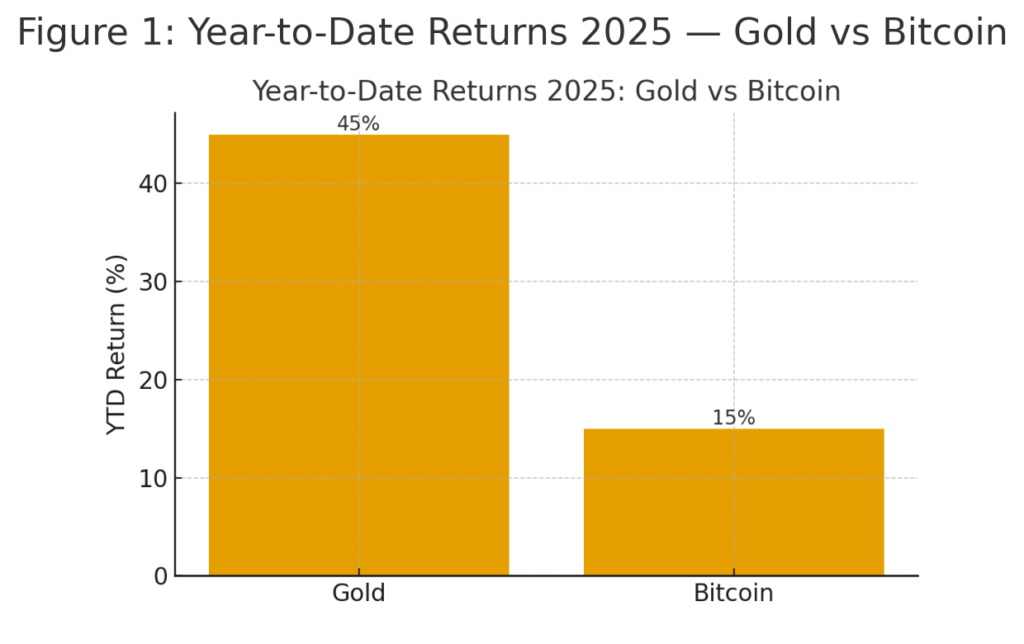

Historically, many investors positioned Bitcoin as a “digital gold,” assuming it would hedge inflation or act defensively when equities wavered. But recent performance suggests its role is evolving. In 2025 so far, gold has climbed over 30%, whereas Bitcoin has gained closer to 15%, indicating a widening divergence in how markets treat each asset class.

One reason is that Bitcoin increasingly behaves as a distinct financial instrument rather than merely a speculative asset or safe store. Its correlation with stock indices has fluctuated over time; daily return correlation from 2014 to April 2025 is modest at ~0.2, but in certain market regimes, correlations jump to ~0.5 or more. Moreover, as institutional adoption has grown, some studies show peaks of correlation reaching as high as 0.87 in 2024.

In short: Bitcoin’s price is now influenced by its own internal dynamics—treasury holdings, stablecoin flows, regulatory signals—not just macro sentiment or safe-haven demand.

2. Treasury Holdings as a Double-Edged Sword

2.1 The Rise of Crypto Treasury Companies

In recent years, a wave of companies (so-called “treasury firms”) has embraced holding large quantities of Bitcoin or other crypto assets on their balance sheets. The rationale: potential upside, signaling conviction, and expanding financial flexibility. For example, as of mid-September 2025, one leading company held nearly 640,000 BTC (valued at ~$47.2 billion).

But this strategy carries hidden risks. Many of these companies are currently trading at valuations lower than the value of their crypto holdings (i.e. market capitalization < crypto reserve), raising red flags about how the market perceives their sustainability.

2.2 Volatility & Mark-to-Market Risk

With Bitcoin’s historically high volatility, the value of those holdings can swing wildly. A steep drawdown doesn’t merely hurt returns—it can erode a firm’s capital ratios, credit metrics, and even solvency. When markets turn, forced liquidation or margin stress may ripple across the ecosystem.

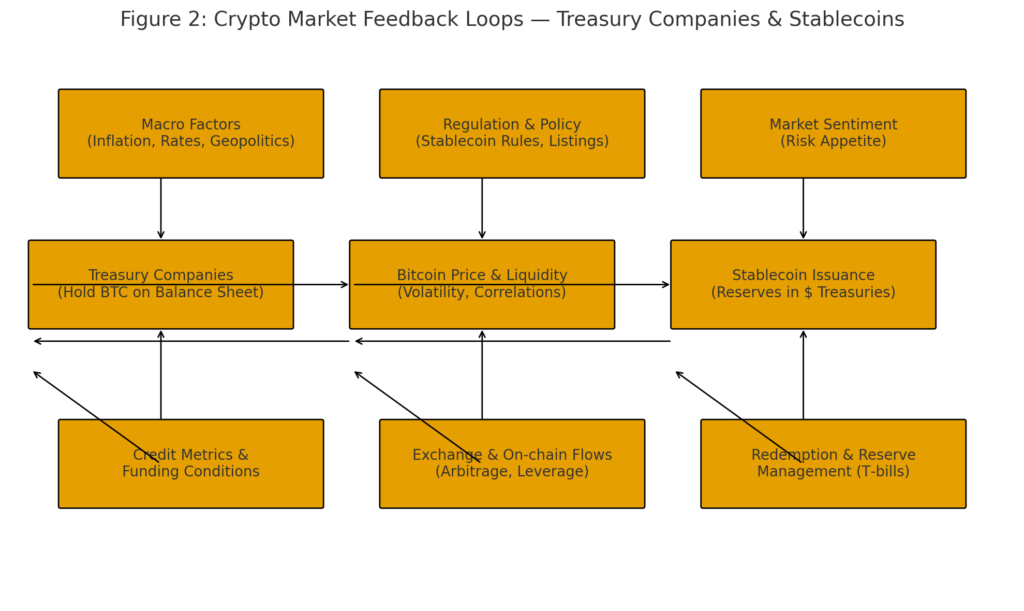

2.3 Structural Feedback Loops

Crypto treasury firms interact with stablecoin issuances, lending, staking, and liquidity operations. Stress in one area—say, a stablecoin redemption run—can force these firms to divest Bitcoin, creating cascading downward pressure. The market is becoming more sensitive to these internal feedback loops.

3. Stablecoins: Liquidity Engines and Systemic Vulnerabilities

3.1 The Growth Engine of Crypto Markets

Stablecoins serve as the plumbing of the crypto economy—facilitating trading, lending, arbitrage, and on-chain settlement. As of 2025, many firms see 2025 as an inflection point for tokenized cash and stablecoin adoption, supported by clearer regulation, improving security, and institutional readiness.

Research shows that demand for stablecoins is tightly correlated with demand for non-stablecoin crypto assets (e.g. Bitcoin). In downturns, stablecoin outflows force collateral liquidation, which can amplify stress.

3.2 The Dependency on U.S. Treasuries & the “Discount” Effect

Many stablecoins—especially the dominant ones—hold large quantities of U.S. Treasuries or cash equivalents to back their peg. Tether (USDT), for instance, holds tens of billions of dollars in Treasuries, making it one of the largest non-sovereign buyers of U.S. T-bills.

Recent econometric work argues that Tether’s share of the U.S. Treasury market has a measurable “discount effect” on yields: that is, increased stablecoin demand lowers short-term interest rates.

However, this dependency introduces risks: if stablecoin demand collapses, they may need to offload Treasuries quickly, causing fire sales and contagion into sovereign debt markets. Indeed, the Bank for International Settlements (BIS) warns of tail risks from such dynamics.

3.3 Technical, Economic & Regulatory Risks

Stablecoins face risks beyond market dynamics. Smart contract vulnerabilities, reserve opacity, redemption delays, and shifting regulation are real threats in 2025.

Regulatory frameworks are catching up. In the U.S., the GENIUS Act has passed, mandating stablecoins to be backed 1:1 by low-risk assets, with transparency and dual federal-state oversight.

Meanwhile, some argue future stablecoins could be bank-issued or fully regulated, potentially altering the dynamics of crypto liquidity and bypassing crypto exchanges.

4. Recent Trends & Institutional Pressures (2025 Updates)

4.1 Bitcoin’s Endurance & Market Sentiment

Amid gold’s rally, Bitcoin has shown signs of resilience. On September 30, 2025, Bitcoin rebounded to around $114,000, up ~2–5%, partly driven by renewed investor risk appetite.

Yet gold continues to dominate headlines. As of late September, gold broke above $3,800 per ounce, up ~45% for the year, driven by geopolitical risk, inflation fears, and U.S. fiscal instability.

4.2 Regulatory & Institutional Moves

- Swift’s blockchain initiative: In response to stablecoin growth, SWIFT plans to deploy its own blockchain infrastructure for cross-border payments in collaboration with major banks and Consensys.

- China’s offshore stablecoin: China launched a yuan-backed stablecoin (AxCNH) in Kazakhstan, pushing its blockchain ambitions and internationalizing its currency.

- Corporate consolidation with Bitcoin holdings: Strive (a bitcoin-centric company) plans to acquire Semler in an all-stock deal and add ~5,816 BTC to its treasury, strengthening its position as a treasury company.

These developments suggest the lines between traditional finance, sovereign policy, and crypto are blurring.

5. Insights for Investors & Practitioners in Japan

5.1 Rethinking “Hedge” vs. “Speculation”

The notion of Bitcoin as a hedge is under stress. Unlike gold, which still tends to rise in equity drawdowns, Bitcoin may perform better under bond stress or inflationary pressure.

Japanese investors should view Bitcoin not as a pure safe-haven but as a financial asset with embedded structural risks.

5.2 Diversification is More Critical Than Ever

Given how Bitcoin’s correlation with equities and fixed income shifts over time, diversification across asset classes remains essential. Relying solely on crypto exposure is increasingly dangerous.

5.3 Focus on Structural Quality & Transparency

When selecting crypto projects, look beyond price charts. Evaluate treasury holdings, stablecoin backing, governance, transparency of reserves, smart contract security, and regulatory compliance.

5.4 Stay Agile & Monitor Macro-Regulatory Signals

In 2025, policy changes (such as U.S. stablecoin laws, central bank behavior, or China’s crypto-initiatives) can rapidly change the landscape. Having flexible allocations and hedges is crucial.

Conclusion

Bitcoin’s recent divergence from gold and equities signals its maturation as a financial asset with its own internal mechanics. The growth of crypto treasury firms and stablecoins has been a powerful driver of market liquidity—but also introduces structural vulnerabilities. In 2025, regulatory shifts, institutional fund flows, and macro dynamics are reconfiguring how crypto interacts with legacy markets.

For those seeking new crypto opportunities or next-generation income sources, the key is disciplined, multifactor evaluation: price momentum matters, but so do balance sheet integrity, reserve transparency, and macro alignment. As the ecosystem grows up, success will go to those who read not just charts, but the deeper architecture of value and risk.